Using LLMs to Research Prediction Markets

You asked an AI model about a Senate race. It gave you a confident answer with structured reasoning, cited polling trends, and explained the competitive dynamics in the district. The answer was based on a primary that had concluded four months before the model’s knowledge cutoff. The redistricting that changed the district boundaries happened six months ago. The candidate the model was analysing had withdrawn from the race three weeks ago.

The model did not know any of this. It sounded exactly the same as it would have if it did.

That gap, between confident-sounding output and accurate output, is the entire terrain this guide covers. LLMs are genuinely useful for prediction market research in specific conditions. They are genuinely dangerous in others. The line between the two is not obvious from the output. It has to be built into how you use the tool.

Quick Answer

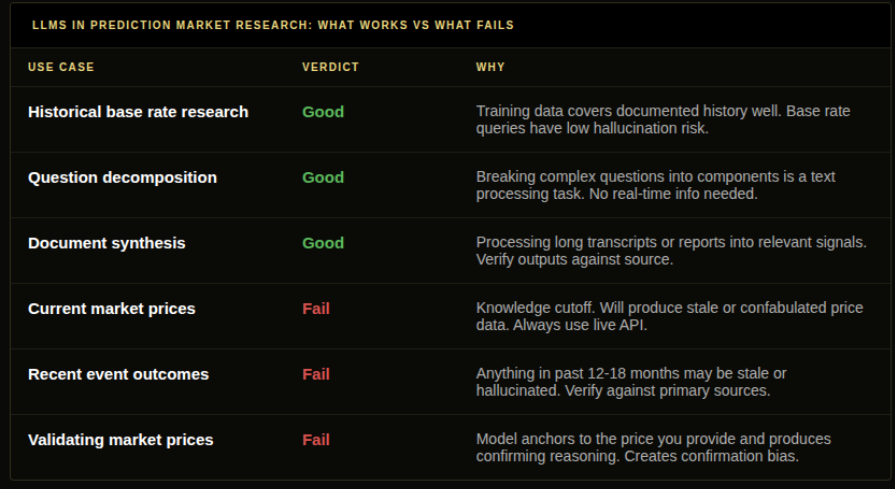

LLMs are useful for three specific research tasks: synthesising historical context on well-documented questions, decomposing complex probability estimates into components, and extracting analytical signals from long documents like transcripts or regulatory filings. They are dangerous for three specific reasons: knowledge cutoffs make them unreliable on anything that changed in the past 6-18 months, hallucination risk means specific factual claims need primary source verification, and confident-sounding output masks genuine uncertainty. Use LLMs as research accelerators, not as probability oracles. The model cannot tell you what is currently true. It can help you think about what was historically true.

Key Takeaways

- Every LLM has a knowledge cutoff. After that date, the model has no information about what happened in the world. For most current models, that cutoff is somewhere in 2024. Any Polymarket market on a current real-world event involves developments the model cannot access, and the model will not announce this limitation unless specifically prompted.

- LLM hallucination on specific factual claims is frequent enough to treat as a default risk, not an exception. A plausible-sounding statistic, historical precedent, or research citation from an LLM may be partially or entirely invented. Every specific claim needs primary source verification before it enters a trading decision.

- The strength of LLMs is text processing at scale. Reading 20 analyst reports, identifying historical precedents across large document collections, and structuring a probability estimate into components are tasks where LLMs add real value. These are research accelerators, not independent forecasters.

- The five prompting rules that reduce error: ask for base rates before predictions, ask for counterarguments before accepting a directional estimate, specify the knowledge cutoff explicitly and ask the model to flag potentially stale claims, ask for uncertainty ranges rather than point estimates, and verify every specific factual claim before using it.

- Using an LLM to validate a market price you already have in your head produces confirmation bias, not independent analysis. The model anchors to the number you provide and constructs reasoning that supports it. This is not a check on the market price. It is a mirror of your prior.

- DG3’s AI research layer is built around these constraints: AI for research structuring and context synthesis, live market data for everything current. The failure modes of LLMs are addressed by limiting their role to the tasks where their strengths apply.

What LLMs Are Actually Good For

Most traders who try using LLMs for prediction market research make the same mistake. They ask the model what will happen. That is the wrong question.

The right questions are ones where the model’s training data is an asset, not a liability.

Historical base rate research

“What is the historical rate at which incumbent senators lose primaries to challengers from their own party, controlling for approval ratings below 45%?”

This question has a well-documented historical record. The model can retrieve patterns from decades of political data with reasonable accuracy. The answer helps set a base rate before any current-cycle analysis. And it cannot be materially changed by events from the past six months, because base rates require historical data, not recent data.

The superforecaster methodology starts with base rates before current context. LLMs make that first step fast and comprehensive in a way that individual research cannot match.

Question decomposition

“Break down the question ‘Will the Fed hold rates at the September meeting?’ into its component parts and identify what evidence bears on each part.”

The model cannot tell you the answer. What it can do is help you structure the analytical problem: which inflation indicators are most predictive of Fed holds, what previous statement language patterns preceded similar decisions, what the Fed’s reaction function looks like given the current employment data. The structure is the value. You fill in the current data yourself.

Document synthesis

A 3-hour Senate committee hearing transcript is a lot to process. A regulatory filing from a pharmaceutical company is dense. A central bank speech is full of coded language. LLMs can extract the analytically relevant signals from long documents efficiently. The limitation is that the model cannot contextualise them against what happened after the document was produced. You add that context.

Identifying blind spots

“What factors might I be underweighting in my analysis of this market?” is a legitimate question for an LLM. The model has been exposed to a wider range of analytical frameworks than most individual researchers. It can surface considerations that are not top of mind from your current framing.

What LLMs Are Dangerous For

Current factual claims

“What is the current Polymarket price on the 2026 midterms?” The model will either state that it does not have current information (if it is well-behaved) or confabulate a plausible-looking price from its training data. Both outcomes are bad. Use the live feed for anything current.

Recent events since the knowledge cutoff

Anything that happened in the 6-18 months before you are asking the question may fall into the cutoff gap. The model will not announce the boundary. It will generate text that sounds like confident analysis of recent events, sourced from training data that ends before those events occurred.

Specific numerical claims without citations

“What percentage of Fed meetings in the last decade ended in a hold when core PCE was above 3%?” A number will appear. It may be right. It may be wrong by 15 percentage points. There is no way to tell from the output. Every specific number from an LLM requires verification against a primary source before it enters any calculation.

Validating market prices you already hold

This is the most expensive failure mode. You see a market at 0.58. You think it should be 0.65. You ask the model: “Does 58% probability seem right for this outcome?” The model anchors to 58%, constructs coherent reasoning around it, and you walk away feeling confirmed. You have not analysed the market. You have generated confirmation bias dressed up as independent analysis. Your estimate and the model’s estimate are not independent data points. They are the same data point with extra steps.

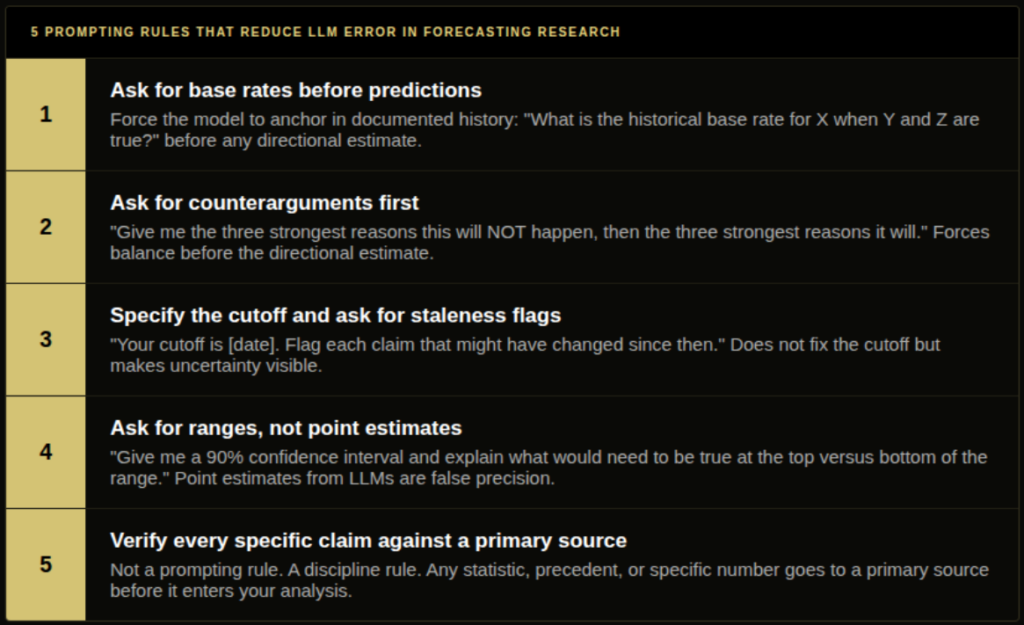

The 5 Prompting Rules

Rule 1: Ask for base rates before predictions

Bad prompt: “What is the probability that the Fed holds rates in September?”

Better prompt: “What is the historical base rate of Fed rate holds when core PCE is above 3%, unemployment is below 4%, and the most recent FOMC statement used language suggesting patience? Then apply this base rate to the current situation.”

The base rate anchor prevents the model from generating a probability from general vibes about the current macro environment. It forces a disciplined starting point.

Rule 2: Ask for counterarguments before accepting directional estimates

Bad prompt: “Give me reasons to be confident that Candidate X wins.”

Better prompt: “First give me the three strongest reasons Candidate X will not win. Then give me the three strongest reasons they will. Then give me a calibrated probability estimate that weights both.”

Models produce confirmation bias on directional prompts. Explicitly requesting counterarguments first forces the model to search for disconfirming evidence before settling on a direction.

Rule 3: Specify the knowledge cutoff and ask for staleness flags

Bad prompt: “What do you know about the current state of AI regulation in the EU?”

Better prompt: “Your knowledge cutoff is approximately [date]. What do you know about EU AI regulation as of that date? Flag each specific claim that might have changed since the cutoff, and note what developments you would need to check to verify the analysis is still current.”

This does not fix the cutoff. It makes the model’s uncertainty visible, which is the minimum viable protection against acting on stale analysis.

Rule 4: Ask for uncertainty ranges, not point estimates

Bad prompt: “What is the probability Candidate X wins the primary?”

Better prompt: “Give me a 90% confidence interval for Candidate X’s primary win probability, and explain what would need to be true for the actual probability to be at the top versus the bottom of that range.”

Point estimates from LLMs carry false precision. A stated “63% probability” implies a level of calibration the model does not have. A range with conditions makes the uncertainty structure visible.

Rule 5: Verify every specific factual claim before using it

This is a discipline rule, not a prompting rule. Any statistic, historical precedent, vote count, or specific fact that emerges from LLM research gets checked against a primary source before it enters your analysis. The model cannot be held accountable for being wrong. You can.

The Knowledge Cutoff Problem in Detail

Every LLM is trained on data collected up to a specific date. Events, decisions, and developments after that date are not in the model’s knowledge. The cutoff for most current production models falls somewhere in 2024.

For a prediction market trader, the specific implications are:

Any market about a current event involves developments that may post-date the cutoff. A model asked about an ongoing political race does not know who withdrew, who endorsed whom, or what the most recent polling showed. A model asked about a sporting event does not know the current season’s form, injuries, or managerial changes. A model asked about a regulatory decision does not know what was filed in the most recent submission period.

The model will fill these gaps. It will generate text that sounds like informed analysis. It will not announce that it is operating on incomplete information unless prompted to. The output has the same confident tone whether the model is drawing on accurate training data or confabulating plausible-sounding content.

The practical rule: treat any LLM output on events or conditions from the past 12-18 months as potentially stale and requiring verification. The closer to the present, the more verification is required.

The Hallucination Problem in Practice

LLM hallucination is the generation of plausible-sounding text that does not correspond to verifiable facts. It is not lying. The model does not know it is doing it. It is generating the most statistically likely next token given its training, and that process sometimes produces text that sounds like a citation but is not.

For prediction market research, the high-risk categories are:

Specific statistics. “Historically, incumbents seeking reelection after their party wins the previous cycle win 73% of contested primaries.” This number may be real, approximately right, or entirely invented. There is no way to determine which from the output alone. Check the primary source.

Named precedents. “In the 2018 Senate race in [state], a comparable dynamic led to a late surge for the challenger.” The race may have occurred. The dynamic may not match. Specific claims about specific events need verification.

Research citations. “A 2022 paper in the Journal of Political Economy found that…” The paper may not exist. The finding may be a composite of different studies the model has conflated. Verify before using.

The practice of verifying every specific claim is the most important single discipline for using LLMs in trading research. It is also the one most commonly skipped under time pressure. Do not skip it.

Common Mistakes

Asking LLMs to validate positions you already hold is the most expensive mistake. You have a probability estimate. You ask the model if it seems right. The model agrees. You feel more confident. Nothing useful has occurred. The model anchored to your number and generated supporting reasoning. That is not independent confirmation. It is the echo chamber operating with an academic tone.

Not specifying the knowledge cutoff in the prompt. Most models will not volunteer the staleness of their information. They answer confidently about “current” situations that are eight months out of date. Always ask the model explicitly to identify which parts of its answer might have changed since its cutoff.

Treating consistent-sounding reasoning as accuracy evidence. LLMs produce coherent, well-structured reasoning regardless of whether the underlying facts are correct. Coherence is a feature of text generation, not of accuracy. A beautifully structured argument built on a hallucinated statistic is still wrong.

Using LLMs for any research step that requires current information without providing that information explicitly. If you want the model to reason about current conditions, paste in the current data. Do not ask it to retrieve current data. It cannot. If you paste in the current injury report and ask the model to help you estimate its probability impact, you are using the tool correctly. If you ask the model what the current injury situation is, you are not.

How DG3 Helps

DG3’s AI research layer is built around the failure modes above rather than pretending they do not exist. The distinction between what AI handles (research structuring, historical context synthesis, question decomposition) and what the data infrastructure handles (current prices, real-time signals, fair value calculations, resolution criteria) is enforced at the architecture level.

Current market data, Fair Value Engine outputs, and real-time order flow from DG3’s Intelligence pane are all separate from the AI research layer. The AI is not asked to produce current market estimates. The data layer is not used for historical synthesis. Each tool does what it is good at.

For the broader context of where AI forecasting sits relative to prediction markets and superforecasters, read Prediction Markets vs AI: Which Forecasts the Future Better.

Frequently Asked Questions

Q: What are LLMs actually good for in prediction market research? A: Three specific uses: historical base rate research where the model’s training corpus covers documented history well, question decomposition where breaking complex forecasting questions into tractable components adds structure to the analysis, and document synthesis where extracting relevant signals from long transcripts or regulatory filings saves time. The common thread is using the model’s text-processing strength on questions where current information is not the deciding factor.

Q: What are the biggest risks of using AI for trading research? A: Knowledge cutoffs make LLMs unreliable on anything that changed in the past 6-18 months. Hallucination risk means specific factual claims need primary source verification. Confident-sounding output masks genuine uncertainty. Anchoring to market prices produces confirmation bias when you provide the current price and ask if it seems right.

Q: How do you prompt AI to reduce error in forecasting research? A: Five practices: start with base rates rather than predictions, explicitly request counterarguments before accepting a directional estimate, specify the knowledge cutoff and ask the model to flag potentially stale claims, ask for uncertainty ranges rather than point estimates, and verify every specific factual claim against a primary source before using it.

Q: What is an LLM knowledge cutoff and why does it matter? A: The knowledge cutoff is the date after which an LLM has no training data. For most current models it falls somewhere in 2024. Any Polymarket market on a current real-world event involves developments that occurred after the cutoff. The model will produce plausible-sounding analysis without being able to access those developments, and it will not announce this limitation unless specifically asked.

Q: How does DG3’s AI layer avoid LLM failure modes? A: By maintaining a strict separation between what the AI handles and what the data infrastructure handles. Research structuring, historical context, and question decomposition go to the AI layer. Current prices, real-time signals, fair value calculations, and resolution criteria come from the data infrastructure. The model is never asked to produce current market estimates. The failure modes are addressed by limiting the model’s role to the tasks where its strengths apply.

Q: How do I use ChatGPT for Polymarket research without being misled? A: Use it for historical context, base rate research, and question decomposition. Specify the knowledge cutoff in your prompt and ask it to flag potentially stale claims. Do not ask it for current prices, recent polling, or anything requiring information from the past 12-18 months. Verify every specific statistic or precedent against a primary source. Treat the output as a starting framework for your own analysis, not as the analysis itself.

Q: What are the best prompts for prediction market research with an LLM? A: Prompts that specify constraints. “As of your knowledge cutoff, what is the historical base rate for this outcome category?” “What are the three strongest reasons this might NOT happen?” “Give me a 90% confidence interval rather than a point estimate.” “Flag which of these claims might have changed since your knowledge cutoff.” Constraint-specifying prompts produce more reliable output than open-ended directional questions.

Final Thoughts

LLMs are genuinely useful research tools for prediction market traders who understand their limits. They are genuinely dangerous for traders who treat them as oracles.

The knowledge cutoff means they cannot tell you what is happening now. The hallucination risk means specific claims need verification. The confident tone means uncertainty is invisible unless you actively build prompts that surface it.

None of this means stop using them. It means use them for what they are good at. Process historical information. Decompose complex questions. Structure analytical frameworks. Then bring current data, live market prices, and real-time signals from your trading infrastructure to do what the model cannot.

The combination is more useful than either alone. The trap is using the model alone and forgetting that it is operating with a view of the world that is months out of date.

For the Information Asymmetry angle on why current information advantages persist in prediction markets, the article covers the mechanics of who knows what and when.