Bayesian Updating in Prediction Markets: Revise Probabilities as News Breaks

The injury report drops. The star player is questionable, not out. Half the market treats “questionable” like “out” and dumps their position. The other half barely moves. Neither reaction is Bayesian. Bayesian updating is the specific, disciplined middle path that most traders skip entirely because it takes more thought than a gut reaction and less time than they think.

Getting this right, consistently, across enough positions, is one of the more underrated edges available to anyone trading event markets.

Quick Answer

Bayesian updating is the process of revising a probability estimate in light of new evidence, using your prior belief and the strength of the new information to calculate an updated, or posterior, probability. In prediction markets, it prevents two common errors: overreaction, where traders treat new information as more conclusive than it actually is, and underreaction, where traders anchor too heavily to their original estimate and fail to move enough. The size of the correct update depends on how strongly the new evidence actually discriminates between the possible outcomes, not on how dramatic the news feels.

What Is Bayesian Updating in Prediction Markets?

Bayesian updating starts with a prior, your existing probability estimate before new information arrives, and combines it with the strength of new evidence to produce a posterior, your updated estimate afterward. The core equation, Bayes’ theorem, formalizes this: posterior probability is proportional to your prior probability multiplied by the likelihood of seeing this specific evidence given each possible outcome.

The plain-language version matters more than the formula for most trading decisions: how surprising is this piece of news, given what you already believed, and how much more likely does it make one outcome over the other. A piece of news that would be equally likely to appear whether the event happens or not carries almost no updating power, regardless of how dramatic it sounds. A piece of news that would only plausibly appear if a specific outcome were true carries real updating power, even if it seems minor on the surface.

This is the actual skill. Most people update based on how emotionally loaded news feels rather than how much it genuinely discriminates between outcomes, and that mismatch is where a large share of retail trading mistakes originate.

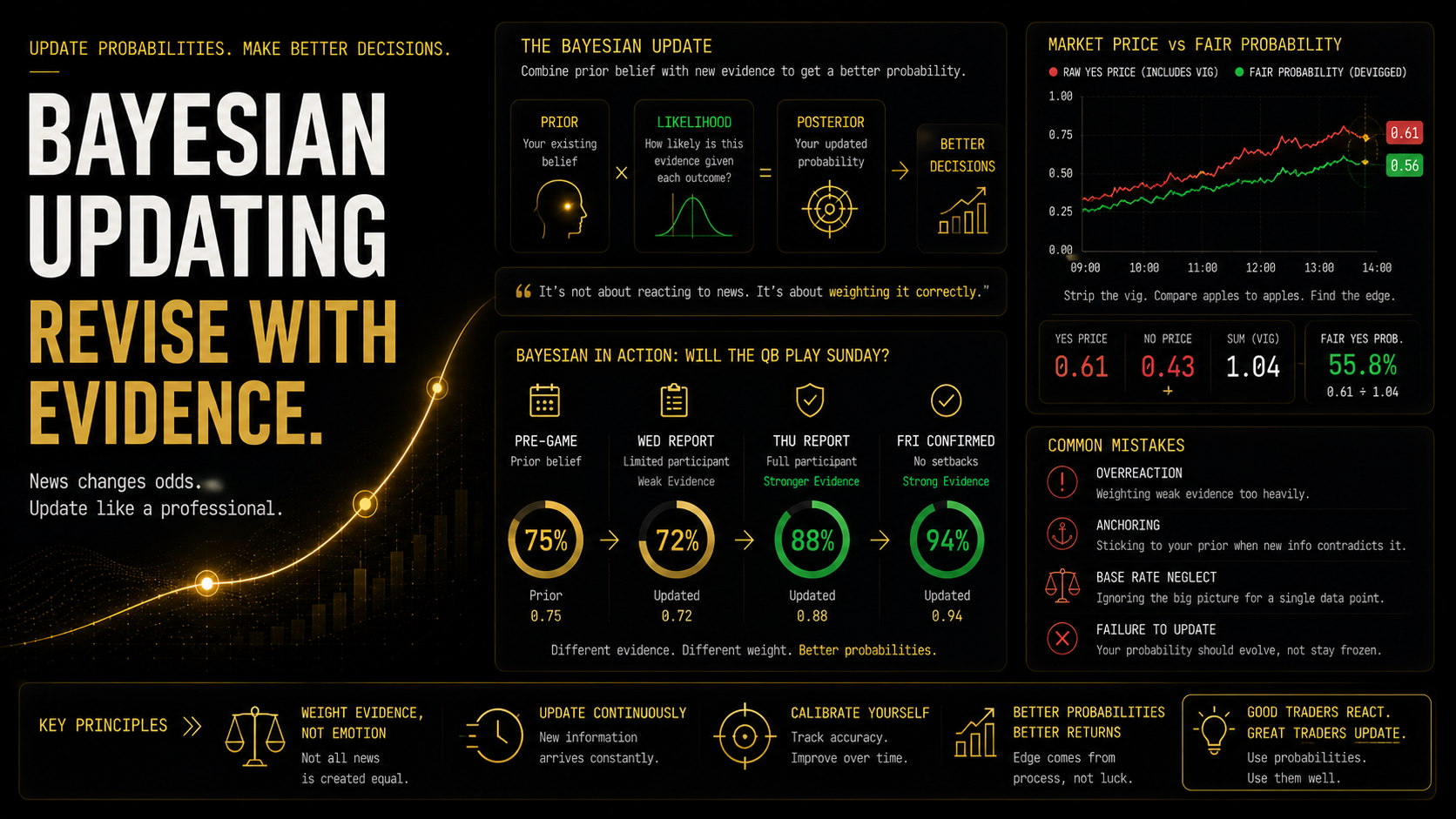

The Bayesian Update in Practice: A Worked Example

Say a market on “will the starting quarterback play in Sunday’s game” trades at a devigged 75% probability heading into the week, based on his recovery timeline from a minor injury. Wednesday’s practice report lists him as a limited participant.

A limited practice participation report is evidence, but it is fairly weak evidence on its own, since players are frequently listed as limited early in the week and still start. If your model estimates that a starter in this recovery stage shows up as “limited” on Wednesday roughly 70% of the time whether or not he ultimately plays, that piece of news barely shifts your probability, maybe from 75% down to 72%.

Thursday’s report lists him as a full participant. That carries meaningfully more weight, since full participation two days before a game is much more strongly associated with actually playing than not. Your updated probability might move from 72% to 88%.

Compare that to a hypothetical scenario where Wednesday’s report says he was pulled from practice entirely with visible discomfort. That is much stronger evidence, since that specific event is far more likely to occur in a world where he ultimately sits out than one where he plays, and a properly Bayesian trader would drop their probability sharply on that specific piece of news, not gradually.

The mechanical lesson: the size of your update should track the actual discriminating power of the evidence, not the emotional weight of the headline describing it.

4 Common Over-Updates and Under-Updates

Overreacting to news that does not actually discriminate well between outcomes. A vague or ambiguous report gets treated as decisive simply because it arrived, when its actual evidentiary weight is low.

Underreacting to genuinely strong evidence because it contradicts your original position. Traders who have already taken a position sometimes discount new evidence that would require admitting the original read was wrong, holding their probability estimate closer to the prior than the evidence justifies.

Base rate neglect. Ignoring the general frequency of an event type in favor of a specific, vivid piece of information. A single dramatic headline about a rare event type can override a well-established base rate that deserved more weight than it got.

Failing to update at all once a position is open. Some traders form an initial thesis, take the position, and then stop actively revising their probability estimate as new information arrives, effectively freezing their prior at entry regardless of what happens afterward.

How Bayesian Updating Connects to Market Prices

Market prices themselves function as a running, aggregated Bayesian update, shifting continuously as the collective body of participants absorbs new information. A price moving from 40 cents to 55 cents after a news event is the market’s version of a posterior update, reflecting the combined reaction of every participant who traded in response to that specific piece of news.

This creates a genuinely useful trading signal for anyone who can update more accurately than the aggregate market. If your own Bayesian update, based on a correct read of how strongly a piece of evidence discriminates between outcomes, differs meaningfully from where the market price actually moved, that gap is your edge. It might mean the market overreacted to weak evidence, creating a fade opportunity, or underreacted to strong evidence, creating a same-direction opportunity before the price fully catches up.

Common Mistakes

Most updating errors run in one of two directions. The first is overreacting: treating all news as equally weighted evidence, when a headline that generates a strong emotional reaction is not automatically strong evidence. The correct update size depends on how well the specific information discriminates between outcomes, not how attention-grabbing it is. Base rate neglect sits in the same bucket, where a single compelling anecdote or vivid recent example distorts a probability estimate away from a well-established base rate that deserved more weight than it got.

The second direction is underreacting, and it is the harder one to catch in yourself. Anchoring too hard to your original prior means interpreting every subsequent piece of evidence in a way that confirms what you already believed, rather than genuinely revising when the evidence points somewhere else. Under real pressure, this can flip into the opposite failure just as easily: updating in the wrong direction entirely, where a panic-driven reaction to news against an open position produces a move that the evidence itself does not actually support, driven by loss aversion rather than probability reasoning.

How DG3 Helps

Bayesian updating done well requires processing new information quickly and weighing it correctly against your existing view, which is difficult to do consistently under time pressure, especially during a live, fast-moving event.

DG3’s live news feed inside the Intelligence Pane scores incoming developments for their likely model impact on the specific market you have open, giving you a starting estimate of how strongly a given piece of news should move your probability rather than leaving that judgment entirely to instinct in the moment. Paired with the Fair Value Engine’s continuously updated devigged probability, you get a clear read on whether the market’s own aggregate update has already caught up to a piece of news or is still lagging behind it.

Frequently Asked Questions

Q: What is Bayesian updating in trading? A: It is the process of revising a probability estimate based on new evidence, combining your prior belief with the strength of the new information to produce an updated posterior probability. It provides a disciplined structure for reacting to news rather than relying on instinct alone.

Q: How do you update predictions with new information correctly? A: By assessing how strongly the new information actually discriminates between possible outcomes, rather than reacting to how dramatic or emotionally loaded it feels, and adjusting your probability estimate proportionally to that discriminating power.

Q: What is base rate neglect in prediction markets? A: It is the tendency to ignore the general frequency of an event type in favor of a specific, vivid piece of information, which can distort a probability estimate away from a well-established, statistically grounded baseline.

Q: How does injury news change a sports prediction market price? A: The size of the price movement should reflect how strongly the specific injury report discriminates between the player playing and not playing. A vague or ambiguous report should move the price less than a definitive one, though markets do not always get this calibration right in the moment.

Q: What is overreaction in prediction market trading? A: It is treating a piece of news as more conclusive than its actual evidentiary strength justifies, producing a probability update larger than the evidence supports.

Q: What is underreaction in prediction market trading? A: It is failing to move your probability estimate enough in response to genuinely strong evidence, often because of anchoring to an original view or reluctance to abandon an existing position’s thesis.

Q: How does Bayesian thinking apply to sports betting and prediction markets? A: Both require continuously revising probability estimates as new information, like injury reports, weather, or lineup changes, arrives, weighing each piece by how much it actually discriminates between outcomes rather than by how prominently it is reported.

Q: Why do prediction market prices sometimes overreact to news? A: Because a large share of participants react to the emotional or narrative weight of a headline rather than calculating its actual evidentiary strength, producing a price move larger than the information genuinely justifies, often followed by a partial correction.

Final Thoughts

Bayesian updating is not a formula you calculate exactly every time. It is a discipline: pausing before reacting to new information and asking how much this specific piece of evidence should actually move your probability, given how likely it would be to appear regardless of which outcome turns out to be true.

Most market overreactions and underreactions trace back to skipping that pause. The traders who consistently read news well are not necessarily faster than everyone else. They are more accurate at sizing their reaction to match the real evidentiary weight of what just happened, which is a skill built through repetition, not an inherent talent.

Read how Sharp Money vs Public Money tends to diverge specifically at the moment new information hits a market.