Slippage in Prediction Markets: What Your Fill Actually Cost You

You made money on the trade. YES resolved, $1 paid out, position closed. But somewhere between the price you saw when you clicked buy and the price you actually paid, 3.8 cents per share disappeared. On 300 shares that is $11.40. It showed up nowhere in your P&L. It does not appear on Polymarket’s fee page. You probably did not notice it.

Most prediction market traders have a running gap between what they think their execution costs and what their execution actually costs. Slippage is the main reason. It is real, it scales with position size in a non-linear way, and it belongs in your EV calculation before every trade – not in your confusion after every fill.

Quick Answer

Slippage in prediction markets is the difference between your intended entry price and your actual fill price. Three types: spread slippage (paying the ask instead of the mid-point, typically 1-3 cents per share), market impact slippage (your order consuming multiple ask levels, 2-8 cents or more on thin books), and timing slippage (price moving between decision and fill, 0.5-15 cents on fast-moving event markets). On a $5,000 position into a moderate-depth Polymarket book, total slippage can reach $300-600 depending on order book depth and execution type.

Key Takeaways

- Slippage is not Polymarket’s fee. The 2% fee on winning positions is disclosed, predictable, and constant. Slippage is variable, invisible, and scales with position size in a way that makes large positions on thin markets disproportionately expensive. Both belong in every EV calculation. Only one appears in the fee disclosure.

- On a Polymarket market with a 4-cent bid-ask spread, a single round-trip (entry plus eventual exit) costs 4 cents per share in spread slippage alone, before Polymarket’s fee, before gas. A position needing 6 cents of probability edge to break even on the model actually needs 10 cents to break even on the full cost.

- Market impact slippage is non-linear. On a shallow book, doubling position size more than doubles slippage because you are consuming progressively worse price levels as you move up the ask side. A 200-share entry costing 2 cents of slippage does not become a 400-share entry costing 4 cents. It becomes 6 or 7 cents.

- Timing slippage is the most expensive type on event markets and the hardest to control without infrastructure. On a market moving at 0.5 cents per second, a 30-second REST polling lag creates 15 cents of timing slippage before your order is even submitted. That gap eliminates most edges entirely.

- The calculation most traders skip: expected fill price from live order book depth before execution. DG3’s Execution Panel runs this automatically. Without it, you are discovering slippage in your fill confirmation rather than in your decision window.

- EV calculations that ignore slippage consistently overstate edge. A trader with a genuine 6-cent model edge entering with 3 cents of expected slippage has a 3-cent net edge trade, not a 6-cent one. Ignoring slippage does not make it disappear. It just makes the EV model wrong.

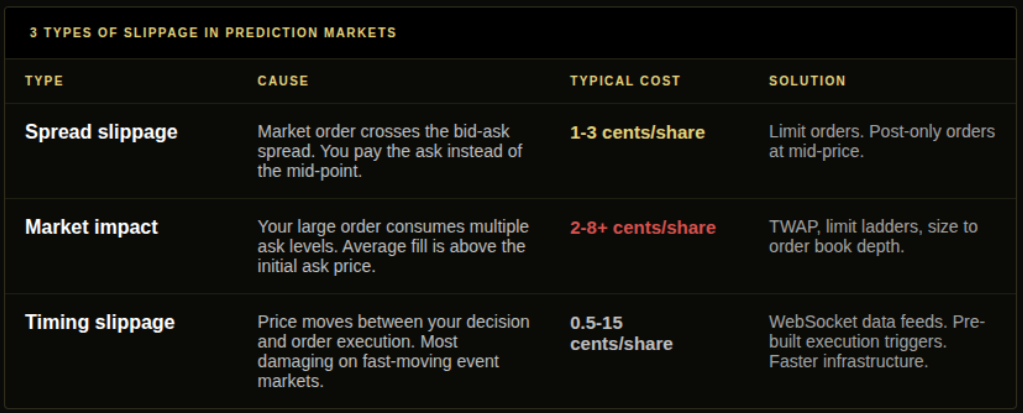

The 3 Types of Slippage

Type 1: Spread Slippage

The most predictable type. The bid-ask spread is the gap between the best buy price (bid) and the best sell price (ask). When you place a market order to buy YES, you fill at the ask, not the mid-point. On a market with YES bid 0.52 and YES ask 0.56, the mid-point is 0.54. You pay 0.56. Spread slippage on this trade: 2 cents per share.

On a 200-share entry: $4 of slippage before the position has existed for one second.

Spread slippage is solved by limit orders. A Limit GTC buy at 0.54 (the mid) sits in the book and waits for a seller to come to you. If it fills, spread slippage is zero. If the market is stable enough that this works, the 2-cent saving per share compounds across every position you take over a year. On 150 positions per year at an average 2-cent spread saving: 300 cents of pure recovered edge.

Type 2: Market Impact Slippage

The more expensive and less visible type. When your order is large relative to the order book’s depth, your own buying pushes the price against you as you fill. You consume the 0.56 ask, then the 0.58, then the 0.60, and your average fill is not 0.56 – it is 0.58 or worse.

The non-linear scaling is the part that catches traders. On a thin book:

- 100 shares at average 0.56: 2 cents above mid. Total slippage: $2.

- 300 shares at average 0.589: 4.9 cents above mid. Total slippage: $14.70.

- 600 shares at average 0.617: 7.7 cents above mid. Total slippage: $46.20.

Position size tripled, slippage increased 23x. The order book depth is the constraint. If you have not checked the book before sizing, you do not know which of these regimes you are entering.

Type 3: Timing Slippage

The most explosive type on event markets. The price at your decision moment and the price at fill execution are different because the market moved in between. On fast-moving prediction markets during news events, this gap can be 5-15 cents in under a minute.

Timing slippage is managed by infrastructure. WebSocket data rather than REST polling. Pre-built execution triggers rather than manual click sequences. The Execution Speed guide covers the infrastructure side in detail. The short version: a 30-second polling interval on a market moving at 0.5 cents per second costs 15 cents of timing slippage before your order is submitted. On a 6-cent edge trade, that inverts the position from positive to negative EV before a single share is filled.

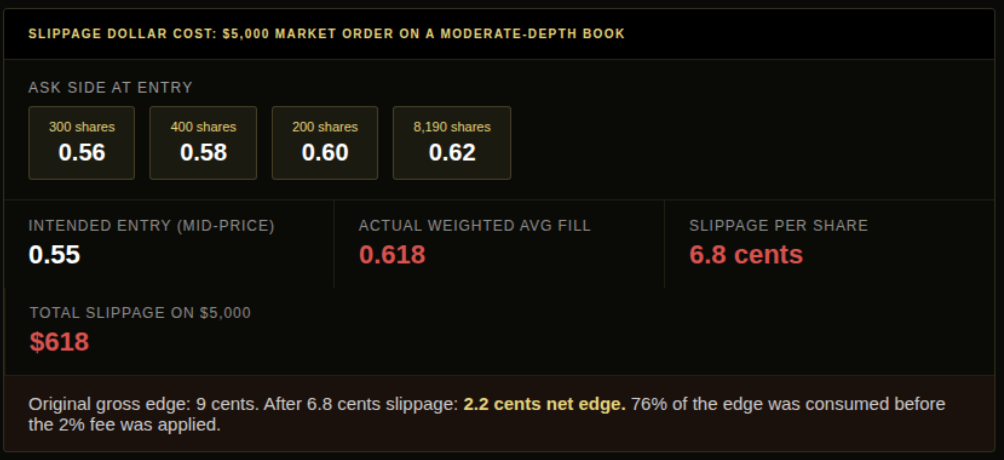

The Dollar Cost: A $5,000 Position Worked Example

$5,000 YES position on a moderate-liquidity Polymarket market. Mid-price: 0.55. Your model: fair value 0.64. Gross edge: 9 cents.

Order book ask side at entry:

- 300 shares at 0.56

- 400 shares at 0.58

- 200 shares at 0.60

- 8,190 shares at 0.62 (next level)

Market order for 9,090 shares (~$5,000 at mid 0.55) fills:

- 300 at 0.56

- 400 at 0.58

- 200 at 0.60

- 8,190 at 0.62

Weighted average fill: 0.618

Intended entry: 0.55. Actual fill: 0.618. Slippage: 6.8 cents per share.

On 9,090 shares: $618 of slippage. Gross edge was 9 cents. Net edge after slippage: 2.2 cents. After Polymarket’s 2% fee on a winning position (approximately 0.76 cents): net edge of 1.44 cents. A position sized and researched for a 9-cent edge delivers 1.44 cents of net edge because the order book was not checked before execution.

This is not an edge case. This is a $5,000 market order into a $60,000-volume Polymarket market. It is a common size on a common market. Most traders who do this do not check their fill prices afterward. They see the position open and assume the price shown was what they paid.

How to Calculate Expected Slippage Before Entry

Five steps before any position over $500:

Step 1: Note the current ask-side depth from the live order book. How many shares at what prices?

Step 2: Calculate how many shares your position requires at mid-price (your position size in USD divided by the mid-price).

Step 3: Simulate the fill by consuming ask levels from bottom to top until your share count is filled.

Step 4: Calculate the weighted average fill price.

Step 5: Compare weighted average fill to mid-price. The difference is your expected slippage. Subtract from gross edge. If net edge after slippage and fees is positive, proceed. If not, reduce position size or use limit orders.

DG3’s Execution Panel performs this calculation automatically from live order book data. You see expected fill price and total slippage cost before submission. The decision becomes: is net edge after slippage still worth taking?

5 Tactics to Reduce Slippage

Tactic 1: Limit GTC orders on stable markets. On markets with no immediate time pressure, a Limit GTC buy at or near the mid-price fills with zero spread slippage when a seller comes to you. The cost is potential non-fill and opportunity cost. For entries that can wait 30-60 minutes without losing edge, this is consistently the lowest-cost approach.

Tactic 2: Spread large positions across multiple limit orders. Breaking a $5,000 entry into $500 increments using multiple Limit GTC orders at descending prices lets the order book reload between fills. The market impact component of slippage – the part that scales non-linearly with size – drops sharply when no single order is large enough to clear multiple price levels.

Tactic 3: Size to the order book, not to your conviction. If the order book only has 120 shares within 2 cents of mid, the right position size is 120 shares (or a limit order waiting for book reload). Oversizing into a thin book is paying for conviction you did not account for in your EV calculation.

Tactic 4: Check spread width before comparing to edge. A market at 0.55 mid with a 4-cent spread has a 2-cent effective entry cost for crossing the spread. If gross edge is 4 cents, spread slippage alone leaves 2 cents of net edge before gas and the 2% fee. That might be a losing trade even on a correct probability estimate.

Tactic 5: Market orders only when speed genuinely justifies the cost. Reserve market orders for the specific situations where execution speed is worth more than entry price: breaking news, information timing trades, urgent exits. On everything else, the spread slippage is a voluntary tax on impatience.

Common Mistakes

The gap between assumed execution cost and actual execution cost is the most expensive thing most Polymarket traders are not measuring. Take your last 30 trades. Compare what you intended to pay (mid-price at the moment of decision) against what you actually paid (fill confirmation price). If you have never done this, the gap will almost certainly be larger than your estimate. For most traders who have not been actively managing slippage, the answer is 2-4 cents per trade larger than expected.

The second mistake is treating slippage as a constant rather than a variable that scales with position size. A trader who calculates slippage as “roughly 1 cent per trade” and then increases position size from $200 to $2,000 on a thin market has not increased slippage by 10x. They have likely increased it by 30-50x due to the non-linear market impact effect.

The third mistake is not accounting for slippage on exits. Most traders calculate entry slippage (because they notice the fill price on entry) but not exit slippage. A round-trip on a 4-cent spread market costs 4 cents in spread slippage total. Both legs matter. The full cost of a trade is entry slippage plus exit slippage plus gas plus the 2% fee, all of which should clear the gross edge before any position is taken.

Frequently Asked Questions

Q: What is slippage in prediction markets? A: Slippage is the difference between your intended entry price and your actual fill price. Three components: spread slippage (paying the ask instead of the mid-point), market impact slippage (your own order consuming multiple ask levels and pushing your average fill above the initial ask), and timing slippage (price moving between your decision and your order’s execution).

Q: How much does slippage cost on a $5,000 Polymarket position? A: On a liquid market with over $500,000 in volume and a 1-cent spread, roughly $25-75. On a moderate-liquidity market with a 4-cent spread and limited order book depth, $200-600 or more. The worked example in this article shows $618 of slippage on a $5,000 market order into a moderate-depth book, 76% of the 9-cent gross edge consumed before the 2% fee was applied.

Q: What are the three types of slippage in prediction markets? A: Spread slippage (paying the ask instead of the mid-point on a market order), market impact slippage (your large order consuming multiple ask levels, with non-linear scaling as position size increases), and timing slippage (price moving in the seconds between decision and fill execution). Each has a different solution: Limit GTC orders for spread slippage, spreading entry across multiple limit orders at descending prices for market impact, and faster data infrastructure for timing slippage.

Q: How do you minimise slippage on Polymarket? A: Five tactics: use Limit GTC orders at or near mid-price on stable non-time-sensitive entries, break large positions into smaller increments using multiple limit orders at descending prices, size to the available order book depth rather than to conviction, check spread width before comparing against gross edge, and reserve market orders for time-sensitive situations only.

Q: How does DG3 show expected fill price before you execute? A: DG3’s Execution Panel calculates the expected weighted average fill price for your chosen position size from live CLOB API order book data. You see projected fill price, slippage cost per share, and total dollar slippage before placing any order, allowing the net-edge check to happen before the trade, not after.

Q: Is slippage the same as Polymarket’s fee? A: No. Polymarket’s 2% fee on winning positions is disclosed, predictable, and consistent across all positions. Slippage is a variable execution cost caused by bid-ask spread and order book depth, is not disclosed by Polymarket, and scales non-linearly with position size. Both reduce net return. Both belong in every EV calculation before entry.

Final Thoughts

Every EV calculation has a slippage assumption embedded in it whether you put it there consciously or not. If you have not calculated expected slippage, the assumption is zero. Zero is almost certainly wrong.

The gap between a trader who accounts for slippage and one who does not is not visible on any single trade. Over 150 positions per year on moderate-liquidity markets, it can represent the difference between a profitable system and a break-even one. Not because the probability estimation was wrong. Because the execution cost was never counted.

Calculate it before you click. The order book is right there. The information is free. The cost of ignoring it is not.

For how fast slippage compounds as edge decays across your open positions, the Edge Decay guide covers the mechanics.

Also read – Edge Decay in Prediction Markets: Why Alpha Disappears

Kelly Criterion for Prediction Markets: Sizing Positions When Odds Move, Market Making on Polymarket: How to Earn the Spread