Real-Time Prediction Market Data: Sources, Latency, and What Clean Feeds Cost

Before you can act on a Polymarket edge, the price has to be correct. Before the price can be correct, the data feeding into your analysis has to be clean, current, and arriving fast enough to matter.

Most traders do not think about data infrastructure until it fails them. The market moved 7 cents, they got a fill at the old price, and they spent the next 20 minutes figuring out whether their feed was lagging or whether the move was genuine. That is a data problem. It is also a solvable one, once you understand the options.

Quick Answer

Prediction market data comes from three primary sources: the Polymarket CLOB API and Gamma API (publicly accessible, variable latency), on-chain Polygon data (ground truth, higher processing latency), and cleaned third-party products like DG3 (pre-processed, fair value applied, cross-market context included). For research and analytics, the Gamma API is sufficient. For execution-speed-sensitive applications, WebSocket feeds are necessary. For building a complete analytical workflow rather than just a price feed, a terminal that processes the raw data into usable signals removes the engineering step between data and decision.

Key Takeaways

- Data latency in prediction markets is the gap between when a price update occurs on-chain and when you can act on it. A 2-second lag on a stable afternoon market costs nothing. A 2-second lag during the first 60 seconds of a major news repricing can cost the entire edge window that motivated the trade.

- The Polymarket CLOB API provides WebSocket streaming with sub-second latency on active markets. REST polling is appropriate for research and analytics. WebSocket is necessary for execution-speed-sensitive applications and automated systems.

- On-chain Polygon data is the ground truth for all Polymarket settlement. It is also slower to process than the CLOB API because each block confirmation adds latency. For settlement verification, use on-chain data. For execution decisions, the CLOB API is faster.

- Data quality has two dimensions: how fresh the data is (latency), and whether it has been cleaned, normalised, and validated (cleanliness). Raw APIs are latency-competitive but not clean. Cleaned data products add processing overhead but remove the validation burden from the trader.

- Historical prediction market data for backtesting is available from the Gamma API going back to each market’s creation date. Tick-level historical data at high granularity requires either building your own collection infrastructure or paying a commercial provider.

- DG3 processes Polymarket’s CLOB and Gamma feeds in real time, applying fair value calculations, edge rankings, and signal classification before the data reaches the trader’s view. The raw data engineering sits inside DG3’s infrastructure, not on the trader’s side.

Why Data Latency Matters in Prediction Markets

A price update on Polymarket occurs when a transaction is confirmed on the Polygon blockchain. That update then propagates through multiple layers before it reaches a trader’s screen.

On a normal day with no catalysts, the latency through this chain is irrelevant. Prices are stable. A 2-second lag on a market that has not moved in 30 minutes costs nothing.

When an FOMC statement drops and a Polymarket rate-hold market moves 11 cents in 3 minutes, those same 2 seconds mean a different thing. If a trader is buying YES at 0.62 while the actual current price is already 0.69, they have either missed the edge that motivated the trade or paid a price that was never available.

Three scenarios where latency specifically changes outcomes:

Execution on news events. The first 60-120 seconds of a major prediction market repricing are the highest-value entry window. Stale data during this window does not slow the trade down. It turns a good entry into a bad one.

Arbitrage between correlated markets. If you are exploiting a price lag between a primary market and a correlated market, both prices need to be current simultaneously. A lagging feed on one side makes the gap invisible, and the arbitrage with it.

Automated trading systems. Any system that makes execution decisions based on price data is only as fast as its data feed. A trading bot running on a 3-second-old price is not trading the market. It is trading the market as it existed 3 seconds ago.

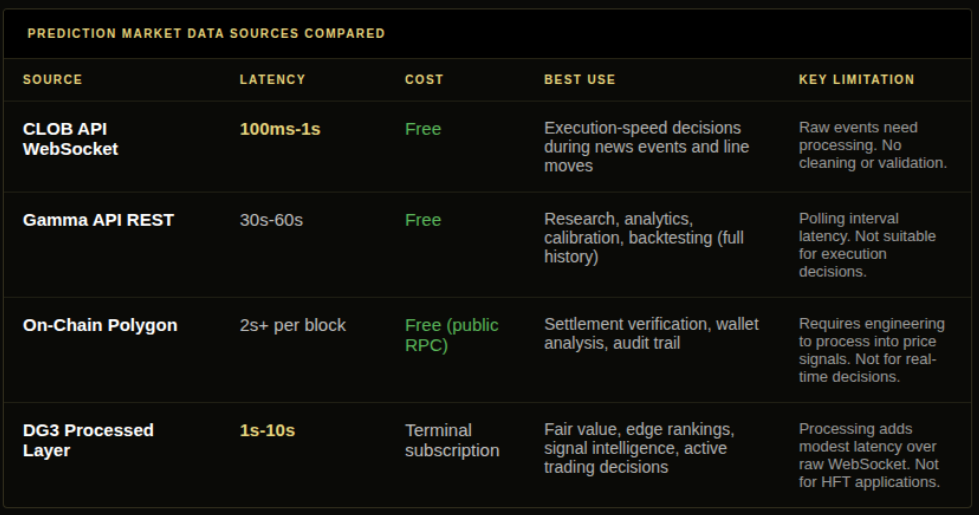

The Main Prediction Market Data Sources

Polymarket CLOB API (WebSocket)

The primary real-time data source for Polymarket. WebSocket subscription delivers price updates as each transaction occurs, with latency typically under 500 milliseconds from on-chain confirmation to feed delivery. This is the correct source for any application that needs to respond to price changes within seconds.

Authentication: read operations are public, no key required. Write operations (order placement) require wallet authentication. Cost: free.

Limitations: the WebSocket feed delivers raw order book events. Building a clean bid/ask midpoint from the raw event stream requires data processing. High-frequency connections across many markets simultaneously may need backoff logic to avoid rate limits.

Polymarket Gamma API (REST)

The primary source for historical price data, market metadata, and current price snapshots. REST polling at 30-60 second intervals is appropriate for research, calibration work, and backtesting.

Cost: free. Limitations: polling introduces latency equal to the polling interval. For a 60-second interval, data is up to 60 seconds old. Not appropriate for execution decisions during fast-moving events. The Polymarket API guide covers the full endpoint structure and practical use cases.

On-Chain Polygon Data

Every Polymarket transaction is on-chain on Polygon. This data is the authoritative source for settlement prices, wallet transaction history, and resolution confirmation. Everything else sits on top of it.

Cost: free via public RPC endpoints. Private node access for higher reliability has infrastructure cost.

Limitations: block confirmation time on Polygon is approximately 2 seconds. Processing raw blockchain data into price signals requires real engineering work. On-chain data is the right source for settlement verification and wallet analysis. For real-time price monitoring, the CLOB API is faster and more practical.

Cleaned Third-Party Data Products

Commercial providers, including DG3, process raw API and on-chain data into normalised, validated price feeds with additional analytical layers. The value is removing data engineering from the trader’s side while providing consistent, verified output.

Cost: varies by provider and tier. Research-grade access is lower cost than institutional tick data with latency SLAs.

Limitations: any processed data product adds at least some latency relative to the raw source. The question is whether the processing overhead is worth the engineering burden it removes. For most traders, it is. For high-frequency automated strategies, the SLAs need to be verified against use case requirements.

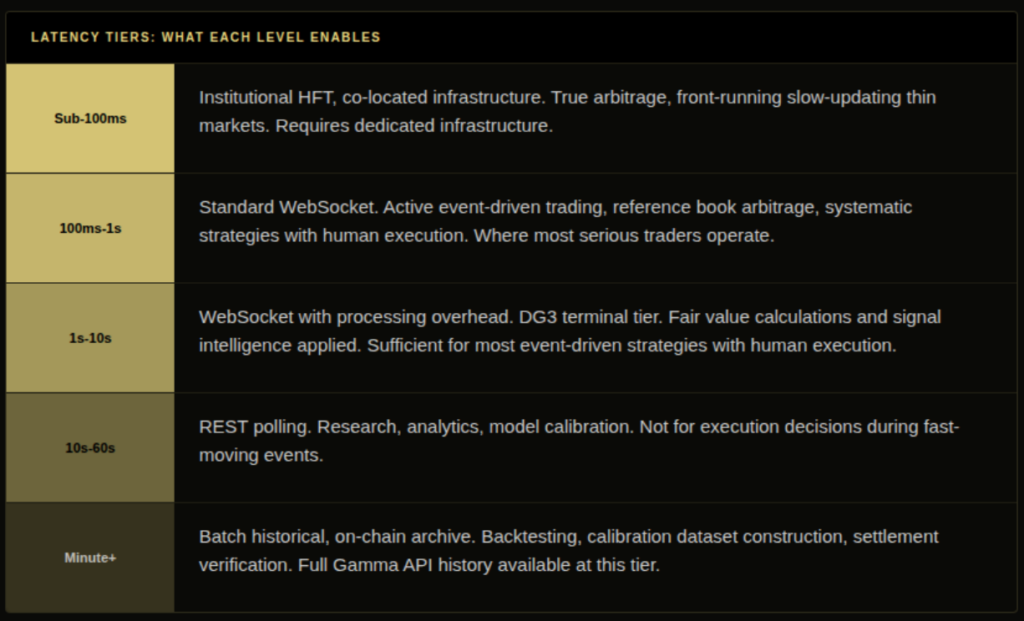

Latency Tiers: What Each Level Enables

Sub-100ms is for institutional HFT and co-located infrastructure. True arbitrage between correlated markets, front-running slow-updating thin markets. Not accessible via a standard terminal setup. Relevant for quant funds building proprietary pipelines.

100ms-1s is the practical real-time tier for most active trading applications. Standard WebSocket connection to the CLOB API operates here under normal network conditions. Fast enough for event-driven entries, reference book arbitrage, and systematic strategies with human execution.

1s-10s is where DG3’s real-time terminal operates. The WebSocket price feed is processed through fair value calculations and edge rankings before display. Sufficient for event-driven strategies where execution is human-triggered rather than fully automated.

10s-60s is REST polling territory. Appropriate for research, calibration work, and model validation. Not appropriate for execution decisions during fast-moving events.

Minute-plus is historical and batch data. Backtesting, calibration dataset construction, settlement verification. Full Gamma API history is available at this tier.

What Clean Data Actually Costs in 2026

The prediction market data landscape has two clear tiers.

Free tier: Raw access to Polymarket CLOB API and Gamma API. Full historical data from market creation. WebSocket real-time feed. No latency guarantees. No cleaning or normalisation. No cross-venue data. Appropriate for individual traders, researchers, and developers building their own processing layer.

Processed tier: Pre-cleaned, normalised price data with fair value calculations, market metadata enrichment, and analytical layer processing. DG3 provides this as part of terminal access rather than as a standalone data fee. Appropriate for active traders who want the analytical layer without building the processing infrastructure themselves.

Institutional tier: Tick-level historical data with verified latency SLAs, cross-venue normalisation across Polymarket and Kalshi, and dedicated delivery infrastructure. Priced at institutional rates, typically thousands of dollars per month for full tick history with SLAs. Appropriate for hedge funds and quant firms building systematic prediction market programs. The Prediction Market Data as Alternative Data article covers the institutional use case.

The honest reality: most traders operate on free-tier access with custom processing built on top. The gap between this and the processed tier is primarily engineering time, not cost. The gap between the processed tier and institutional tier is primarily latency guarantees and cross-venue normalisation.

Backtesting Data: Getting Historical Feeds Right

Building a prediction market model requires historical data. The Gamma API provides price history going back to each market’s creation date, which covers most research use cases.

Four challenges in backtesting with prediction market data that are easy to overlook:

Survivorship bias. Historical market listings can inadvertently over-represent markets that had sufficient volume. Thin markets with sparse price histories appear in the same dataset as liquid markets with dense histories. Mixing these in a backtest overstates the liquidity available for strategies in practice.

Resolution price accuracy. The final price at resolution is not always the same as the last traded price before the trading halt. UMA Protocol oracle resolutions on Polymarket can take time to confirm. Backtests that use last-traded-price as a resolution proxy may have small errors on markets where the final price was not 0 or 100 cents at halt.

Time zone alignment. Polymarket timestamps are UTC. Event times (sports matches, economic data releases) may be in local time zones. Misalignment between data timestamps and event timing is a common source of backtest error. Verify timestamp alignment before building any event-timing model.

Kalshi data availability. If your model incorporates cross-venue signals, you need data from both Polymarket and Kalshi. Kalshi API historical data is accessible but requires separate collection and normalisation. A naive comparison of raw price numbers from both APIs produces incorrect edge calculations because the contract structures and fee schedules differ.

Common Mistakes

Using REST polling for execution-speed-sensitive decisions is the most expensive single mistake. During a news event where a market moves 8 cents in 90 seconds, a 30-second polling interval means your data reflects prices from before most of the move occurred. Switch to WebSocket for any application where price recency matters within a 10-second window.

Treating API price as settlement price is a less obvious but meaningful error. The CLOB API price is the current mid-market price, not the settlement price. Settlement prices on Polymarket are determined by UMA Protocol at resolution, which can differ from the last traded price in markets with disputed resolutions or complex resolution criteria. Verify settlement against on-chain data for any analysis that depends on precise resolution values.

Building a backtesting model on historical data without checking latency assumptions overstates a strategy’s practical performance. A strategy that requires acting within 30 seconds of a price move needs to be backtested with data that reflects the price 30 seconds after a move, not a smoothed or OHLC representation. The speed requirement has to be built into the backtest, not assumed away.

Not accounting for Polygon gas costs in execution analysis produces cost estimates that are lower than reality. Every CLOB API write operation is an on-chain transaction. Those gas costs accumulate. A trader who made 300 trades over six months has paid gas costs that do not appear in the Polymarket P&L display. The true net return is lower than the displayed figure by the total gas paid. The Automating Polymarket Trades guide covers how to model this for systematic strategies.

How DG3 Helps

DG3’s data layer connects to the Polymarket CLOB API WebSocket and Gamma API, applies fair value calculations to each market’s current prices, and ranks markets by the size of the gap between current price and fair value. The output is a pre-processed analytical view rather than a raw price feed.

For traders who want the real-time analytical layer without building the processing infrastructure, DG3 provides it as the terminal’s core function. The fair value calculation removes the manual devig step. The edge rankings remove the need to scan across markets manually. The signal classification adds context to price movements by cross-referencing wallet quality data and reference book prices.

The raw data is free and publicly accessible. What takes time and engineering to build is the processing layer that converts it from prices into decisions. That is the layer DG3 provides.

Frequently Asked Questions

Q: Why does data latency matter in prediction markets? A: In fast-moving events, prices can shift several cents in under a minute. Acting on stale data means entering at a price that no longer reflects current market conditions. A 5-second lag during the first 60 seconds of a major repricing event can mean the difference between capturing the edge and paying the price that others already captured.

Q: What are the main prediction market data sources? A: Three primary sources. The Polymarket CLOB API WebSocket for real-time execution decisions, the Gamma API REST feed for historical data and research, and on-chain Polygon data for settlement verification and wallet analysis. Trading terminals like DG3 sit above these sources, applying processing and analytical layers before the data reaches the trader’s screen.

Q: How do raw API feeds compare with a processed data product? A: Raw APIs provide direct access to prices, order books, and market metadata at the lowest latency and no cost. They require the trader to build their own processing, normalisation, and validation layer. Processed data products add modest latency but deliver pre-normalised, validated prices with analytical layers applied. The trade-off is engineering burden versus processing overhead.

Q: What does real-time prediction market data cost? A: The Polymarket CLOB API and Gamma API are free. Processed data products with fair value calculations and edge rankings are available through DG3 as part of terminal access. Institutional-grade tick data with verified latency SLAs and cross-venue normalisation is priced at institutional rates, typically thousands of dollars per month for full tick archives.

Q: How do I get real-time Polymarket data for backtesting? A: The Gamma API provides historical price data going back to each market’s creation date at no cost. For tick-level history at high granularity, you either need to have been collecting the WebSocket feed yourself or to use a commercial data provider with historical tick archives. Verify timestamp alignment, check for survivorship bias in your market selection, and confirm that resolution prices match on-chain settlement records.

Q: What is prediction market data latency and how do I reduce it? A: Latency is the time between a price update occurring on-chain and that update arriving in your decision interface. To reduce it: switch from REST polling to WebSocket subscription, reduce processing overhead between the data feed and your decision logic, and use a provider with co-located infrastructure if sub-100ms latency is required for your use case.

Q: How does DG3 process Polymarket data? A: DG3 connects to the Polymarket CLOB API WebSocket and Gamma API, applies fair value calculations (devigging the bid-ask spread on each market), ranks markets by the gap between current price and fair value, and classifies price movements by probable cause using wallet quality data and reference book comparison. The result is a pre-processed view rather than raw price data.

Final Thoughts

Access to raw prediction market data stopped being a differentiator a long time ago. The Polymarket APIs are free, publicly documented, and comprehensive enough to support almost any research or execution use case.

What remains differentiated is the processing layer between the raw feed and the trading decision. Fair value calculations, edge rankings, signal classification, wallet quality attribution: these are the steps that convert a price feed into something a trader can act on. Each step takes engineering time to build and maintain.

The question is not which data source to use. The question is how much of that processing layer you want to build yourself, and how much you want to use infrastructure that has already built it.

The data is free. The time is not.