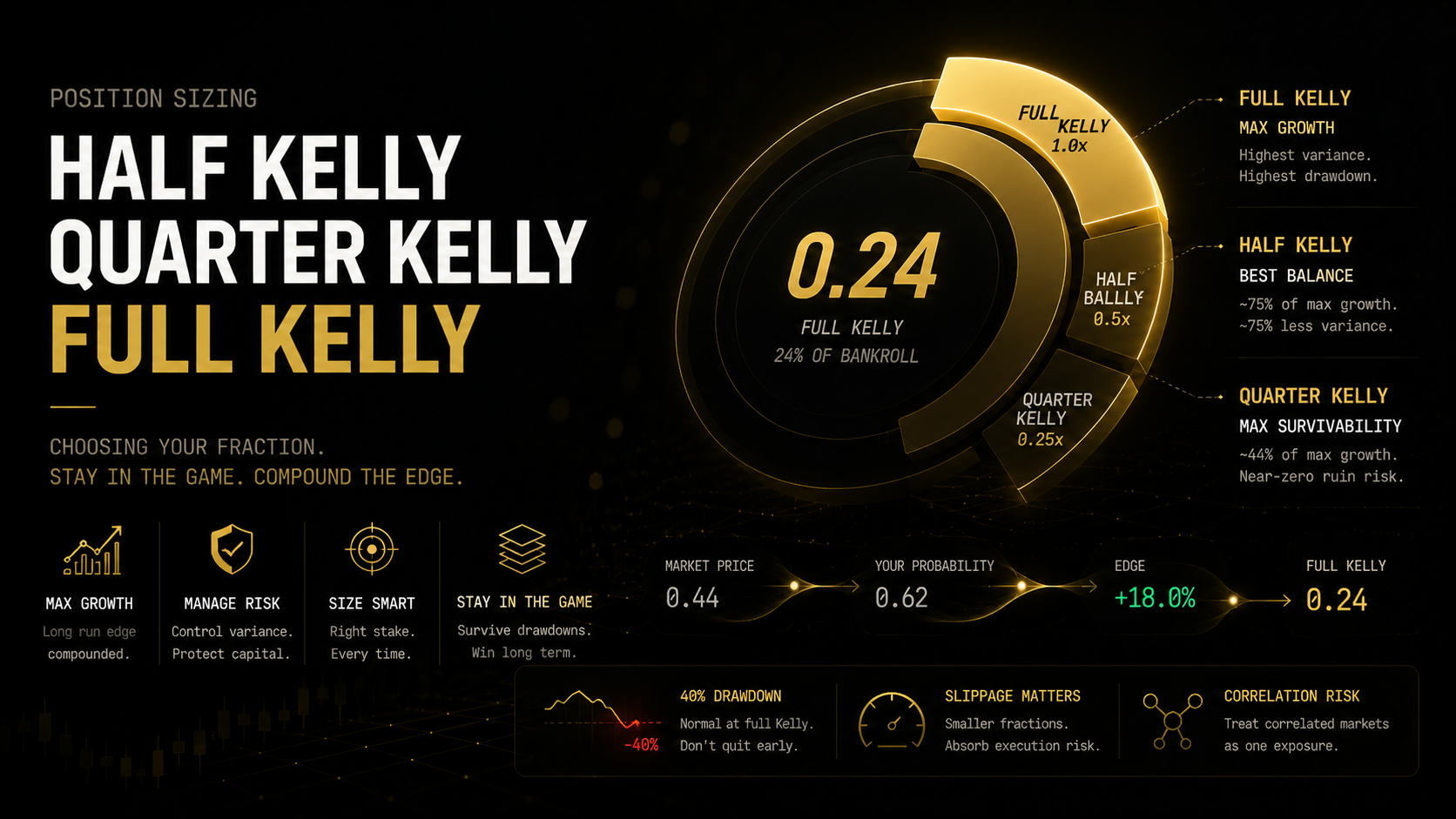

Half Kelly, Quarter Kelly, Full Kelly: Choosing Your Fraction

Full Kelly on a 24% edge means putting 24% of your bankroll on one Polymarket position. Read that again. That is not a typo, and it is exactly why almost no professional trader actually runs full Kelly with real money.

The kelly criterion tells you the theoretical maximum. Choosing your fraction is the part that decides whether you are still trading six months from now.

Quick Answer

Fractional Kelly means staking a set proportion of the full Kelly amount, most commonly 0.5x (half Kelly) or 0.25x (quarter Kelly), to account for the fact that probability estimates are never perfectly accurate. Half Kelly captures roughly 75% of maximum long-run growth while cutting variance by close to 75%, making it the standard professional default. Quarter Kelly sacrifices more growth, around 44% of maximum, in exchange for near-zero practical ruin risk.

Key Takeaways

- Full Kelly is only optimal when your probability estimate is exact, and since real-world estimates always carry error, running full Kelly with genuine confidence is closer to overconfidence than discipline.

- Half Kelly delivers roughly 75% of maximum geometric growth while cutting variance by close to 75%, an asymmetric trade that makes it the near-universal professional default rather than a conservative fallback.

- Quarter Kelly sacrifices real growth, roughly 44% of the maximum rate, but pushes practical risk of ruin toward zero, which is the correct response when your edge estimate is a judgment call rather than a calculation.

- A 40% drawdown at full Kelly is not evidence the strategy failed. It is a mathematically expected outcome over a long enough run, and most traders quit at exactly the point where the math was about to start working.

- On Polymarket specifically, smaller Kelly fractions absorb price slippage better, since a position that moves 5 cents against you during fill does less dollar damage at half Kelly than at full.

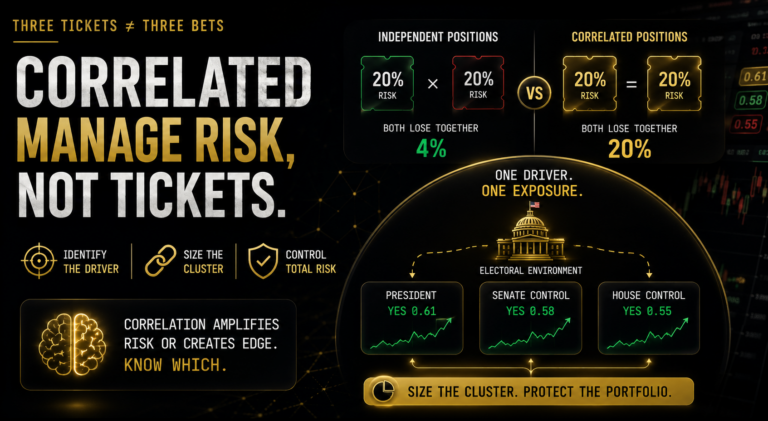

- Correlated positions must be treated as one Kelly exposure. Five markets tied to the same underlying event, each sized at quarter Kelly individually, can quietly add up to something close to full Kelly against a single outcome.

- The decision is not “how confident do I feel.” It is “how mechanically derived is this specific edge,” and that distinction should decide your fraction more than gut instinct ever should.

What Is Fractional Kelly Betting?

Fractional Kelly: Staking a fixed multiple of the theoretically optimal Kelly amount, most often 0.5x or 0.25x, to price the uncertainty in your own probability estimate directly into your position size.

The Kelly formula assumes your input probability is correct. In practice it never is, and the gap between an estimate and reality is where full Kelly stops being optimal and starts being reckless. Fractional Kelly does not abandon the framework. It adjusts for the fact that the framework’s core assumption is never fully met.

The mechanics are simple: calculate full Kelly using f* = p – q for binary markets, then multiply by your chosen fraction before converting to a dollar stake. The judgment call is choosing which fraction fits the specific edge in front of you.

The Risk Profile of Full Kelly

Full Kelly is mathematically optimal in one narrow sense: it maximises long-run geometric growth if, and only if, your probability estimate is exactly right every time.

That condition almost never holds. Real edges come from research, pattern recognition, or informational advantage, all of which carry estimation error. Full Kelly treats that error as zero, and the formula punishes that assumption harshly.

The practical consequence is variance. At full Kelly, a 50% or larger drawdown is not a tail risk, it is a normal feature of the strategy over enough trades. Most traders who experience a 40% drawdown do not conclude “this was expected.” They conclude Kelly does not work, abandon the approach, and lock in the loss right before the strategy’s long-run advantage would have shown up.

Full Kelly makes sense in one narrow case: an edge that is mechanically verified rather than estimated, where the probability input carries close to zero uncertainty. That describes almost no prediction market position.

Half Kelly: Why It Is the Default

Half Kelly (f* x 0.5) captures most of the Kelly growth benefit while absorbing the reality that estimates are imperfect.

| Metric | Full Kelly | Half Kelly |

|---|---|---|

| Growth rate vs maximum | 100% | ~75% |

| Expected maximum drawdown | Very high (50%+) | Much lower (~12-15%) |

| Variance reduction | Baseline | ~75% lower |

| Risk of ruin (long run) | Real | Very low |

| Standard professional use | Rarely | Most common default |

The 75/75 rule summarises it well: half Kelly delivers roughly 75% of maximum long-run growth for roughly 25% of the variance. Professional sports bettors, quantitative traders, and serious prediction market participants converge on half Kelly independently, which is a reasonably strong signal that it is not a hedge but a genuinely efficient trade-off.

On Polymarket, half Kelly also handles execution risk better. If your order fills 5 cents worse than the price you sized against, the dollar impact on a half-Kelly position is smaller, giving you more room to be right on direction while being slightly off on entry.

Quarter Kelly and When to Use It

Quarter Kelly (0.25x) fits situations where your edge estimate carries real uncertainty:

- You are trading a market category you have not historically calibrated on

- Your probability is a judgment call without much supporting data

- The market is thin enough that your own order flow will move the price

- You are early in your Polymarket history and do not yet know your true calibration

- The outcome has tail risk your model may not fully capture

At quarter Kelly you are explicitly saying your edge estimate could be meaningfully wrong. The growth sacrifice is real, roughly 44% of maximum, but ruin probability drops close to zero and drawdowns shrink enough that most traders can hold through a losing stretch without abandoning the approach.

Quarter Kelly is not caution for its own sake. It is the mathematically correct response to genuine uncertainty in your inputs, which is a different thing entirely.

Decision framework:

- High confidence, mechanically verified edge: 0.75x to 1.0x Kelly

- Standard confidence, model-based edge with solid data: 0.5x Kelly

- Low confidence, judgment-based edge in a new category: 0.25x Kelly

- Very uncertain, gut feel, or thin market: flat small stake or pass

Risk Profile Comparison Across Fractions

| Fraction | Growth Rate | Max Drawdown Risk | Ruin Risk | Best Use Case |

|---|---|---|---|---|

| Full Kelly (1x) | Maximum | Very high | Real | Near-certain, mechanically verified edge |

| 0.75x Kelly | ~94% of max | High | Low | High-confidence model-based edge |

| Half Kelly (0.5x) | ~75% of max | Moderate | Very low | Standard professional default |

| Quarter Kelly (0.25x) | ~44% of max | Low | Near zero | Uncertain edge, new categories |

| 0.1x Kelly | ~19% of max | Minimal | Zero practical | Learning phase / exploration |

The column that matters most in that table is max drawdown risk, because that is what actually destroys traders in practice. A 50% drawdown at full Kelly is not a catastrophic edge case, it is expected. Most people who hit a 40% drawdown quit, call it a failed strategy, and never see the fraction was the actual problem, not the framework.

How Prediction Market Traders Size Positions in Practice

Working professionals rarely apply one fixed fraction across every position. The fraction moves with the quality of the edge.

A trader with a mechanically derived arbitrage between Polymarket and Kalshi pricing on the same event might run close to 0.75x Kelly, since the edge is close to certain by construction. The same trader entering a thinly-traded niche political market based on their own read of local dynamics might drop to 0.25x, because the input probability is a judgment call with real error bars.

The skill is not memorising one number. It is correctly classifying which type of edge you are holding before you size it, and being honest when an edge that feels certain is actually just familiar.

Common Mistakes

Mistake 1: Running full Kelly because the math looks clean. Clean math on an imperfect input still produces an imperfect output. The formula’s precision does not transfer to your probability estimate.

Mistake 2: Treating quarter Kelly as “playing it safe.” Quarter Kelly is a rational response to genuine uncertainty, not timidity. Sizing it correctly protects long-run growth rather than sacrificing it needlessly.

Mistake 3: Picking a fraction once and never revisiting it. Your fraction should track the quality of the specific edge, not sit fixed regardless of whether the position is a mechanical arbitrage or a gut read on a thin market.

Mistake 4: Ignoring correlation when stacking fractional positions. Three quarter-Kelly positions on correlated outcomes are not automatically safe just because each one looks conservative in isolation.

Mistake 5: Quitting after a drawdown that was mathematically expected. A 30 to 40% drawdown at half Kelly over enough positions is not proof the approach failed. Abandoning it at that point locks in exactly the loss the framework was built to help you survive.

How DG3 Helps

Choosing a Kelly fraction is a judgment call layered on top of a calculation, and most traders either skip the judgment or skip the calculation. DG3’s Kelly Sizing Tool handles the calculation cleanly: input your fair value estimate and the live Polymarket price, and it returns full, half, and quarter Kelly dollar stakes side by side against your bankroll.

Seeing all three fractions in one view makes the judgment call easier, because you can weigh the actual dollar difference between running quarter Kelly versus half Kelly on a specific position rather than reasoning about it abstractly. The tool also tracks your total open Kelly exposure across positions, which matters more once you are running different fractions on different trades at the same time.

Frequently Asked Questions

Q: What is fractional Kelly betting? A: It is staking a fixed multiple, usually 0.5 or 0.25, of the full Kelly amount to account for estimation error in your probability input. It keeps the Kelly framework while adjusting for the fact that real-world edges are never known with certainty.

Q: When should you use half Kelly instead of full Kelly? A: Whenever your probability estimate carries meaningful uncertainty, which is nearly always. Half Kelly captures roughly 75% of maximum growth while cutting variance close to 75%, making it the practical default for research-based edges.

Q: Does half Kelly reduce variance? A: Yes, substantially. The Kelly growth curve is concave, so moving from full to half Kelly costs a moderate amount of growth but buys a disproportionately large reduction in variance and drawdown depth.

Q: What is the risk of ruin at full Kelly? A: Drawdowns of 50% or more are mathematically expected over a long sequence at full Kelly, even with genuine edge. That risk drops sharply at half Kelly and becomes close to negligible at quarter Kelly.

Q: How do professional prediction market traders size positions? A: Most vary their fraction by edge type, running higher fractions on mechanically verified edges and lower fractions on judgment-based reads in thin or unfamiliar markets, rather than applying one fixed number everywhere.

Q: Should I use half Kelly or full Kelly on Polymarket? A: Half Kelly, for almost every position. Full Kelly is only justified when your probability input is close to certain, which describes very few real prediction market edges.

Q: How do I choose a Kelly fraction when my edge estimate is uncertain? A: Drop to quarter Kelly or lower. The formula’s optimality depends entirely on input accuracy, and when that input is a judgment call rather than a calculation, a smaller fraction protects you from the cost of being wrong.

Q: What did Ed Thorp say about Kelly fractions? A: Thorp, who applied Kelly first to blackjack and then to convertible bond arbitrage, publicly preferred half Kelly for real-world capital, arguing that estimation error is unavoidable and that over-betting costs more than under-betting under the Kelly function’s concave shape.

Final Thoughts

There is no single correct Kelly fraction. There is only the correct fraction for the specific edge you are holding right now, and that changes from position to position.

The traders who last are not the ones who found the perfect number. They are the ones who got honest about how certain their edge actually was before sizing it, and who treated a 0.25x classification as a real signal rather than a failure to commit.

Half Kelly, 75% of the growth for 25% of the variance, is the closest thing to a universal starting point. Everything past that is about correctly reading your own confidence, which is harder than the arithmetic and matters more.

Read the full mechanics in Kelly Criterion for Prediction Markets and see how DG3’s Bankroll Management tools apply your chosen fraction automatically to every live position.