.png?updatedAt=1779992389202)

Prediction Market Microstructure: How Prices Actually Form

Most people see a number on a prediction market and assume it just appears. It does not. Behind that single price sits a whole machine of orders, spreads, market makers, and information colliding in real time. Microstructure is the study of that machine. Learn it, and the price stops being a number you read. It becomes a story you can hear.

What is prediction market microstructure?

Prediction market microstructure is the study of how a price forms at the level of individual orders, including who trades, how their orders interact, and how information turns into a market price.

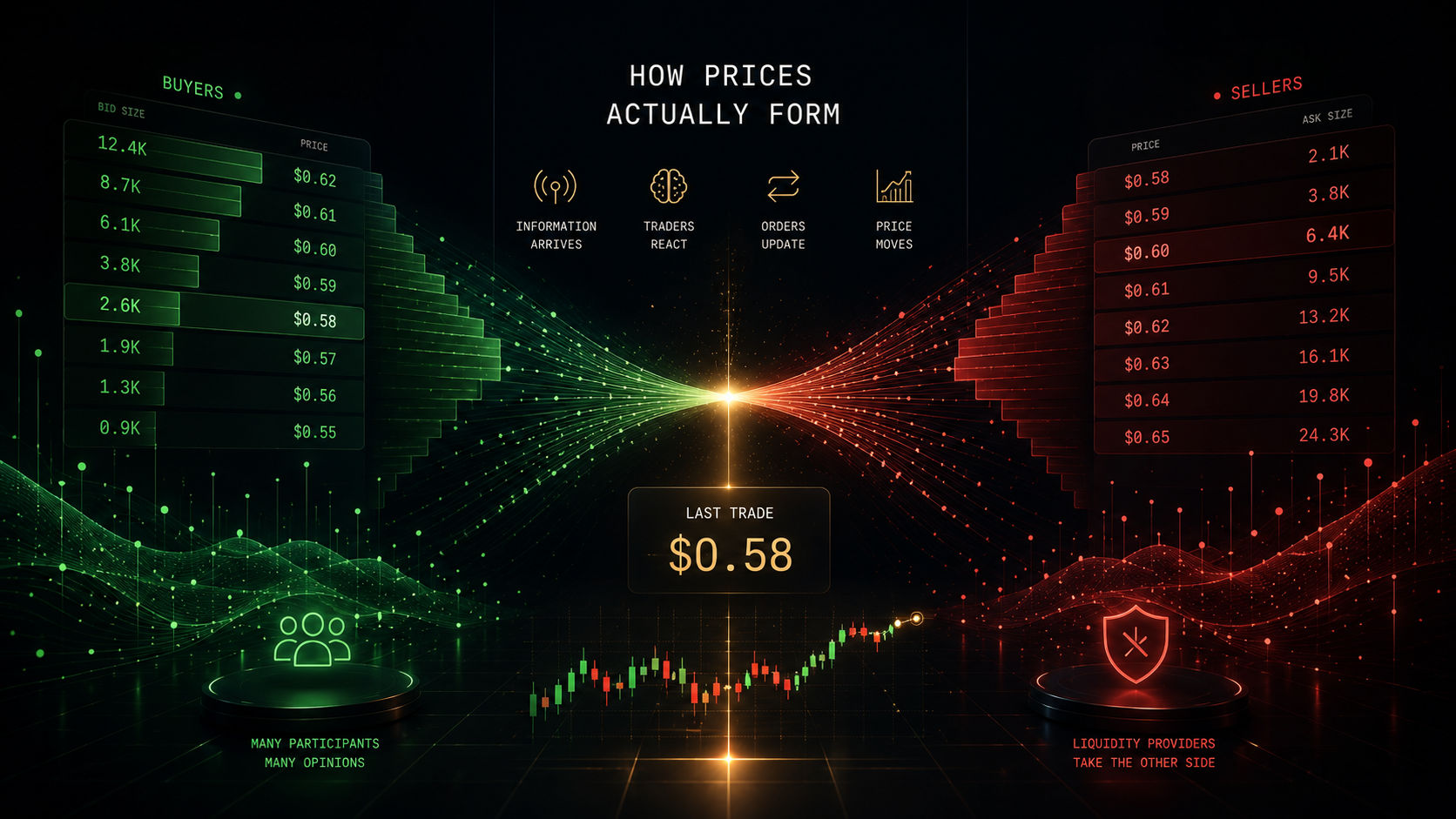

How is a price actually formed?

A price is the meeting point of everyone willing to buy and everyone willing to sell, right now. Buyers post what they will pay. Sellers post what they will accept. The price is wherever those two stacks touch. When new information arrives, traders move their orders, the stacks shift, and the price moves with them.

That is the whole engine in three sentences. Everything below is just the detail of how it runs.

The order book: where most of the action lives

Picture two columns. On one side, every buy order, ranked from highest price down. These are bids. On the other side, every sell order, ranked from lowest price up. These are asks. Together they form the order book.

The highest bid and the lowest ask sit in the middle, staring at each other. The gap between them is the bid-ask spread. When someone agrees to cross that gap, a trade happens, and the last traded price updates.

This setup has a name. A central limit order book, or CLOB. It is the same structure that runs equity markets, futures, and most serious financial venues. Polymarket runs an order book model. So the skills you build reading one transfer straight across.

Two ways to trade inside it:

Limit order. You name your price and wait. Buy this contract at 61 cents, not a tick higher. You might get filled. You might not. You are providing liquidity, sitting in the book until someone takes the other side.

Market order. You take the best price available right now and trade immediately. You are removing liquidity, reaching into the book and lifting an order that was already there.

That distinction matters more than almost anything else in trading. Limit orders build the book. Market orders eat it.

The bid-ask spread: the price of trading now

The spread is not random. It is the market's way of pricing immediacy.

A tight spread, say 49 to 50 cents, means there is plenty of interest on both sides and you can get in and out cheaply. A wide spread, say 40 to 55 cents, means the book is thin and trading right now will cost you. You buy high, you sell low, and the gap is friction you eat on entry and exit.

The spread is the cost of demanding a trade immediately instead of waiting for one. Wide spreads are a warning. They tell you liquidity is thin and your read had better be good enough to clear that cost.

Who is actually trading

A price is a crowd, and the crowd has types.

Market makers. They quote both sides at once. A bid and an ask, always live, profiting off the spread. Their job is to keep the book full so others can trade. They take on inventory risk to do it, and the spread is their compensation. Without them, books go thin and prices get jumpy.

Informed traders. The sharps. They trade because they know something, or model something, the price has not caught yet. When they move, they move with size and conviction, and they drag the price toward what they believe is true.

Uninformed traders. The public. They trade on vibes, headlines, loyalty, or a hunch. Their flow is noisy and often lands on the wrong side. Market makers love them, because their orders are the bread and butter of spread capture.

Arbitrageurs. They hunt the same outcome priced differently in two places and pocket the difference. Their trading drags prices back into line and keeps the whole system honest.

Every trade is one of these meeting another. Reading microstructure is partly reading which type is driving the flow right now.

AMM vs order book: two ways to make a market

Not every venue uses an order book. Some use an automated market maker, an AMM. The difference shapes how the price feels.

An order book matches real buyers to real sellers. The price moves when orders interact. An AMM replaces the human counterparty with a pool of capital and a formula. You trade against the pool, and the formula sets your price based on how much you buy. Big order, the price slides as you fill. That slide is called slippage.

Order books give you tighter spreads and a transparent view of resting demand on liquid markets. AMMs give you a price on anything, anytime, even with no one else around, which is why they took off in early crypto markets. The tradeoff is slippage and a price that bends under size.

Here is how the two compare.

How information becomes price

This is the part that matters most.

A price is a forecast. When something new happens in the world, the forecast has to update, and microstructure is the mechanism that updates it.

Walk through it. A piece of news drops. An informed trader sees it first and acts, sending a market order that lifts the best ask. The last price ticks up. Market makers notice their quotes getting hit on one side and widen or shift to protect themselves. Other traders see the move, infer that someone knows something, and follow. Within seconds, the new information is baked into the price.

No vote. No announcement. Just order flow doing its job. The speed and smoothness of that update is a direct read on how healthy the market is. Deep, liquid markets absorb news cleanly. Thin ones lurch.

This is why reading order flow beats reading the headline price alone. The price tells you where the market is. The flow tells you where it is going.

A worked example

A contract on a sporting outcome sits quietly. Best bid 53, best ask 54, a one cent spread. Tight. Healthy.

Then a key player is ruled out an hour before kickoff. Here is the sequence.

An informed trader who tracks team news acts first. They fire a market order to sell, hitting the 53 bid and clearing it. Last price drops to 53, then 52 as their order keeps filling down the book. Market makers see one-sided pressure and pull their bids lower, repricing to 49 bid, 51 ask. The spread widens to two cents while uncertainty is high. Public traders, now seeing the news, pile in to sell at 49. The price settles at 48 as a new consensus forms.

In under a minute, a single fact moved the price six cents and reshaped the entire book. That is microstructure. Not theory. The actual sequence of orders that turns information into a number.

For scale on why this matters, Polymarket cleared more than 14 billion dollars in trading volume in 2024, the bulk of it driven by the US election. That is the order flow, market by market, that all this machinery is built to handle.

FAQ

What is the difference between a limit order and a market order? A limit order sets your price and waits in the book to be filled, providing liquidity. A market order takes the best available price right now and fills immediately, removing liquidity. Limit orders build the book. Market orders consume it.

What does the bid-ask spread tell me? It tells you the cost of trading immediately and how liquid the market is. A tight spread means deep liquidity and cheap entry. A wide spread means thin liquidity and expensive trading, and it is a signal to be careful.

What is the difference between an AMM and an order book? An order book matches real buyers and sellers, with the price set where they meet. An AMM lets you trade against a pool of capital, with the price set by a formula. Order books are tighter on liquid markets. AMMs always give you a price, but with slippage on size.

Who are market makers and why do they matter? Market makers quote both a buy and a sell price at once and profit off the spread. They keep the book full so others can trade. Without them, liquidity dries up and prices get volatile.

How does news actually move a prediction market price? An informed trader acts on the news first, sending orders that move the last price. Market makers reprice to protect themselves. Other traders follow. The new information ends up baked into the price in seconds, through order flow alone.

Key takeaways

- Microstructure is how a price forms at the level of individual orders. It is the machine behind the number.

- An order book stacks bids against asks. The gap between the best of each is the spread, and the spread is the price of trading now.

- Most serious venues, Polymarket included, run a central limit order book. AMMs trade against a pool instead, easier on thin markets but with slippage.

- Four player types drive every market: market makers, informed traders, the public, and arbitrageurs. Reading flow means reading who is in control.

- Information becomes price through order flow. The price tells you where the market is. The flow tells you where it is headed.

Related reading

For how a sharp price reads against a bookmaker line, see price discovery in prediction markets vs sportsbooks. To pin down the number all this machinery is chasing, read fair value in prediction markets. Then study why the closing line is the truest price a market prints, and how sharp money moves differently from the public. To put all of this on one screen, the DG3 terminal shows the order book, the flow, and the sharps in a single view.

Author note

Written by the DG3 research desk. We build tools for traders who treat probability as a number to beat, not a line to accept. We track market microstructure, order flow, and cross-venue pricing across prediction markets every day.

The order book, the flow, and the sharps in a single view. Try the DG3 terminal at dg3.trade.

Sign in →