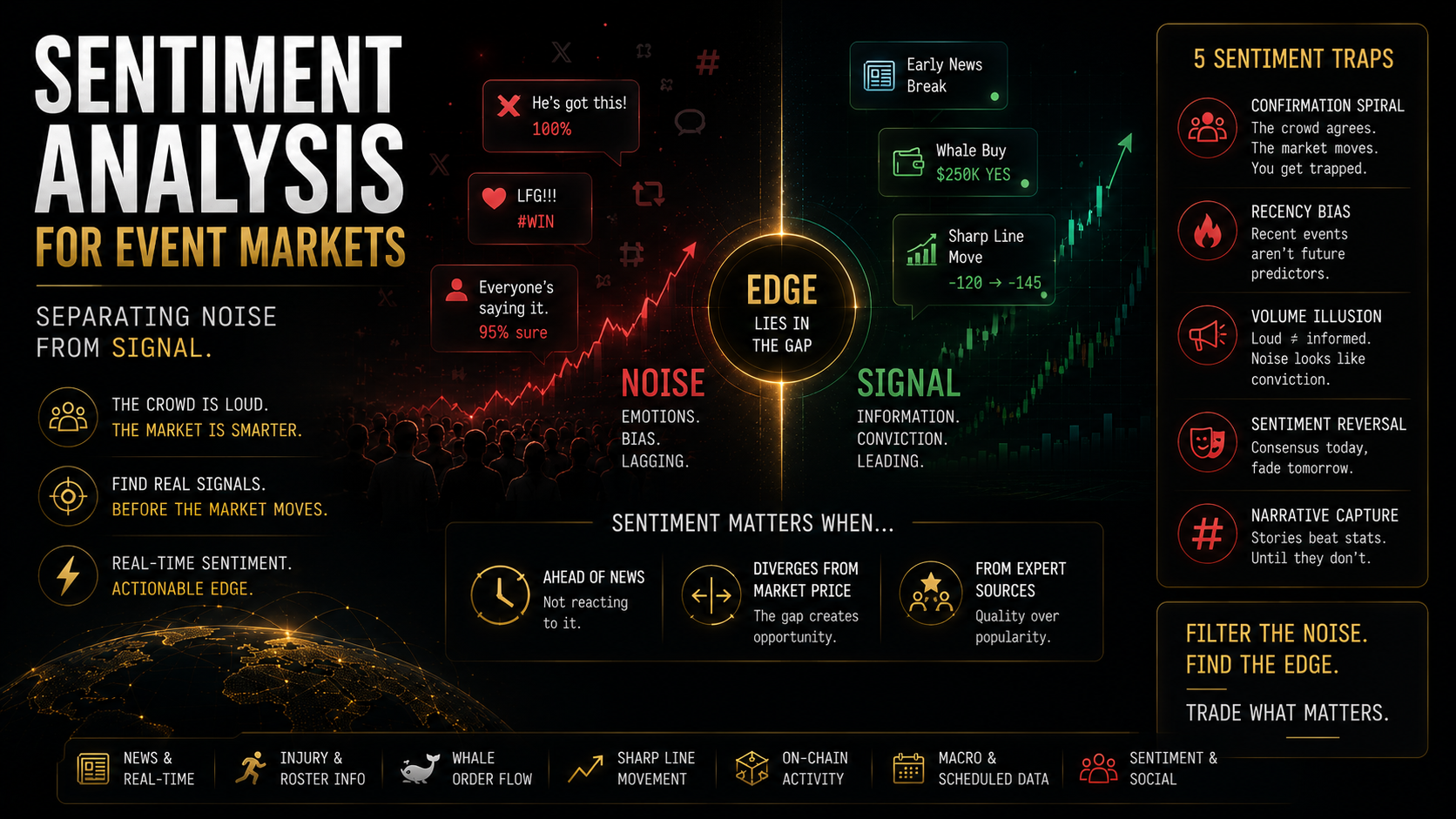

Sentiment Analysis for Event Markets: Separating Noise From Signal

Ninety minutes before the 2024 US presidential election markets closed, Twitter was overwhelmingly bullish on one candidate. The crowd was loud, confident, and largely in agreement. Polymarket prices told a different story. The sharp money and the crowd had separated, and you had to pick which one to follow.

The crowd was wrong. Not because crowd sentiment is always wrong. Because in that specific situation, the conditions under which social sentiment has predictive power were absent. Knowing the difference is the entire skill.

Quick Answer

Social media sentiment has predictive value in prediction markets only under specific conditions: when it is ahead of news rather than reacting to it, when volume reflects genuine information dispersion rather than emotional amplification, and when it diverges from current market price rather than confirming it. Most of the time, Twitter sentiment in prediction market contexts is a lagging indicator driven by retail emotion. The five most dangerous sentiment traps all exploit the same pattern: high-volume, high-confidence crowd consensus that is priced too slowly by the market and then reverses sharply when the underlying event resolves.

Key Takeaways

- Social media sentiment is a signal in prediction markets under three specific conditions: leading the news cycle, showing genuine divergence from market price, and originating from sources with domain expertise rather than general audience amplification. Most sentiment fails one or more of these conditions.

- The distinction between retail sentiment and sharp money sentiment is the most important filter in event market trading. A Reddit thread with 2,000 upvotes and an institutional research desk with $200,000 in exposure are not comparable signal sources.

- High social volume around a prediction market topic is often a contrarian indicator, not a confirmation. The highest-engagement periods around political and sports markets frequently coincide with retail sentiment that is furthest from the fundamental probability.

- Sentiment reversal is the most expensive trap: a trader follows consensus sentiment into a position, the price confirms the sentiment, and then the event resolves against the crowd. The sentiment was self-confirming (the crowd’s buying moved the price) not fundamentally informative.

- News sentiment and social sentiment are different categories that require different analytical treatment. A Reuters report and a viral tweet about the same event have different signal quality even if they carry the same directional message.

- The Sharp Money vs Public Money article covers the structural difference between these two types of market participants in detail.

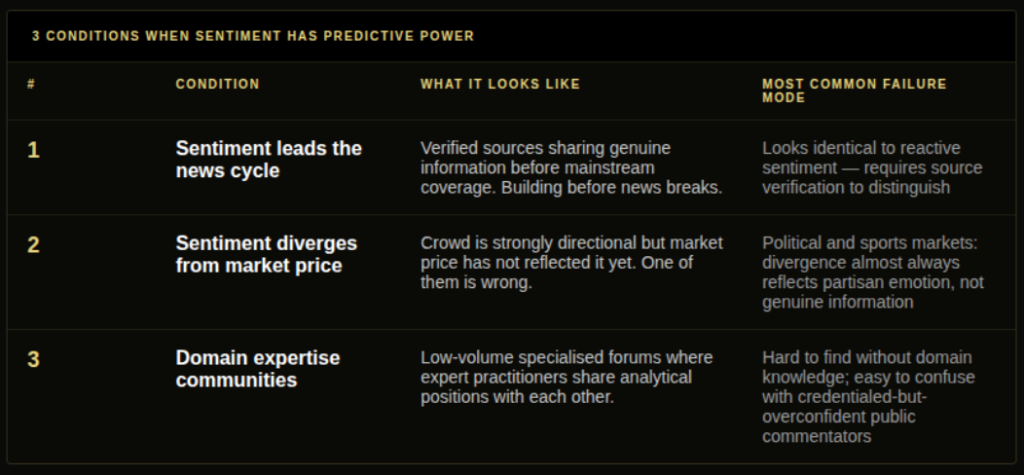

When Does Crowd Sentiment Have Predictive Power?

Most of the time, it does not. But the exceptions matter.

Condition 1: Sentiment leads the news cycle.

When social sentiment around an event is building before any mainstream news coverage, it can reflect genuine information dispersion from participants who are closer to the event. Early reporting by journalists with primary source access, information spreading through domain-specific communities before reaching general audiences, or early signals from insiders that have not yet crystallised into public news: all of these can produce leading sentiment signals.

This is rare. The vast majority of social sentiment around prediction market events is reactive, forming after news breaks and expressing the crowd’s interpretation of information that has already been reported. Reactive sentiment does not move prices. It follows them.

Condition 2: Sentiment diverges meaningfully from current market price.

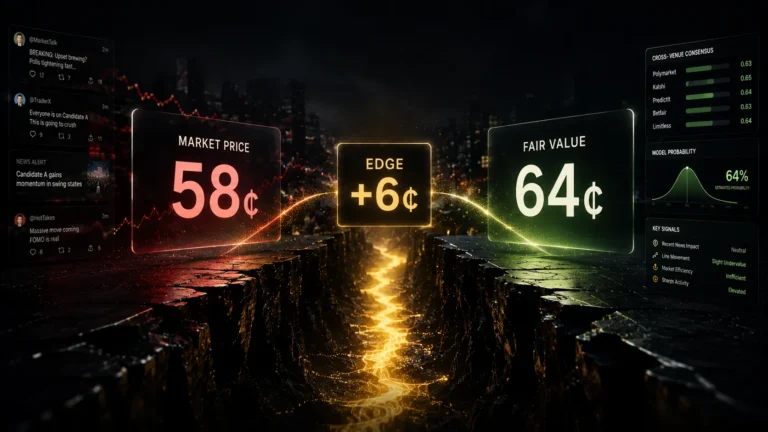

When the crowd on social media is strongly bullish on an outcome but the Polymarket price is sitting at 0.45, one of them is wrong. If the sentiment is based on genuine information (insiders, domain experts, early data) rather than emotional optimism, the crowd may be pricing correctly and the market may be lagging.

The problem with this condition is distinguishing genuine information from wishful thinking. Political and sports markets are uniquely prone to partisan sentiment that is emotionally invested rather than analytically grounded. A US presidential market where one side’s supporters are expressing 90% confidence on social media while the devigged market price says 58% is almost certainly showing partisan emotion, not information.

Condition 3: Sentiment originates from domain-specific expertise communities.

A prediction from a constitutional lawyer in a Supreme Court legal analysis forum carries different information content than the same prediction from a general political commentary account with 500,000 followers. Domain expertise communities with skin in the analytical game generate higher-quality sentiment signals than mass-audience platforms where amplification correlates with emotion rather than accuracy.

Identifying these communities takes domain knowledge itself. In football markets, scouting and tactical analysis communities. In economic markets, central banking and fixed income research communities. In political markets, district-level electoral specialists rather than national political commentators.

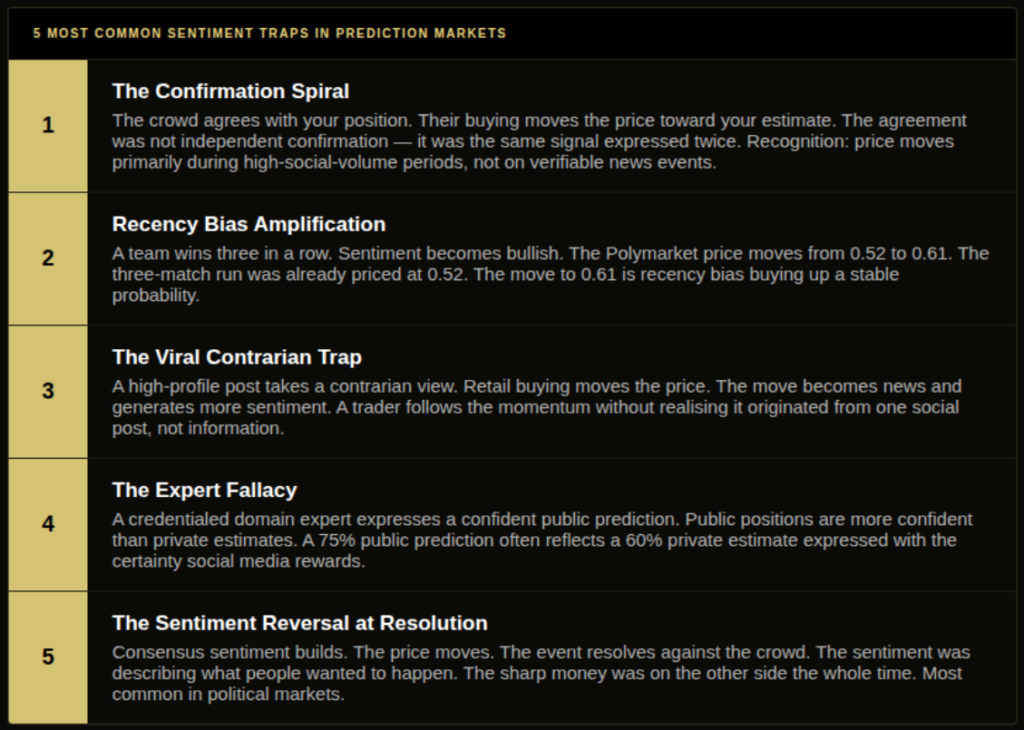

The 5 Most Common Sentiment Traps

Trap 1: The confirmation spiral.

You form a probability estimate. You check Twitter. The crowd agrees with you. You size up. The crowd’s buying (not your analysis) is pushing the price toward your estimate. When the event resolves against the consensus, it turns out the crowd was pricing itself in a feedback loop, not processing new information. Your analysis and the crowd’s agreement felt like two independent confirmations. They were the same signal expressed twice.

Recognition: if your position’s price moves in your direction primarily during high-social-volume periods rather than in response to verifiable news or data events, you may be in a sentiment spiral rather than an informed position.

Trap 2: Recency bias amplification.

A team wins three matches in a row. Social sentiment becomes extremely bullish. Their Polymarket match winner market moves from 0.52 to 0.61. The three-match run was public information throughout. The price at 0.52 already reflected the historical form. The move to 0.61 is the crowd’s recency bias buying up a price that the market had already correctly set.

Recency bias amplification is easiest to spot in sports markets where recent results drive disproportionate sentiment shifts on probabilities that have not fundamentally changed.

Trap 3: The viral contrarian trap.

A high-profile commentator takes a contrarian position on a prediction market. The post goes viral. It generates enough retail buying in the contrarian direction that the price actually moves. Now the move itself becomes news and generates more sentiment. A trader who observes the price move and interprets it as confirmation of new information is following momentum driven by a single high-reach social post, not by any fundamental update.

The tell: a price move that is large relative to the market’s normal volatility but is not accompanied by any verifiable news event or order flow from historically accurate wallets.

Trap 4: The expert fallacy.

A domain expert with genuine credentials expresses a confident prediction on social media. The post gets wide distribution. Traders weight it heavily because of the source’s credibility. The expert is forecasting outside their area of genuine edge, or their publicly expressed view differs from their private analytical model.

Public forecasting by domain experts carries selection bias: the positions people express publicly tend to be more confident and less qualified than their private probability estimates. A 75% public prediction from a credible source often reflects a 60% private estimate expressed with the certainty that social media rewards.

Trap 5: The sentiment reversal at resolution.

The most expensive trap. Consensus sentiment has been building for days. The market price has moved to reflect it. You are in the position and watching the sentiment confirm your view. Then the event resolves against the crowd. The sentiment was not predictive. It was describing what people wanted to happen, and the wanting was loud enough to move prices.

Sentiment reversals at resolution are particularly common in political markets. They are the mechanism by which partisan money consistently loses to sharp money over large samples. The Information Asymmetry guide explains why informed participants systematically take the other side of sentiment-driven positions.

Retail Sentiment vs Sharp Sentiment: The Only Distinction That Matters

Crowd sentiment has no consistent predictive value. Sharp sentiment (the expressed positions of consistently accurate forecasters) does.

Retail sentiment is characterised by: high social amplification, emotional investment in outcomes, recency bias, partisan framing, and updating slowly after disconfirming evidence. It is the majority of what appears in searches for prediction market sentiment signals.

Sharp sentiment is characterised by: low social volume, probabilistic framing rather than confident directional assertions, explicit uncertainty acknowledgement, rapid updating when new information arrives, and a track record that can be evaluated.

The practical problem is that sharp sentiment is mostly private. The traders with real edge do not post their positions on Twitter. What is publicly expressed is almost entirely retail sentiment, which means most social media sentiment signals are capturing the noise layer rather than the information layer of the market.

The exception is in specialised domain communities where expert practitioners share genuinely analytical positions with each other. These communities are harder to find and require domain knowledge to evaluate. When you find them, they carry substantially better signal quality than mass-market sentiment platforms.

Does Twitter Sentiment Predict Polymarket Prices?

Sometimes yes. Usually no. The conditions matter.

Research on prediction market sentiment relationships consistently shows that social media volume and directional sentiment have weak predictive power on average, with meaningful predictive power in a narrow set of circumstances. High social volume is, if anything, a mild contrarian indicator on political markets because it correlates with partisan retail participation rather than informed capital.

The cases where Twitter sentiment has shown leading predictive power:

Early-cycle information dispersion, where verified accounts with primary source access are sharing genuine new information before it reaches mainstream outlets. This looks identical to reactive sentiment in the moment and requires source verification to distinguish.

Domain expert communities on specialised platforms (private groups, subpages, Substacks) where the signal-to-noise ratio is higher than on general social media. These generate less volume but carry more information per unit of content.

Sentiment divergence between different market venues. When one platform’s price has moved in response to a sentiment signal and another has not, the lag is informative regardless of whether the sentiment itself was predictive.

Common Mistakes

Mistake 1: Using Twitter volume as a proxy for signal strength. High tweet volume about a prediction market event means the topic is salient to a broad audience. It says nothing about the directional accuracy of the crowd’s assessment. On political and sports markets, the highest-volume sentiment periods frequently precede the largest market corrections.

Mistake 2: Treating a confident social media post as an independent probability update. When you see a confident social media prediction about a market you are analysing, it is not a new data point unless you can verify the source has genuine domain expertise and a track record. A confident post from an unknown account adds near-zero information to your probability estimate. A confident post from a domain expert with verifiable credentials and a good forecasting record adds something worth weighing.

Mistake 3: Updating probability estimates based on sentiment rather than underlying information. Crowd sentiment expressing 80% confidence does not change the underlying probability of an event. The event has a true probability that exists independently of how many people tweet about it confidently. If your probability estimate was 55% before the sentiment wave and remains 55% after it (because no new factual information has arrived), the sentiment should not move your estimate.

Mistake 4: Not distinguishing between sentiment moving the price and information moving the price. When a Polymarket market moves 6 cents, it can be because informed capital entered (information signal) or because retail sentiment buying pushed the price (sentiment signal). These two causes have different implications for whether the move represents a genuine probability update or a temporary sentiment-driven displacement. Whale tracker data and sharp line movement context help distinguish the two.

Mistake 5: Ignoring sentiment entirely because it is usually noise. The five conditions where sentiment has genuine predictive value are narrow but real. A trader who ignores all social signals loses access to early information dispersion events, contrarian price corrections, and expert community forecasts that occasionally lead markets. The skill is selective filtering, not blanket dismissal.

How DG3 Helps

DG3’s Signal Layer includes sentiment signals filtered by source quality and linked to specific Polymarket markets. Rather than monitoring a global social feed and attempting manual signal extraction, DG3 shows sentiment events connected to active positions and highlights when social sentiment is diverging from current market price in a way that has historically been informative.

The integration with whale order flow and sharp line movement means you can evaluate sentiment signals in context: when a sentiment signal aligns with a whale entry and a sharp line move, it carries more weight. When sentiment runs counter to whale flow, the default should be the whale signal. Trading Signals That Actually Move Event Markets covers the full signal hierarchy in detail.

Frequently Asked Questions

Q: Does Twitter sentiment predict Polymarket prices? A: Weakly and conditionally. On average, Twitter sentiment has low predictive power for Polymarket price movements. In specific conditions, it has genuine predictive value: when sentiment leads the news cycle, when it reflects genuine domain expertise rather than mass-audience amplification, and when it diverges meaningfully from current market price. High Twitter volume on political and sports markets is, if anything, a mild contrarian indicator because it correlates with retail participation rather than informed capital.

Q: When does crowd sentiment have predictive power in event markets? A: Under three specific conditions: when it is ahead of the news cycle (reflecting early information dispersion from sources close to the event), when it diverges from current market price in a way that reflects genuine information rather than emotional optimism, and when it originates from domain-specific expert communities with a track record of accuracy rather than from general social media amplification.

Q: When should you ignore social sentiment in prediction market trading? A: When it is reactive (forming after news has already broken), when volume is high but source quality is low (viral tweets from non-expert accounts), when it aligns with partisan or emotional investment rather than analytical probability assessment, and when it confirms your existing position rather than offering independent information. Sentiment that makes you feel more confident in a position you already hold is not an independent signal.

Q: How do you distinguish retail from sharp sentiment in event markets? A: Sharp sentiment is characterised by probabilistic framing, explicit uncertainty acknowledgement, rapid updating when disconfirming evidence arrives, and a track record that can be evaluated over time. Retail sentiment is characterised by high volume, confident directional assertions, slow updating after disconfirming events, and partisan or recency-biased framing. Most of what appears on general social media is retail sentiment. Sharp sentiment is mostly private or in specialised low-volume communities.

Q: What are the five most common sentiment traps in prediction markets? A: The confirmation spiral (crowd agreement with your existing position is not independent confirmation), recency bias amplification (recent results driving disproportionate sentiment on stable probabilities), the viral contrarian trap (a single high-reach post generates momentum that looks like information), the expert fallacy (publicly expressed expert confidence is more certain than private estimates), and the sentiment reversal at resolution (partisan or emotional consensus that prices itself in and then collapses when the event resolves against the crowd).

Q: How does sentiment analysis differ from trading signals for event markets? A: Trading signals (news, whale order flow, sharp line movement, macro data) have direct probability implications that can be evaluated against fundamental information. Sentiment analysis is a second-order layer: it reads the crowd’s interpretation of information rather than the information itself. Signals tell you what happened and what it implies. Sentiment tells you what the crowd thinks happened and what they think it implies. The latter requires an additional layer of filtering to distinguish genuine information from crowd noise.

Q: What is a sentiment reversal and why is it expensive? A: A sentiment reversal occurs when crowd consensus builds around an outcome, the market price moves to reflect it, and then the event resolves against the consensus. The price correction on resolution is often sharp because sentiment-driven positions unwind simultaneously. A trader who followed the sentiment into the position experiences both the wrong outcome and the amplified price move as the crowd exits. Sentiment reversals are most common in political markets where partisan sentiment is strong.

Final Thoughts

The honest answer about social sentiment in event market trading is that it is mostly noise with occasional signal buried inside.

The traders who use sentiment well are not the ones who monitor the most platforms or track the highest volume conversations. They are the ones who have built a clear model of when sentiment carries genuine information and when it is just the crowd talking to itself. That model is narrower than most traders expect. The conditions are specific. The exceptions are real but rare.

The default should be skepticism. The exception should be carefully verified. Most of the time the sharp money is not following the crowd. It is taking the other side of it.

For the Bayesian Updating framework on how to incorporate new information correctly when sentiment and data conflict, the article covers the mechanics in detail.

Sign up now – DG3 Terminal