Implied Probability Calculator: Read Prediction Market Prices as Probabilities

A YES contract at 61 cents is not “61% likely to happen” in the clean way most people assume. Part of that price is probability. Part of it is the platform’s built-in margin, sitting quietly inside a number that looks like a straight probability read. Strip that margin out and you get something closer to the truth, and most traders never bother to check the difference.

That gap between raw price and fair probability is small on any single position and compounds into real money across a hundred of them.

Quick Answer

Market-implied probability is the probability of an event occurring as reflected by the current market price, but the raw YES price includes platform vig and cannot be read as pure probability without adjustment. Devigging removes that margin to produce a fair probability estimate, calculated by normalizing YES and NO prices so they sum to exactly 100%. Devigged implied probability serves as an active trading reference, updating within minutes as new information arrives, in contrast to slower-moving polling averages or expert panel forecasts.

What Is Market-Implied Probability?

If a YES contract trades at 72 cents, the naive read is that the market believes the event has a 72% chance of happening. That is directionally right but not exactly correct, because YES and NO prices on most platforms do not sum to exactly 100 cents. The small difference is the platform’s built-in margin, sometimes called the vig or overround, and it means the raw price slightly overstates the market’s true probability estimate on both sides at once.

The word “implied” matters here. The market is not asserting a verified probability. It is reflecting the aggregate belief of everyone currently trading, filtered through whatever margin structure the platform uses, and that raw number needs one more step before it becomes a genuinely useful probability estimate.

The Devig Formula: Step-by-Step

Devigging is the process of removing platform margin to recover the fair, normalized probability implied by the market.

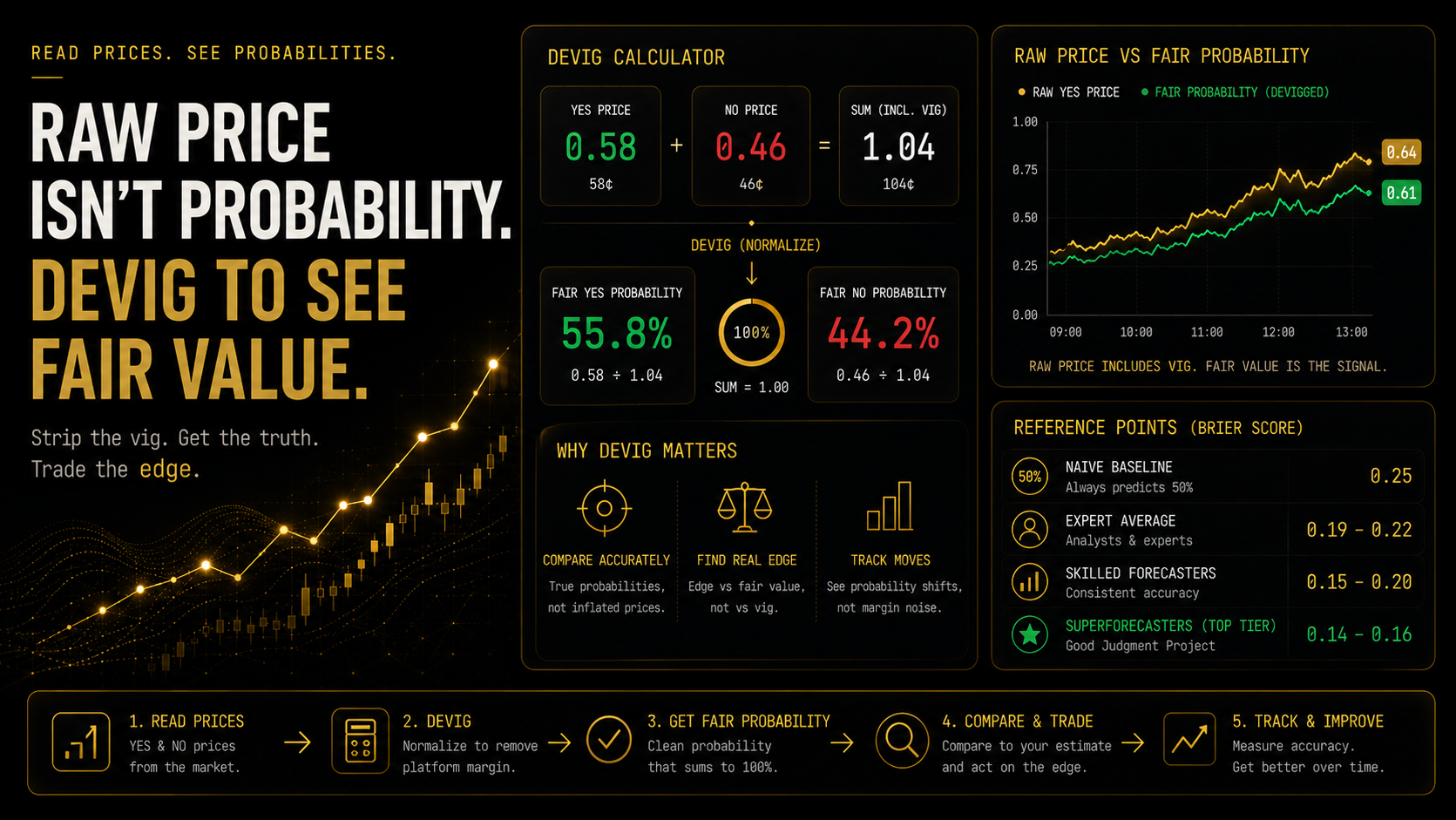

Step 1: Note the YES price. Say YES trades at 0.58.

Step 2: Note the NO price. On the same market, NO might trade at 0.46. Notice these sum to 1.04, not 1.00. That extra 0.04 is the vig.

Step 3: Sum both prices. 0.58 + 0.46 = 1.04.

Step 4: Divide each price by the sum to normalize. Fair YES probability = 0.58 / 1.04 = 0.5577, or roughly 55.8%. Fair NO probability = 0.46 / 1.04 = 0.4423, or roughly 44.2%. These now sum to exactly 100%.

The devigged number, 55.8%, is a more accurate read of the market’s actual probability belief than the raw 58 cent price, because it strips out the margin that inflates both sides. On liquid markets with tight spreads, this adjustment is small, often a percentage point or two. On thinner markets with wider spreads, the gap between raw price and devigged probability can be meaningfully larger, which is exactly where skipping this step costs traders the most.

Implied Probability as a Trading Signal

Once you have a clean, devigged probability, it becomes useful in three specific ways beyond simply reading the current market sentiment.

Comparing your own estimate against fair value. If your independent research suggests 68% and the devigged market probability is 56%, that 12 point gap is your calculated edge, not the raw price gap, which would have understated the true difference.

Reading probability shifts as a signal in themselves. A devigged probability moving from 40% to 55% over a short window tells you something concrete happened, and tracking the normalized number rather than the raw price avoids misreading vig fluctuations as sentiment shifts.

Fair value comparison across markets. When the same underlying event trades on multiple platforms with different question wording, devigging both allows a direct, apples-to-apples probability comparison. A meaningful gap between two devigged fair values on correlated markets can point to an arbitrage or hedging opportunity that the raw prices alone would obscure.

| Source | Accuracy | Speed of Update | Best Use |

|---|---|---|---|

| Polling average | Moderate | Days to weeks | Long-horizon baseline |

| Expert panel forecast | Varies | Days to months | Sanity check |

| Prediction market implied probability (devigged) | Good in aggregate | Minutes | Active trading reference |

How Accurate Is the Implied Probability from Polymarket?

Across large samples of resolved markets, devigged Polymarket probabilities have tracked realized outcome frequencies reasonably closely on liquid, well-traded markets. Markets that traded consistently near a devigged 70% have resolved YES in the neighborhood of 70% of the time across enough samples to call that a real pattern rather than coincidence.

Accuracy is not uniform. It concentrates on markets with real depth and participant attention, and weakens on thin markets where a small number of positions can move the price without reflecting genuine information. It also degrades in the early life of a market, before enough participants have weighed in, and improves as a market matures and accumulates volume.

The practical implication is that devigged implied probability deserves real trust on liquid, established markets and deserves more skepticism, and more independent verification, on markets that are new, thin, or narrowly covered.

Common Mistakes

Mistake 1: Reading the raw price as pure probability. Skip the devig step and you are treating platform margin as if it were part of the market’s genuine belief. That slightly overstates probability on both YES and NO at the same time, on every single market you look at, which is a small error that never corrects itself because it is baked into how the price is quoted in the first place.

Mistake 2: Ignoring the size of the vig when comparing markets. A tight 2 cent spread barely needs adjusting. An 8 cent spread does.

Mistake 3: Treating implied probability as static. A trader devigs a market on Monday, gets a fair value of 61%, writes it down, and comes back to size a position on Thursday still anchored to that number. In the meantime the raw YES price has moved from 0.58 to 0.71 on real news, which means the actual current devigged probability is closer to 74%, not 61%. Sizing Thursday’s position against Monday’s stale number means trading against a fair value that no longer exists, and the gap between the two is pure, avoidable error. The devigged number should be recalculated continuously as prices move, not calculated once and referenced days later on a market that has since shifted meaningfully.

Mistake 4: Comparing raw prices across platforms instead of devigged probabilities. Different platforms use different margin structures, so comparing raw YES prices directly across two venues can produce a misleading read on which one actually holds the better value.

Mistake 5: Assuming high liquidity guarantees accuracy everywhere. Check the specific market, not the platform’s reputation.

How DG3 Helps

Manually devigging every market before comparing it against your own probability estimate is tedious enough that most traders skip it, which means they are often comparing their research against a slightly distorted number without realizing it.

DG3’s Fair Value Engine runs the devig calculation automatically on every live Polymarket price, surfacing the normalized probability alongside the raw quote. That gives you a clean number to compare your own estimate against without doing the arithmetic manually on every position, and it updates continuously as the underlying market moves rather than requiring a fresh manual calculation each time.

Frequently Asked Questions

Q: What is market-implied probability? A: It is the probability of an event occurring as reflected by the current market price. The raw price includes platform margin, so a devig calculation is needed to recover the fair, normalized probability estimate.

Q: How do you read prediction market prices as probabilities? A: Take the YES and NO prices, sum them, and divide each individual price by that sum to normalize them to exactly 100%. The resulting devigged numbers are a more accurate probability read than the raw prices alone.

Q: What does devig mean in prediction markets? A: Devig means removing the platform’s built-in margin, or vig, from raw market prices to recover the true, normalized probability estimate that the market is implying.

Q: How do I calculate fair probability on Polymarket? A: Sum the YES and NO prices, then divide each price by that sum. If YES is 0.58 and NO is 0.46, they sum to 1.04, and dividing each by 1.04 gives fair probabilities of roughly 55.8% and 44.2%.

Q: What does a Polymarket price actually mean? A: The raw price represents the market’s aggregate probability belief plus a small built-in margin. Devigging separates the two, giving a cleaner read of what the market actually believes the probability to be.

Q: How accurate is implied probability from Polymarket? A: On liquid, well-traded markets, devigged implied probability has tracked resolved outcome frequencies closely across large samples. Accuracy weakens on thin, new, or narrowly covered markets.

Q: Why do YES and NO prices not add up to 100 cents? A: Because platforms build in a small margin, similar to a vig in sports betting, which means the sum of both sides typically exceeds 100 cents slightly. Devigging normalizes both prices to remove that margin.

Q: What is a no-vig probability calculator used for? A: It is used to strip platform margin out of raw prediction market prices, producing a normalized probability estimate that can be compared directly against your own research or against fair value on a different platform.

Final Thoughts

The raw price on a prediction market is close to the true probability, but close is not the same as accurate, and the gap between the two is the vig sitting quietly inside every quote.

Devigging takes ten seconds of arithmetic and produces a genuinely better number to trade against, which makes it one of the highest-value, lowest-effort habits a prediction market trader can build. Skipping it does not usually cost you dramatically on any single position. It costs you steadily, across every position, in ways that are easy to miss and expensive to ignore over time.

Read Fair Value Prediction Markets to see how a devigged probability becomes the foundation for every other calculation that follows it, from Kelly sizing to edge detection.