Positive EV Trading: A Practical Framework for Prediction Markets

You bought YES at 0.54. Your research was thorough. Your estimate was careful. The market resolved NO.

That night you opened a notes app and wrote “stop using this system.” You deleted the app. You went back to gut instinct. Your system was not broken. A 46% probability event had just occurred, exactly as the math said it might. You quit a process that was working because you confused a losing result with a wrong decision.

That confusion costs more money in prediction market trading than any bad pick ever will.

Quick Answer

Positive EV trading in prediction markets means taking positions where your estimated probability is higher than the devigged market implied probability, creating a mathematical edge. The 5-step framework: estimate independently, devig the price, calculate edge, apply minimum thresholds against Polymarket’s 2% fee, size with Kelly. Outcomes on individual positions are irrelevant to whether the decision was correct. Edge only becomes visible at scale across 100 or more comparable positions.

Key Takeaways

- Positive expected value and positive results are fundamentally different measurements. A position with genuine 13-cent edge will lose money roughly 35-40% of the time by design. If you evaluate decisions by outcomes, you will abandon correct processes and keep incorrect ones based on nothing but variance.

- The EV calculation requires two honest inputs: your independent probability estimate and the devigged market price. The market price is visible to everyone. Your probability estimate is the only part of the calculation that can produce genuine edge, which is why forming it before looking at the price is not a suggestion but a structural requirement.

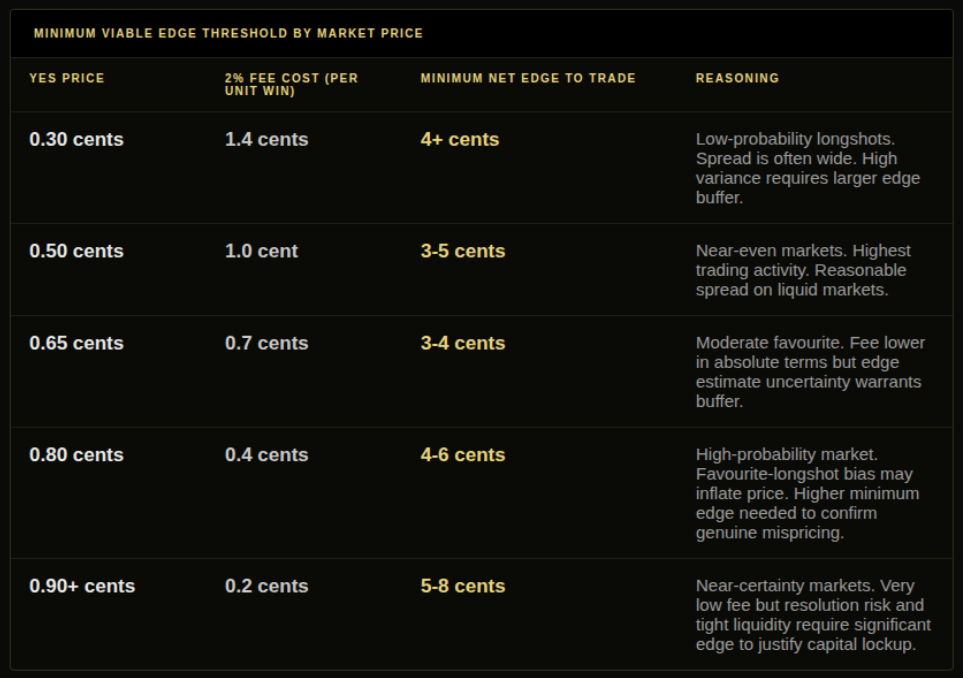

- On Polymarket, the 2% fee on winning positions is a cost that changes the minimum viable edge by market price. A 1-cent edge at a 0.50 market is a negative EV position after fees. The minimum edge threshold table below shows what the floor actually looks like.

- The 5-step framework runs in a fixed sequence for a reason: estimate, devig, calculate edge, threshold check, size with Kelly. Reversing the order starting with a price that looks interesting and working backwards produces positions anchored to market consensus rather than independent analysis.

- Expected value compounds through volume, not individual wins. A consistent 4-cent edge across 200 positions per year is not 4 cents of income per position. It is a distribution that, given enough sample size, trends toward its mathematical expectation. That is not a comforting metaphor. It is arithmetic.

- DG3’s Edge Finder applies the devigging and ranking steps of this framework to every live Polymarket market simultaneously, in real time. What takes you 5 minutes per market takes the Edge Finder 0 seconds across all of them.

What EV Actually Is (And What It Is Not)

Expected Value (EV): The average result of a position if it were replayed under identical conditions an infinite number of times. A positive EV position has a mathematically favourable expected average. A negative EV position does not. Neither tells you what happens on the next trade.

Most traders have read this definition before. Almost none have actually internalized what it means for their process.

Here is what it means: the quality of a decision is determined before the outcome is known. When you buy YES at 0.54 and you genuinely estimate 70% probability, you made a correct decision. The event resolving NO at 46% frequency is not a surprise. It is not a failure. It is probability mechanics working exactly as described.

The formula for a binary Polymarket position:

EV = (p x profit_per_unit) – ((1 – p) x cost_per_unit)

Where p is your estimated probability, profit_per_unit is what you gain per dollar if YES resolves (1 minus entry price), and cost_per_unit is what you lose per dollar if NO resolves (entry price).

Worked example using a real Polymarket market type:

A Federal Reserve rate decision market has YES (hold rates) priced at 0.61. After reading the most recent FOMC minutes and comparing against forward guidance language, you estimate the true probability of a hold at 0.73.

- EV per dollar = (0.73 x 0.39) – (0.27 x 0.61)

- EV = 0.2847 – 0.1647

- EV = +0.12 per dollar, or +12 cents per dollar staked

That is a 12-cent edge. At half Kelly on a $2,000 bankroll, the correct position is approximately $180. If the Fed cuts and the position loses, the loss is not evidence the analysis was wrong. It is evidence a 27% probability event occurred. The only thing that would change the quality of the original decision retroactively is if the probability estimate was wrong, not if the outcome was wrong.

Over 50 positions with similar edge, the arithmetic takes over. Over 5, it almost certainly does not.

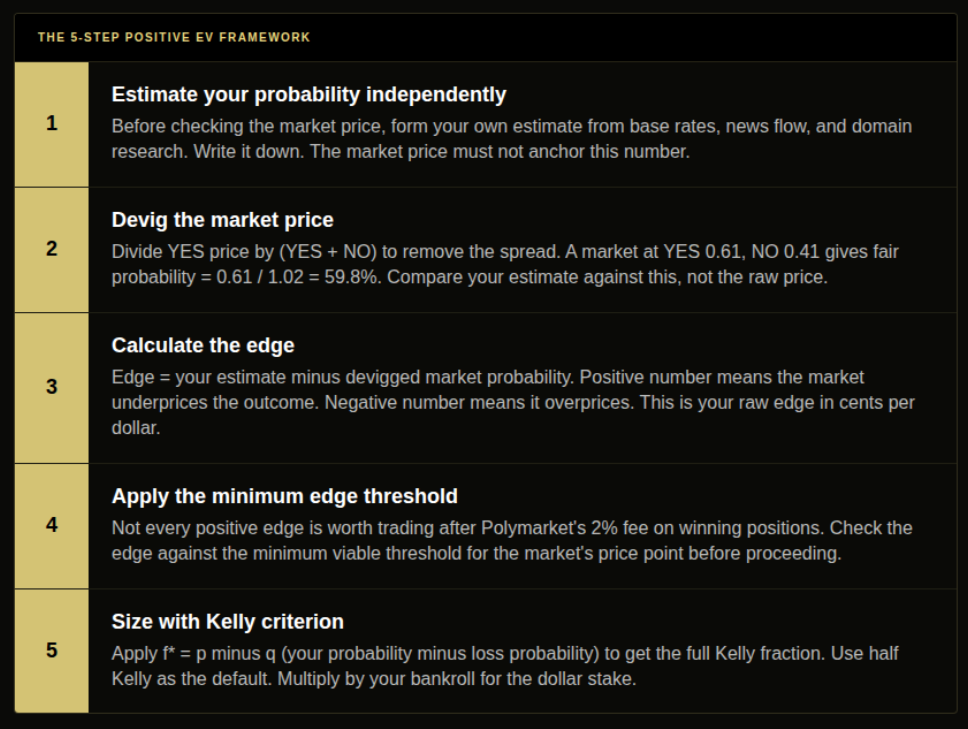

The 5-Step Positive EV Framework

Step 1: Estimate your probability before touching the price. This is not optional. Every other step depends on this one being honest. Use base rates, news flow, domain knowledge, or a formal model. Write the number down. If you look at the market price first and then form an estimate, you have anchored to the crowd’s consensus and eliminated your ability to find genuine edge. There is no shortcut here. The estimate is the work.

Step 2: Devig the market price. The raw Polymarket YES price includes the bid-ask spread. A market at YES 0.61, NO 0.41 has a total overround of 1.02. Devigged fair probability = 0.61 / 1.02 = 59.8%. That 1.2-cent gap between raw price and fair probability sounds small. Across 200 positions per year, you are adding 240 cents of systematic error to your edge calculations if you skip it. For a full explanation of the devig mechanic, read the Implied Probability Calculator article.

Step 3: Calculate edge. Edge = your estimated probability minus devigged market probability. In the Fed example: 0.73 – 0.598 = 13.2 cents of edge. Positive means the market underprices the outcome. Negative means it overprices it. The size of this number determines whether step 4 clears the threshold.

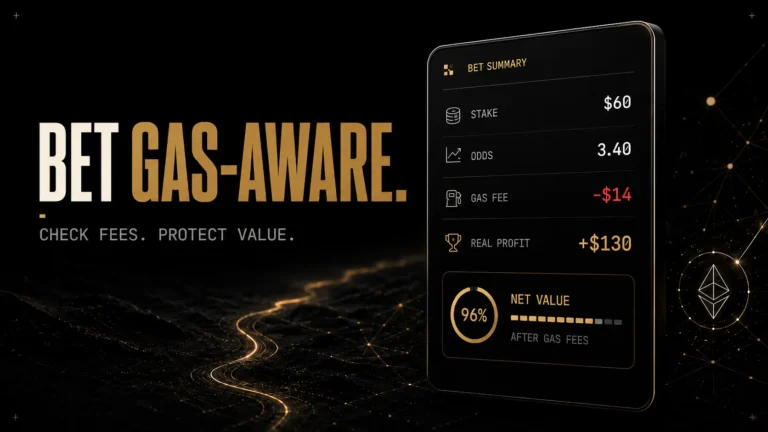

Step 4: Apply the minimum edge threshold. Not every positive edge is worth taking after Polymarket’s 2% fee on winning positions. The fee is paid on the profit, not on the stake. At 0.61 YES, the fee on a winning $180 position costs approximately $1.44. That represents about 0.8 cents per unit. A position with 1-cent apparent edge is effectively break-even or negative after fees and spread. The minimum viable net edge varies by price.

Step 5: Size with the Kelly criterion. For a binary Polymarket market: f* = p – q, where p is your estimated win probability and q = 1 – p. Use half Kelly as the default. At 73% estimated probability: f* = 0.73 – 0.27 = 0.46. Half Kelly = 0.23 of bankroll. On a $2,000 bankroll that is $460 at full Kelly, $230 at half Kelly. Read the Kelly Criterion article for the complete sizing framework before applying this.

Why the System Produces Losing Trades (By Design)

This is the section you need to read on the night you want to quit.

A genuine 70% probability position loses 30% of the time. Run 20 positions at 70% edge and expect 6 losses. Run them in sequence and you will see 3 or 4 losses in a row at some point. You will feel certain the model is broken. You will be wrong. What is happening is probability mechanics operating exactly as described on a sample too small to surface the underlying edge.

The law of large numbers needs a large number. That means roughly 100 positions in a comparable category before the signal starts to distinguish itself from noise. Most retail Polymarket traders abandon systematic approaches after 15-20 positions. They never give the sample size a chance to work. They conclude the framework does not work, having never actually run the experiment.

The fix is tracking that separates process quality from outcome quality. Record your estimated probability before every position, not just the result. After 100 positions, compare your estimated probability bands against your actual win rates. If you estimated 70% on 30 positions and won 62%, you have an overconfidence bias of approximately 8 percentage points. Your EV calculations are overstated by a predictable amount. That is information you can correct. “I had a bad run” tells you nothing you can act on.

EV trading without calibration tracking is just guessing with a formula attached. The formula is the easy part.

What Counts as Real Edge (And What Does Not)

Four things that look like edge but are not:

The liquidity discount. Thin Polymarket markets have wide spreads. YES 0.58, NO 0.48 means a 6-cent spread baked in. After devigging, fair YES probability is approximately 54.7%. If you estimated 58%, your apparent 3.3-cent edge is actually negative 3.3 cents once you account for the spread structure. Always devig before calculating edge.

The information you think you have. You read the Fed statement and estimated 73% probability of a hold. So did 200 other informed traders. The market at 0.61 has either not processed it yet (an information timing edge real but time-limited) or it has processed it and disagrees with you (a probability estimation edge you may be right, but verify). Distinguish between the two before sizing.

The stale market. A market last traded 6 hours ago on an event that has since had significant news. The price has not moved not because the crowd decided it is right, but because nobody has updated it yet. This is a real edge. It is also an edge that is measured in minutes, not hours. DG3’s Signal Layer flags stale markets next to news events. Without it, you are manually checking timestamps across dozens of markets.

The calibration illusion. Your edge is real only if your probability estimates are genuinely better calibrated than the market over time. A single position where you estimated 73% and won is one data point. A track record of 73% estimates resolving YES 72% of the time across 200 positions is calibration. The Calibration guide shows how to build and read that track record.

Common Mistakes

Mistake 1: Quitting after a losing streak on genuinely positive EV. A 30% probability sequence happening 5 times in a row feels like the system is broken. It is not. It is 0.30^5 = 0.24% probability unlikely, but not rare enough over a year of trading to mean anything. The traders who stay systematic through losing streaks are not more disciplined by personality. They are more disciplined because they track the process separately from the outcomes. When you have 50 data points showing your calibration is accurate, a bad week is not evidence. It is noise.

Mistake 2: Anchoring probability estimates to market price. You see a market at 0.55 and think “that seems a bit low, probably more like 0.62.” Your estimate is not 0.62. Your estimate is “market price plus gut displacement,” which means it is still the market’s estimate with adjustment noise. Start from base rates and contextual analysis. The market price should be the last number you see before comparing, not the first number that shapes your view.

Mistake 3: Treating all positive-edge positions as equivalent. A 3-cent edge and a 13-cent edge both qualify as positive EV. They do not deserve the same stake. Kelly sizing scales with edge magnitude precisely for this reason: a larger confirmed edge justifies a larger fraction of bankroll. Flat-staking across all positive-EV positions leaves the bulk of the mathematical advantage unused. Every position you size the same regardless of edge magnitude is a position you are not actually applying the framework to.

Mistake 4: Skipping the devig step because it “barely changes the number.” At a 0.50 market with a 2% overround, the devig adjustment is approximately 1 cent. Not much per trade. Over 200 positions per year, that is a 200-cent systematic error in your edge calculations. After five years, it is 1,000 cents. “Barely changes the number” compounds into a meaningful distortion of your entire calibration record.

Mistake 5: Using the 2% fee as a rough guideline rather than a precise cost. The Polymarket fee is not a flat 2% of stake. It is 2% of the profit on winning positions. That means the fee cost in absolute cents varies by market price. At a 0.40 market, winning earns 0.60 per unit, so the fee is 0.012 cents per unit. At a 0.80 market, winning earns 0.20, so the fee is 0.004 cents per unit. The minimum edge threshold is not constant across market prices. Using a single rough number distorts your threshold calculation at price extremes.

How DG3 Helps

The most time-consuming step in the 5-step framework is the devigging and ranking step. Done manually across 40 active Polymarket markets, it takes 20-30 minutes before you have identified where the largest current edges sit. By then, some of those edges have closed.

DG3’s Fair Value Engine deviggs every live Polymarket market automatically, removing the bid-ask spread to show the true implied probability in real time. You arrive at Step 3 of the framework instead of Step 2.

DG3’s Edge Finder then ranks all live markets by the gap between current price and fair value, updated continuously. The markets with the largest current divergences sit at the top. That ranked list compresses Steps 1 through 3 of the framework across every Polymarket market simultaneously.

Step 1 is still yours. The probability estimate cannot be automated. It is the work that creates the edge. What DG3 removes is everything between having that estimate and knowing which markets are worth bringing it to.

Start with the terminal at dg3.trade.

Frequently Asked Questions

Q: What is positive EV trading in prediction markets? A: Positive EV trading means systematically taking positions where your estimated probability of an outcome is higher than the probability the current market price implies, after removing the bid-ask spread. The gap between those two numbers is your edge. A position is positive EV if that gap is real, not the result of anchoring to the market price or wishful estimation.

Q: How do you find positive EV positions on Polymarket step by step? A: Estimate fair probability independently before checking the price. Devig the Polymarket price by dividing YES by (YES + NO). Calculate edge as your estimate minus devigged probability. Check edge exceeds the minimum viable threshold for that market price after Polymarket’s 2% fee on winning positions. Size using the Kelly criterion at half Kelly as default. DG3’s Edge Finder automates the devigging and ranking steps.

Q: How big does an edge need to be to be worth trading on Polymarket? A: It depends on market price. At a 0.50 market, the minimum viable net edge after Polymarket’s fee is approximately 3-5 cents. At a 0.80 market the fee is smaller in absolute cents but the risk of favourite-longshot bias inflating the price means you need 4-6 cents of confirmed edge before it is worth taking. Small apparent edges at any price point risk being fee-negative or within the margin of your estimation error.

Q: What is the difference between EV and profit in prediction markets? A: EV is the expected average result across many repetitions of the same decision. Profit is what actually happened. In the short run they can diverge significantly because variance dominates small samples. A trader can run genuinely positive EV for three months and show negative profits. The reverse is also true. Profit measures what happened. EV measures whether you are playing the right game.

Q: How does DG3 identify positive EV positions automatically? A: DG3’s Fair Value Engine calculates the devigged fair probability for every live Polymarket market by dividing the YES price by the YES plus NO sum. DG3’s Edge Finder then ranks markets by how far the current trading price diverges from that fair value baseline, updated continuously. The ranked output shows where current mispricings are largest across the entire Polymarket catalogue.

Q: How do you find positive EV on Polymarket as a beginner? A: Start with one market category you understand deeply a sport, an economic indicator type, a political domain. Form probability estimates from primary sources before checking market prices. Track every estimate and every outcome in a spreadsheet. After 50 positions, compare your estimated probability bands against your actual win rates. That comparison tells you whether your estimates are calibrated and whether your edge is real.

Q: What is a positive EV prediction market strategy? A: A systematic approach where every position is evaluated using the same 5-step framework: independent probability estimation, devigging, edge calculation, threshold check, and Kelly sizing. Results are tracked at the calibration level, not just win/loss. The strategy improves over time through feedback between estimated probabilities and actual outcomes, not through changing what markets you pick based on recent results.

Q: Why does positive EV trading sometimes produce losing months? A: Because variance dominates small samples. A genuine 65% probability position loses 35% of the time. Over 20 positions, a losing run of 7 or 8 consecutive losses is statistically possible and tells you nothing about whether the underlying edge estimate is accurate. The law of large numbers requires hundreds of comparable positions before the expected value of the process surfaces clearly in the results.

Q: What edge size is worth trading for prediction market traders? A: After Polymarket’s 2% fee on winning positions, the minimum viable net edge varies from approximately 3-4 cents at near-even markets to 5-8 cents at high-probability markets where liquidity is tighter and favourite-longshot bias is stronger. The minimum is not constant. Calculate fee cost precisely for the specific market price before deciding whether a position clears the threshold.

Final Thoughts

The 5-step framework is not complicated. You could apply it to your next ten positions this week. The difficulty is not the framework. The difficulty is holding the framework against your own psychology across months of results that will not cooperate with your timeline.

Most Polymarket traders never reach the sample size where the math becomes readable. They take 20 positions, draw conclusions, and adjust the strategy. They take another 20 positions, draw more conclusions, adjust again. The adjustments are not improvements. They are the trail of a process being optimized against noise.

The framework only tells you what to do. Staying with it long enough for the sample to matter is the part nobody can hand you.

The calculation is the easy part. Build the habit of running it before every position, every time, in order. That is the entire system.

Sign up now – DG3 Terminal