Market Making on Polymarket: How to Earn the Spread

You do not have to be right about the outcome to make money on Polymarket. You have to be right about the spread, quote both sides consistently, and survive the moments when someone on the other end of your quote knows something you do not. That last part is the whole job, and it is why most people who try market making quit before they understand what actually went wrong.

Quick Answer

Market making on Polymarket means placing both buy and sell orders around a market’s fair value to earn the bid-ask spread, rather than taking a directional position on the outcome. Profit comes from the difference between your buy and sell prices across many trades, not from correctly predicting the event. The main risk is adverse selection, where informed traders systematically hit your quotes right before the price moves against you, which is why active spread and inventory management separates profitable market makers from ones who slowly bleed capital to smarter counterparties.

What Is Market Making in Prediction Markets?

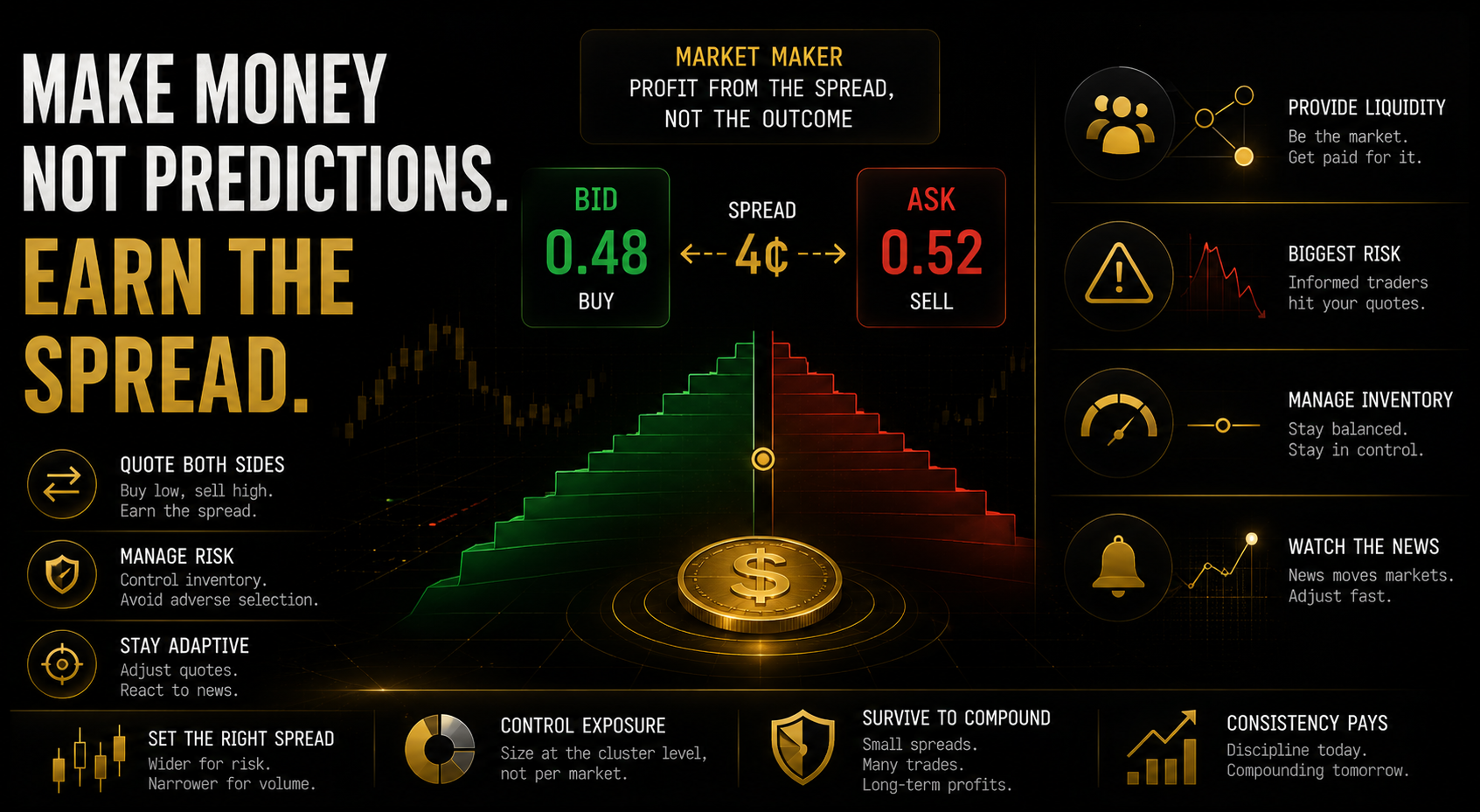

A market maker posts both a bid, the price they are willing to buy at, and an ask, the price they are willing to sell at, at the same time on the same contract. The gap between those two prices is the spread, and it represents the market maker’s potential profit on a completed round trip if both sides fill without the underlying fair value moving.

Say fair value on a market is roughly 50 cents. A market maker might post a bid at 48 cents and an ask at 52 cents. If both orders fill, roughly evenly, the market maker captures the 4 cent spread regardless of which way the market ultimately resolves. That is the entire appeal: profit that is structurally independent of predicting the outcome correctly, built instead from providing liquidity to traders who do want to take a directional position.

The risk sits in that word “if.” Both sides filling evenly, without fair value moving against the market maker in between, is the ideal case. Reality is messier, and the gap between the ideal and reality is where market making either works or quietly fails.

How to Make Money on Polymarket as a Market Maker

The mechanics come down to four ongoing tasks, done continuously rather than as a one-time setup.

Setting your spread width. Wider spreads earn more per completed round trip but fill less often, since fewer traders will accept a worse price. Narrower spreads fill more often but earn less per trade and leave less buffer against adverse price moves. The correct width depends on the specific market’s volatility and how informed the typical counterparty is likely to be.

Managing inventory. If your bid fills more than your ask, you accumulate a directional position you did not intend to hold, and that unintended exposure needs active management, either by adjusting your quotes to attract the opposite side or by hedging elsewhere.

Adjusting quotes as fair value shifts. A static spread around a stale fair value estimate is exactly what gets exploited by informed traders. Continuously updating your reference price as news arrives is not optional, it is the core defensive skill of the job.

Widening or pulling quotes during high-uncertainty windows. Right before a major news catalyst, like an injury report or a Fed announcement, the probability of facing an informed counterparty spikes. Experienced market makers widen spreads or step away from the market entirely during these windows rather than holding a normal spread into a moment of elevated risk.

Order Book vs AMM: Two Different Liquidity Provision Models

The prediction market landscape includes both order book venues like Polymarket and automated market maker pools like those used on Azuro. The risk profiles differ structurally, not just in degree.

| Feature | Order Book Market Making (Polymarket) | AMM Liquidity Provision |

|---|---|---|

| Price setting | Market maker sets their own bid/ask | Algorithm sets price based on pool ratio |

| Spread control | Full control – can widen or narrow | No control – algorithmically determined |

| Adverse selection management | Can pull quotes, widen spreads proactively | Cannot – all flow accepted at current price |

| Impermanent loss | Not applicable | Real risk – pool value diverges from held position |

| Capital efficiency | High (only collateralise posted orders) | Lower (must provide full pool-share liquidity) |

| Active management required | High – continuous monitoring | Lower – passive once deployed |

| Gas cost | Per-order adjustment | Per rebalancing event |

The key operational difference is control. Order book market making on Polymarket demands continuous, active management, but gives you the ability to pull quotes or widen spreads the instant you sense informed flow arriving. AMM liquidity provision is more passive once deployed, but removes that defensive ability entirely. On an AMM model, liquidity providers accept all incoming flow at the algorithmically determined price, meaning informed traders and uninformed traders hit the pool at the exact same terms, with no way for the provider to react in real time.

For anyone weighing the two, the honest framing is a trade-off between control and effort. Order book market making rewards active attention with better downside protection. AMM provision trades that protection for a simpler, less hands-on setup.

Worked Example: A Polymarket Market Making Position

Consider a moderately liquid political market with fair value around 45 cents. A market maker posts a bid at 43 cents and an ask at 47 cents, a 4 cent spread.

Over the course of a trading session, the bid fills three times at 43 cents and the ask fills three times at 47 cents, for six completed round trips. Gross spread capture: 6 x 4 cents = 24 cents per unit of size across those trades, before accounting for any adverse price movement during the session.

Now assume that on the seventh fill, a large, well-informed trader hits the bid at 43 cents right before a piece of news drops that moves fair value down to 38 cents. That single fill, if the market maker cannot adjust quickly enough, effectively costs 5 cents of unrealized loss on that specific position, potentially wiping out more than one full spread’s worth of the earlier profitable round trips.

This is the entire adverse selection problem in miniature: consistent small gains from uninformed flow, punctuated by occasional larger losses when an informed trader trades right before a price-moving event. Long-run profitability depends on the small gains outweighing the occasional larger losses, which is a function of spread width, quote responsiveness, and how quickly you can identify and react to a genuinely informed counterparty.

3 Risks Every Prediction Market Maker Must Manage

Adverse selection. This is the single largest structural risk in the business and the entire reason spreads exist at all. Informed traders don’t hit quotes randomly. They hit them disproportionately right before the price moves, which means a market maker quoting a static spread through a news window is effectively handing out free information to whoever reacts fastest. A political market maker quoting 43/47 cents around a fair value of 45 gets picked off on the bid at 43 seconds before a leaked poll drops fair value to 38, and that single fill can erase the profit from a dozen earlier, uninformed round trips.

Inventory risk. Uneven fills leave you holding a position you didn’t choose to hold.

Volatility risk around news events. Fair value can jump discontinuously around a catalyst, and a market maker with stale quotes at that moment is effectively offering a free option to whoever trades against them first.

Is Market Making Profitable on Polymarket?

It can be, but the honest answer depends heavily on execution quality and market selection rather than the strategy being reliably profitable by default. Moderately liquid markets with steady, mixed order flow tend to favor market makers, since a healthy mix of informed and uninformed participants means the uninformed flow’s spread capture can outweigh the periodic cost of adverse selection.

Thin markets with infrequent but highly informed flow tend to be worse for market makers, since a smaller number of fills means each adverse selection event represents a larger share of total activity, and there is less uninformed flow to offset the cost. Highly liquid, heavily-covered markets can also compress spreads to the point where the earnable margin barely covers the operational effort and risk involved.

The traders who do well at this generally specialize, learning the specific volatility and informed-flow patterns of a narrow set of market types rather than attempting to market make broadly across everything available on the platform.

Common Mistakes

Running the same spread width regardless of market conditions. A spread that survives a quiet, low-volatility period is often far too narrow for the run-up to a major news catalyst on that same market. The fix: widen mechanically ahead of known catalysts, not reactively after the price has already moved.

Ignoring inventory buildup. One side of the quote fills more than the other, and a market-neutral strategy quietly turns into an unintended directional bet. The fix: check your net position every session, not just your open orders.

Failing to widen or pull quotes before known catalysts. Fed announcements and election results are risk windows you can see coming. Quote through them at your normal spread and that’s a choice, not bad luck.

Market making on markets with a poor informed-to-uninformed flow ratio. Not every market is a good candidate. Selecting markets with genuinely mixed participation matters as much as any individual quoting decision.

Underestimating the operational effort required. Order book market making gets marketed in places as close to passive income, quote once and collect the spread while you sleep. It isn’t. A market maker who sets a 4 cent spread on Monday and doesn’t touch it again until Friday will have been adversely selected multiple times over by then, most likely without noticing, because the losses show up as a slowly eroding account balance rather than a single obvious event. The traders who actually make this work check their positions constantly, especially in the hours around scheduled news, and treat every session as requiring fresh attention rather than a spread they can set once and walk away from.

How DG3 Helps

Reacting quickly enough to protect against adverse selection requires seeing relevant information as fast as possible and having a clear, continuously updated fair value reference to quote around. DG3’s Fair Value Engine provides that continuously devigged reference price, updating as the underlying market moves, which gives market makers a cleaner anchor than the raw, potentially stale last-traded price.

The Intelligence Pane’s live signal feed, scoped to the specific market being quoted, also surfaces exactly the kind of incoming news and informed flow activity that should trigger a spread widening or a temporary quote pull, reducing the lag between a real information event and a defensive quote adjustment.

Frequently Asked Questions

Q: How do you make money on Polymarket without predicting outcomes? A: Through market making, posting both buy and sell orders around fair value to earn the spread between them, which generates profit from providing liquidity rather than from correctly predicting which side of the market will win.

Q: What is adverse selection in prediction market making? A: It is the risk that informed traders disproportionately trade against a market maker’s quotes right before the price moves in a direction unfavorable to the market maker, since informed traders are more likely to act just ahead of price-moving information.

Q: Is market making profitable on Polymarket? A: It can be, particularly on moderately liquid markets with a healthy mix of informed and uninformed order flow, but profitability depends heavily on spread management, market selection, and responsiveness around news events rather than being guaranteed by the strategy itself.

Q: What is the difference between order book market making and AMM liquidity provision? A: Order book market making, as used on Polymarket, lets the market maker actively set and adjust their own bid and ask prices. AMM liquidity provision uses an algorithm to set prices based on pool ratios, removing the provider’s ability to react to informed flow in real time.

Q: How wide should my market making spread be? A: It depends on the specific market’s volatility and the likely proportion of informed versus uninformed order flow. Wider spreads protect against adverse selection but fill less often, while narrower spreads fill more but leave less buffer against unfavorable price moves.

Q: What is inventory risk in market making? A: It is the risk of accumulating an unintended directional position because one side of your quote fills more often than the other, which then exposes the market maker to the same outcome risk as any directional trader.

Q: Can I earn passive income on prediction markets through market making? A: Market making can generate income without taking a directional view on outcomes, but it requires continuous, active management rather than being genuinely passive, particularly around news events where adverse selection risk spikes sharply.

Q: How does order flow toxicity affect prediction market makers? A: Toxic order flow, meaning trades that reflect information the market maker does not have, disproportionately hits quotes right before adverse price moves, which is why market makers widen spreads or pull quotes when they suspect informed traders are active.

Final Thoughts

Market making is not a way to avoid taking a view on prediction markets. It is a different kind of view, a bet that you can price the spread correctly and manage the moments of informed flow better than the spread compensates you for on average.

The traders who do this well are not the ones who found a perfectly safe strategy. They are the ones who treat adverse selection as the central, permanent cost of the business rather than an occasional surprise, and who widen, narrow, or pull their quotes based on a continuously updated read of fair value rather than a static spread set once and left alone.

Pair market making with a solid grasp of Fair Value Prediction Markets to keep your quoted reference price honest as conditions shift underneath it.