Negative Risk and Intra-Market Arbitrage on Polymarket

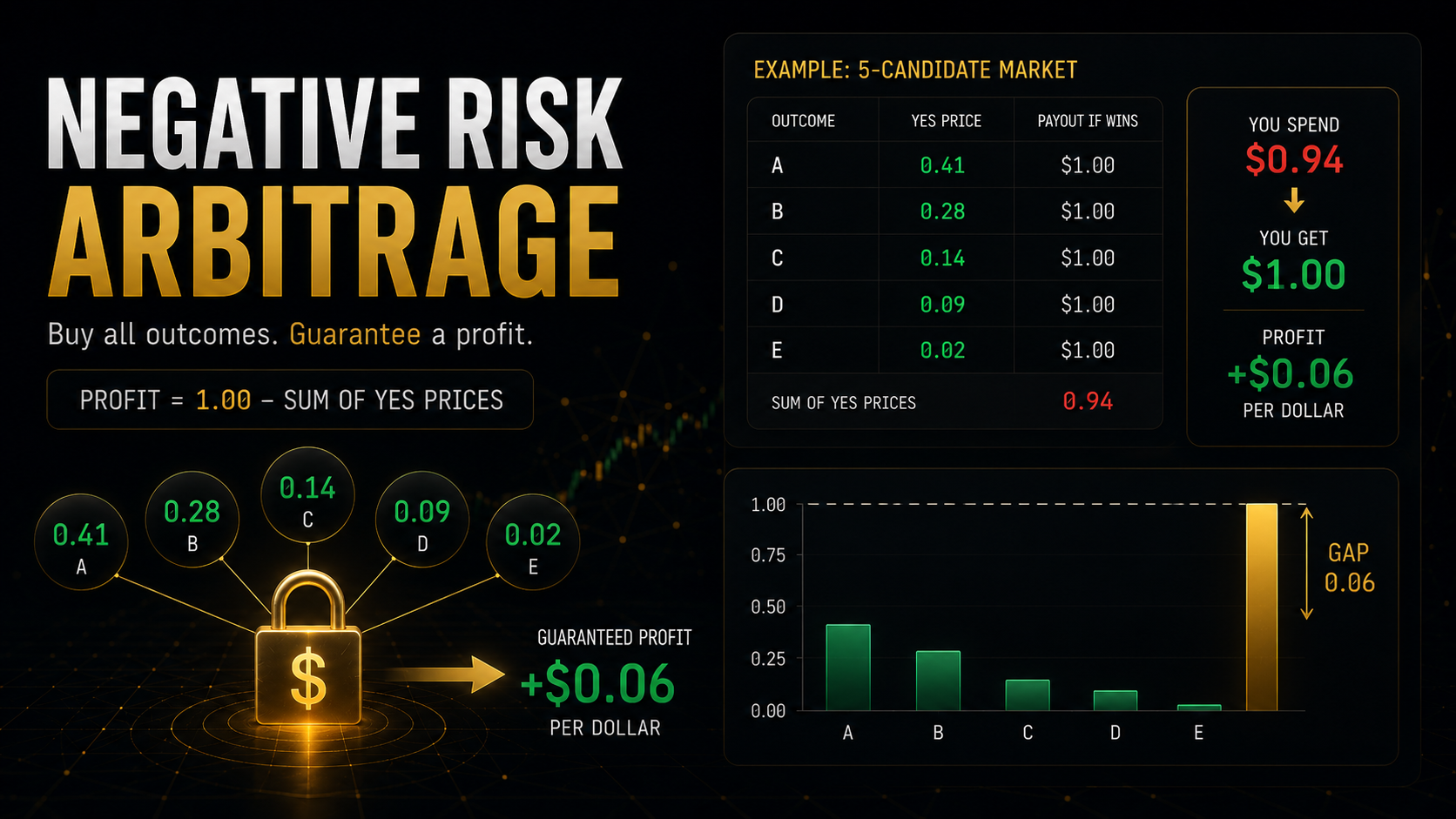

The Polymarket market had five candidates listed. Four of them were clearly priced wrong. The five YES prices added up to 0.94 cents. Someone had missed the fact that the same dollar would pay out on whichever one resolved, and you could buy all five, guarantee a return of 6 cents on the dollar regardless of outcome, and call it a day.

That is negative risk. It is rare. When it appears, it disappears fast. Understanding exactly what it is, how to find it, and what eats into the profit before you collect it is the difference between executing a genuinely risk-free trade and learning an expensive lesson about gas fees on Polygon.

Quick Answer

Negative risk arbitrage on Polymarket occurs when the YES prices across all mutually exclusive outcomes in a multi-outcome market sum to less than 1.00. Buying YES on every outcome guarantees a profit of (1 minus the sum of all YES prices) per dollar invested, regardless of which outcome resolves. In practice, this gap is rare, small, often short-lived, and partially consumed by Polymarket’s 2% fee on winning positions and Polygon gas costs. Net profitability depends on whether the margin survives those deductions.

Key Takeaways

- Negative risk exists when a multi-outcome categorical market on Polymarket has YES prices that sum below 1.00. The gap below 1.00 is the theoretical arbitrage margin before costs.

- The most common version is a winner-takes-all categorical market, where exactly one of N outcomes resolves YES and the rest resolve at zero. Buying YES on all outcomes simultaneously guarantees the full $1 payout on one contract, offset by the cost of all the others.

- Polymarket’s 2% fee on winning positions and Polygon gas costs for each transaction can together consume the entire margin on small gaps. An apparent 3-cent arbitrage can turn negative after a 2-cent fee and 0.5 cents in gas across multiple transactions.

- These gaps appear most often in newer or thinner markets before liquidity providers have had time to price all outcomes efficiently, and in categorical markets where one outcome is widely assumed to be near-certain, leaving the remaining options priced so low they collectively undershoot the 1.00 ceiling.

- Identifying a negative risk opportunity is 30 seconds of arithmetic. Executing it before it closes on a liquid market can take longer than the gap survives.

- DG3’s Market Scanner surfaces multi-outcome markets ranked by the sum of their YES prices, flagging markets where that sum falls below 1.00 as potential arbitrage candidates.

What Negative Risk Actually Means

Negative Risk: A condition in a multi-outcome prediction market where the combined cost of buying YES on every possible outcome is less than the guaranteed $1 payout, producing a risk-free profit regardless of which outcome resolves.

The term comes from the fact that your downside risk is negative. You cannot lose. The expected return is positive regardless of the outcome. In traditional finance, this kind of opportunity is called a risk-free arbitrage or a locked-in profit.

On Polymarket, the structure that makes this possible is the categorical multi-outcome market. Take a presidential primary with five candidates. Each candidate has a YES contract that pays $1 if they win and $0 if they lose. Exactly one of them will win. If you buy YES on all five for a combined cost of $0.94, you are guaranteed to receive $1 when one of them resolves YES. Your guaranteed profit: $0.06 per dollar of total stake.

The identification check is one calculation:

Sum all YES prices in the categorical market. If the sum is below 1.00, a negative risk opportunity exists at the theoretical level. Subtract 1.00 from the sum and flip the sign: that is your gross margin per dollar.

Example: a four-outcome market with YES prices of 0.41, 0.28, 0.14, and 0.09.

Sum = 0.41 + 0.28 + 0.14 + 0.09 = 0.92

Gross margin = 1.00 – 0.92 = 0.08 (8 cents per dollar, or 8% gross return)

The Fee and Gas Problem

Eight cents of gross margin sounds useful. Whether it survives to become net profit depends on two costs that most articles about arbitrage skip over.

The Polymarket 2% fee on winning positions.

When one of your YES contracts resolves at $1, Polymarket takes 2% of the profit. If you bought YES on the winning contract for 0.41, your profit on that contract is $0.59. The fee is 2% of $0.59 = $0.0118, or roughly 1.2 cents per dollar of winning position.

On a gross margin of 8 cents, that leaves approximately 6.8 cents. Still positive.

On a gross margin of 2 cents, that leaves approximately 0.8 cents. Still technically positive, but read on.

Gas costs on Polygon.

Each YES purchase is a separate on-chain transaction. Four outcomes means four transactions. Polygon gas fees are typically very low (a fraction of a cent each in normal conditions), but they are not zero. At high network congestion, gas can rise enough to matter on small margin trades. For an 8-cent margin across four outcomes, gas is usually irrelevant. For a 1-cent margin, it can flip the trade negative.

The combined cost check:

Net margin = Gross margin – Fee on winning position – Total gas across all transactions

If this number is positive, the trade works. If it is zero or negative, it does not. The Gas-Aware Betting article covers how to model Polygon transaction costs before executing.

Step-by-Step: Identifying a Negative Risk Trade

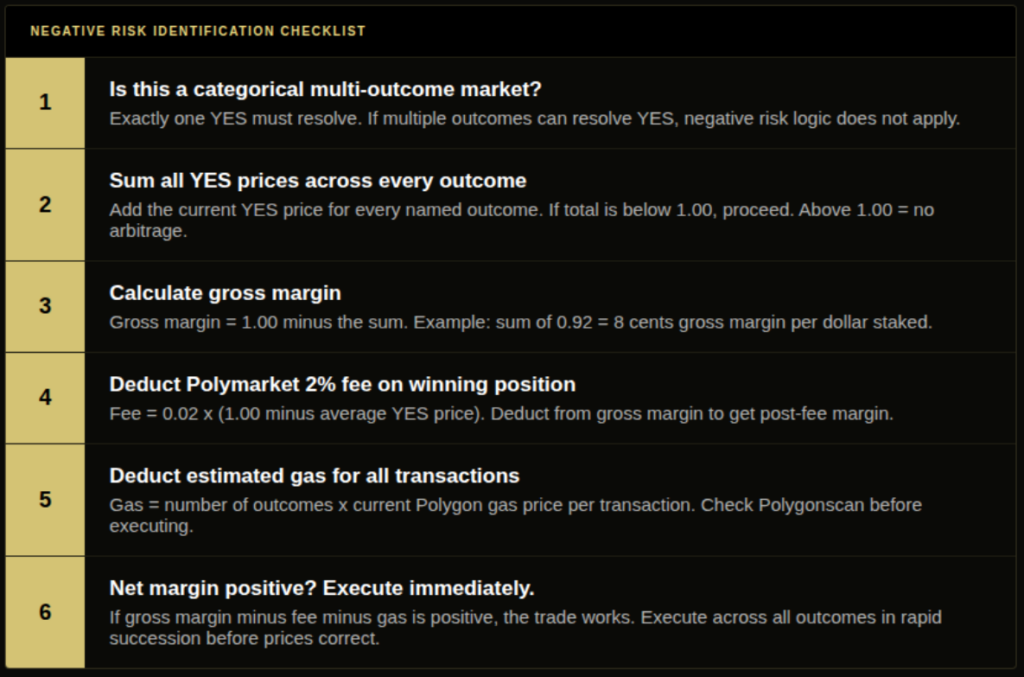

Step 1: Find a categorical multi-outcome market. These are markets where exactly one of several named outcomes will resolve YES and all others resolve at zero. Presidential primaries, tournament winner markets with a small final field, and categorical policy outcome markets are the most common structures. Simple binary YES/NO markets cannot produce negative risk by construction.

Step 2: Add up all YES prices. Navigate to the market and note the current YES price for every outcome. Add them together. If the total is below 1.00, proceed. If it is above 1.00, the market is normally priced and no arbitrage exists.

Step 3: Calculate gross margin. Gross margin = 1.00 minus the sum of YES prices. This is the profit per dollar of total stake before costs.

Step 4: Deduct the fee. The fee applies to the winning contract only. Fee cost = 0.02 x (1.00 minus the price you paid for the winning contract). Since you do not know which will win, use the average YES price as an estimate: average price = sum / number of outcomes. Fee estimate = 0.02 x (1.00 minus average price).

Step 5: Deduct estimated gas. Estimate total gas as number of outcomes x typical Polygon gas cost per transaction. In normal conditions, this is fractions of a cent total. In congestion, check current gas price on Polygonscan before executing.

Step 6: Confirm net margin is positive. If gross margin minus fee minus gas is positive, the trade is viable. If not, the arithmetic has done its job and saved you a losing execution.

Step 7: Execute quickly. These gaps close. On a liquid market, informed participants will notice and push prices up to correct the mispricing. Execute the purchases in rapid succession across all outcomes.

Why These Gaps Appear and Why They Close

Negative risk gaps form because prediction markets are not centrally priced. Each outcome in a multi-outcome market is its own order book with its own liquidity providers. When someone sells the apparent frontrunner’s YES price down without adjusting the others proportionally, or when new outcomes are added to a market that has not yet reached equilibrium, the sum of YES prices can drift below 1.00 temporarily.

The gap closes when: a trader identifies it and buys across all outcomes (pushing prices up), a market maker adjusts their quotes to reflect the full market structure, or the market’s existing liquidity providers notice the discrepancy and correct it.

On actively monitored markets, this process takes minutes. On thin markets with limited monitoring, gaps can persist for hours. The Market Efficiency guide covers the mechanics of how price corrections propagate across Polymarket markets.

Thin markets create a different problem: they create the gap, but they may not allow you to buy enough of each outcome to make the trade worth executing. If you can only buy $50 of each outcome before your buying moves prices past the arbitrage margin, the total profit on $200 of capital is $6 gross before fees. After the 2% fee, you are looking at $4.80 net, and that is before gas.

The math still works. But you are executing four transactions and monitoring five order books for $4 of profit. Know your time and effort floor before executing small arbitrages.

What Intra-Market Arbitrage Is Not

Two things that look like arbitrage but are not.

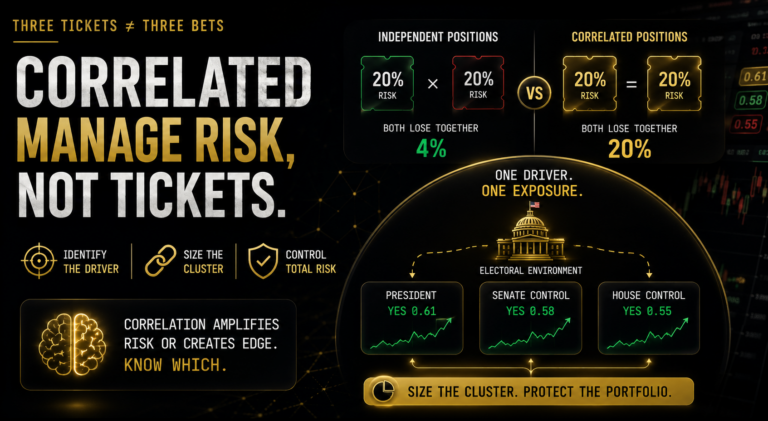

Cross-market arbitrage on the same outcome. If Polymarket has “Will X win?” priced at 0.62 YES and a correlated market on the same event is priced differently, that is not negative risk. It is a potential edge based on which market is more accurately priced. You are taking directional risk on which price corrects first. The Correlated Markets guide covers how to think about this.

Apparent mispricing in non-categorical markets. A market with YES 0.55 and NO 0.40 sums to 0.95 below 1.00 but this is the bid-ask spread, not an arbitrage. YES and NO in the same binary market are not independent contracts in the same way. The spread represents the market maker’s margin, not a gap you can capture by buying both sides.

Common Mistakes

Mistake 1: Forgetting the fee before executing. The 2% fee on winning positions is not a rounding error on small arbitrage margins. On a 2-cent gross margin trade, the fee alone on a typical 0.25 average YES price is approximately 1.5 cents. You are left with 0.5 cents, which gas will likely consume. Run the net margin calculation before every execution, not after.

Mistake 2: Executing on a market that is not truly categorical. Not all multi-outcome markets on Polymarket are winner-takes-all structures. Some pay out on multiple outcomes. Some have complex resolution criteria where two outcomes could both resolve YES. If the market is not strictly categorical (exactly one YES resolves), the negative risk logic breaks. Read the resolution criteria before assuming the structure works.

Mistake 3: Taking too long to execute across outcomes. In a liquid market, the gap you identified at Step 2 will not be the same gap at Step 7. Prices move as you buy. If your buying on outcome A pushes prices up, the gap narrows before you complete the other purchases. On thin markets this matters less; on liquid markets, execution speed is part of the viability calculation.

Mistake 4: Treating every gap below 1.00 as equivalent. A 0.5-cent gap and an 8-cent gap are not the same trade. The 0.5-cent gap is likely fee-negative. The 8-cent gap is likely worth executing. The net margin calculation is not a formality; it is what separates genuinely risk-free profit from the illusion of it.

How DG3 Helps

Finding negative risk opportunities manually means checking the YES price sums across dozens of multi-outcome Polymarket markets each day. Most will sum above 1.00. Most of the time spent is on markets that do not qualify.

DG3’s Market Scanner monitors multi-outcome Polymarket markets and flags those where the sum of YES prices falls below 1.00, ranked by the size of the gap. Instead of manually adding prices across market after market, the Scanner surfaces the candidates. The net margin calculation and execution remain yours.

When a gap appears on a thin market, DG3’s order book depth data shows how much of each outcome you can purchase before your buying moves the price past the arbitrage threshold. That capacity estimate is as important as the gap size when evaluating whether a trade is worth executing.

Frequently Asked Questions

Q: What is negative risk in prediction markets? A: Negative risk is a condition in a multi-outcome categorical Polymarket market where the combined cost of buying YES on every possible outcome is less than $1.00, guaranteeing a profit regardless of which outcome resolves. The guaranteed return equals 1.00 minus the sum of all YES prices, before fees and gas.

Q: How do you find arbitrage on Polymarket? A: Navigate to categorical multi-outcome markets, sum the YES prices across all outcomes, and check whether the total is below 1.00. If it is, a theoretical arbitrage exists. Then calculate net margin by deducting Polymarket’s 2% fee on the winning position and estimated Polygon gas costs for each transaction. If net margin is still positive, the trade is viable.

Q: Are risk-free trades possible on prediction markets? A: Yes, in specific conditions. When a categorical Polymarket market’s YES prices sum below 1.00, buying YES on every outcome guarantees a profit. In practice, these gaps are small, short-lived, and partially consumed by the 2% fee on winning positions and gas costs. True risk-free profit requires the net margin after all costs to remain positive.

Q: How does gas cost affect arbitrage viability on Polymarket? A: Each YES purchase is a separate Polygon transaction. At normal gas prices, the cost per transaction is fractions of a cent. Across four or five outcomes, total gas cost is typically under 1 cent. On a gross margin below 2 cents, however, gas can flip the trade negative. Always calculate total gas cost as number of outcomes multiplied by current Polygon gas price before executing.

Q: How does DG3 surface these opportunities? A: DG3’s Market Scanner monitors multi-outcome Polymarket markets and flags those where the sum of YES prices falls below 1.00, ranked by margin size. It also shows order book depth per outcome so you can estimate how much capital the trade can absorb before your buying moves prices past the arbitrage threshold.

Q: Why does negative risk appear on Polymarket? A: Each outcome in a multi-outcome market has its own order book and its own liquidity providers who price independently. When one outcome’s price is pushed down without corresponding adjustments across others, or when new outcomes are added before equilibrium is reached, the sum of YES prices can drift below 1.00 temporarily. The gap closes as participants buy across outcomes and push prices back toward the 1.00 ceiling.

Q: What is the difference between negative risk and a spread arbitrage? A: Negative risk is a true risk-free opportunity specific to categorical multi-outcome markets where exactly one outcome resolves YES. A spread in a binary YES/NO market (where YES plus NO sum below 1.00) is the bid-ask spread, not an arbitrage. Buying YES and NO in the same binary market does not guarantee a risk-free profit because both contracts are settled against the same single outcome.

Q: Is intra-market arbitrage legal on Polymarket? A: Yes. Buying YES contracts across multiple outcomes in the same market is standard trading activity. There are no Polymarket rules against executing across all outcomes of a categorical market simultaneously. It is a mechanical consequence of the market’s pricing structure, not a prohibited strategy.

Final Thoughts

Negative risk is the cleanest trade in prediction markets. No probability estimation required. No edge to defend. No calibration to track. The arithmetic either works or it does not.

The reason it remains worth writing about in 2026 is that it still appears, still disappears fast, and still catches traders who execute without running the net margin calculation. The 2% fee on winning positions is not optional. The gas cost is not zero. The gap that looks like free money often is, but only after those deductions confirm it.

Run the calculation. Execute quickly. Keep position sizes proportional to the gap, not to your enthusiasm for risk-free trades.

Sign up now – DG3 Terminal