Prediction Market Data as Alternative Data: What Funds Actually Use It For

The portfolio manager had been watching a Polymarket FDA approval market for three weeks. When the YES price climbed from 0.44 to 0.61 over 48 hours with no public announcement, she did not wait for an analyst note. She added to her pharmaceutical equity position. Three days later the approval came through.

She was not trading Polymarket. She was using Polymarket pricing as a leading indicator for an equity position she already held. The crowd had better information, or a better aggregate model. Either way, the price moved before the announcement. She saw the move. She acted.

That is the institutional use case. Not trading prediction markets as a speculative asset class. Using prediction market data as a real-time probability feed for binary events that move other markets.

Quick Answer

Hedge funds and quant strategies use prediction market data primarily in five ways. As a leading indicator for correlated equity, fixed income, or macro positions. As an event probability input to options pricing models. As a political risk signal for cross-asset strategies. As a backtesting dataset for event-driven equity strategies. And as real-time thesis validation when an equity position depends on a binary event. Institutional data quality requirements go beyond what the free API provides, including verified timestamp accuracy, normalised cross-venue pricing, and delivery latency SLAs. DG3 provides a processed data layer that covers the analytical gap for most systematic traders.

Key Takeaways

- Prediction market data is alternative data in the technical sense: non-traditional, not produced by the company or asset being traded, and carrying information content that can lead or supplement conventional sources. The key property that distinguishes it from most other alternative data: it is probabilistic. A devigged Polymarket price is a directly usable event probability estimate, not a sentiment score that requires conversion.

- The primary institutional use case is not trading prediction markets directly. It is using prediction market prices as probability inputs to cross-asset strategies. A presidential election market is a real-time probability estimate for an event that affects every asset class simultaneously. A pharmaceutical approval market is a probability estimate for an event that directly affects one stock’s expected value.

- Thin market problem. A Polymarket market with $20,000 in total volume does not carry the same information content as one with $5 million. Institutional users filter by minimum liquidity thresholds before including any market’s price in a signal. Applying the same weight to a thin market and a liquid one produces noisy signals.

- Data quality at the institutional level requires verified timestamp accuracy, clean bid-ask data with spread metadata, normalised cross-venue pricing between Polymarket and Kalshi, historical data with settlement verification, and delivery latency SLAs. The free API provides the raw data. It does not provide the processing. The gap between them is where commercial data products add value.

- Prediction market prices carry a specific weakness that institutional users account for: partisan bias on political markets. In high-emotion election cycles, prediction market prices are partially driven by emotionally invested capital rather than purely by probability estimation. Institutional models apply discounts to political market prices during partisan peak periods.

- DG3’s processed data layer provides fair value calculations, spread metadata, and edge rankings as a starting point for systematic strategies without requiring the trader to build the processing infrastructure from scratch.

Why Prediction Market Data Is Alternative Data

Alternative data is any data source that is not directly produced by the company or instrument being analysed but carries information content beyond conventional sources. Satellite imagery of retail parking lots. Credit card transaction aggregates. App download rankings.

Prediction market data fits this definition with one property that most alternative data lacks: it is directly probabilistic. A devigged Polymarket YES price of 0.63 is a 61.8% probability estimate (after removing the bid-ask spread) for the named outcome. That number slots directly into expected value calculations, options pricing models, and scenario-weighted portfolio construction. Most alternative data requires transformation into a probability before it can be used this way. Prediction market data arrives as a probability.

The second distinguishing property: real-time updating. Satellite imagery is collected periodically. Credit card data is aggregated with a lag. Prediction market prices update with every transaction, continuously. When new information enters the market, the price reflects it within minutes on liquid markets.

The third property: verifiability. Every Polymarket price is backed by an on-chain transaction on Polygon. The data cannot be quietly revised after the fact. This matters for institutional users who need to audit their data pipeline against original sources.

These three properties make prediction market data particularly well-suited to event-driven strategies where binary event probabilities are the operative variable.

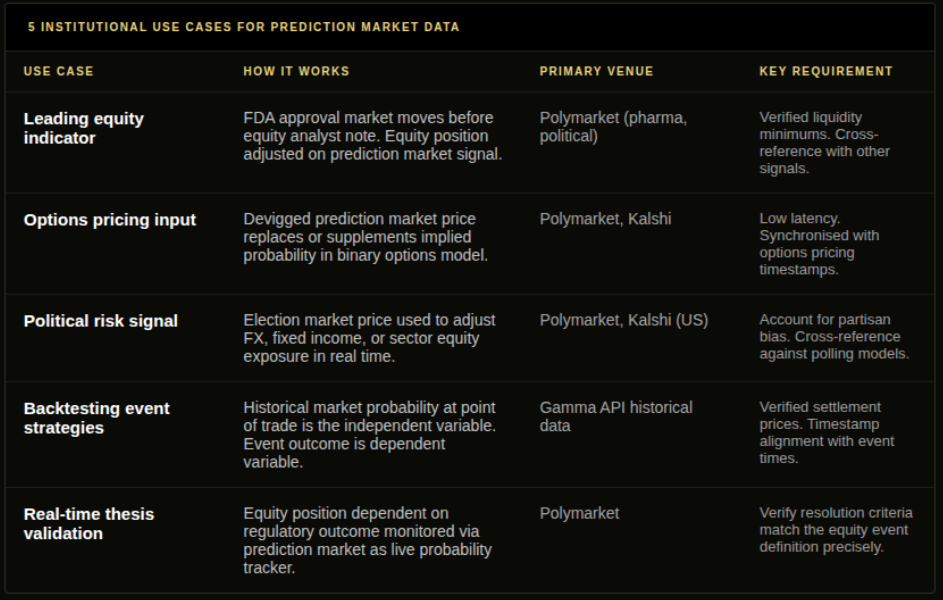

The 5 Institutional Use Cases

Use Case 1: Leading Indicator for Correlated Equity Positions

The FDA approval example in the opening is the clearest version. When a pharmaceutical approval market on Polymarket moves from 0.44 to 0.61 over 48 hours without any public announcement, it signals that the aggregate of informed traders believes approval probability has increased. If the underlying equity moves 30% on approval, that probability shift represents a material change in expected equity value.

The same structure applies to political events and policy-sensitive sectors: an election outcome market moving before polling consensus shifts is a signal for defence, energy, or healthcare equities that depend on which party controls regulation. A central bank decision market moving before the meeting represents informed capital taking positions on rate-sensitive fixed income.

The caveat: thin markets on this theme carry low signal. A $30,000 volume market moving from 0.44 to 0.61 may reflect $10,000 of informed capital or $10,000 of uninformed speculation. Institutional users cross-reference with order book quality data before acting on any single market movement. DG3’s wallet classification data makes this cross-reference faster.

Use Case 2: Event Probability Input to Options Pricing

Binary options pricing models require an estimate of the probability that the binary event occurs. Prediction market prices, after devigging, provide exactly this input in a live, continuously updating format.

A pharmaceutical company trading with an options structure ahead of a binary FDA decision has implied volatility that depends on the market’s probability estimate for the approval. If the prediction market price implies 68% approval probability and the options market is pricing the event as if the probability were 55%, there is a discrepancy that options strategies can exploit through positions that go long the event’s volatility at the lower implied probability.

This cross-asset application requires low-latency, verified prediction market data synchronised with options pricing. The free API tier’s variable latency makes this challenging without additional processing infrastructure.

Use Case 3: Political Risk Signal for Macro Positions

Election outcome markets, legislative passage markets, and regulatory decision markets are direct probability estimates for events that affect currencies, fixed income, and equity markets simultaneously.

A fund with exposure to US interest rate policy uses Polymarket FOMC decision markets as a real-time probability estimate for rate changes, supplementing Fed Funds futures market implied probabilities. When the two diverge, it is an arbitrage opportunity or a signal that one market is mispricing the event. The prediction market provides a second, independent probability estimate from a different pool of capital.

Emerging market currency exposure that depends on election outcomes in a specific country can be adjusted in real time using prediction market prices as a live probability tracker. The prediction market’s speed advantage over polling consensus means it provides probability updates faster than traditional political risk frameworks, which typically update on weekly or biweekly polling cycles.

Use Case 4: Backtesting Event-Driven Equity Strategies

A quant fund building a systematic event-driven equity strategy needs historical data on event probabilities at the time of the trade, not the benefit of hindsight. Prediction market historical data from the Gamma API provides this: the market’s probability estimate for each event at any point in time, going back to the market’s creation date.

Building a model that trades equities based on FDA approval probabilities, election probabilities, or earnings outcome probabilities requires historical prediction market data as the independent variable. The outcome (the event resolved YES or NO) is the dependent variable. The full time series of historical probability estimates is available from the Gamma API at no cost. The Polymarket API guide covers the data structure in detail.

Use Case 5: Real-Time Thesis Validation

An equity fund holds a long position in a company whose value depends on a specific regulatory outcome. Rather than waiting for analyst estimates to update (which happens slowly and with meaningful lag), the fund monitors the Polymarket market on the regulatory decision as a real-time tracker of probability consensus.

When the prediction market price falls 8 cents in a single session, the fund reassesses their equity position without waiting for an analyst downgrade. The prediction market is faster than the research cycle by days or weeks. That speed advantage translates directly to earlier risk management decisions.

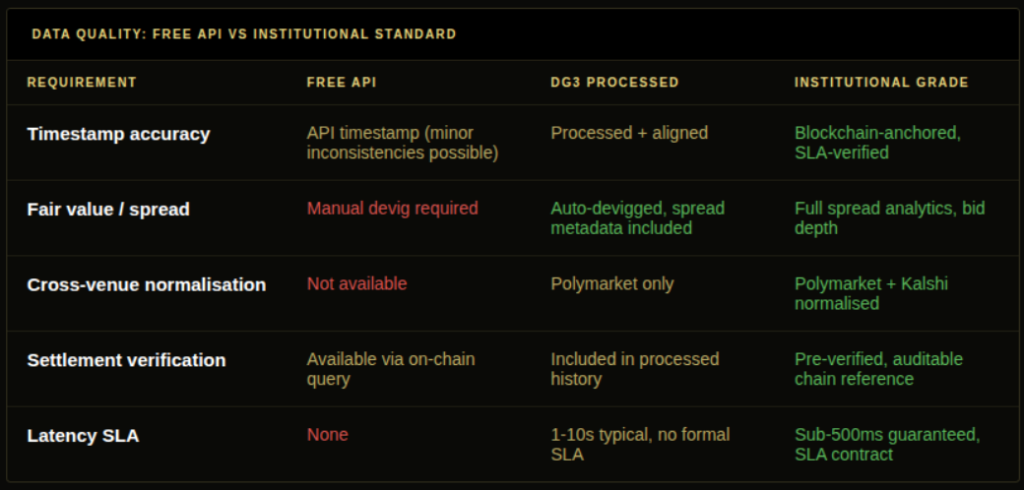

Data Quality Requirements at the Institutional Level

The gap between what the free Polymarket API provides and what institutional data pipelines require explains why commercial prediction market data products exist.

Timestamp accuracy. Institutional strategies depend on knowing precisely when a price occurred. The Polymarket API provides timestamps, but the relationship between the API timestamp and the actual blockchain confirmation time can have inconsistencies during high-traffic periods. Institutional data requires verified, blockchain-anchored timestamps.

Spread metadata. The fair probability of an event requires correctly capturing the bid-ask spread and applying the devig calculation. Raw API data provides transaction prices but requires additional processing to produce clean midpoints and spread metrics.

Cross-venue normalisation. Equivalent questions on Polymarket and Kalshi have different contract structures, different fee structures, and different liquidity profiles. Comparing prices across venues requires normalisation that converts both to a comparable probability scale.

Historical depth with settlement verification. Backtesting requires historical data with verified settlement prices against on-chain records. The Gamma API provides this data but confirmation against blockchain records adds overhead.

Latency SLAs. Institutional strategies that need to act within seconds of a prediction market signal require guaranteed delivery latency. The free API provides no guarantees. Commercial providers with dedicated infrastructure provide contractual SLAs.

Common Mistakes

Using thin market prices as institutional-grade signals is the most common error. A $20,000-volume Polymarket market is not providing the same information content as a $5 million market. Apply minimum liquidity thresholds before including any market’s price in a systematic strategy. A market that does not clear the threshold may still be worth monitoring manually, but it should not be feeding automated signals.

Not accounting for partisan bias on political markets. During high-emotion election cycles, prediction market prices on political questions are partially driven by capital that is emotionally invested rather than purely probability-motivated. Institutional users discount political market prices relative to other data sources during these periods, or they cross-reference against polling-derived probability models to identify when the divergence is outside normal range.

Building a cross-asset signal on prediction market data without backtesting the historical correlation. The hypothesis that prediction market prices lead equity or other market movements is plausible but requires empirical validation on the specific event type and asset class being traded. Not all prediction market movements have historically preceded corresponding asset movements.

Frequently Asked Questions

Q: Do hedge funds use prediction market data? A: Yes, at a growing number of funds. The use cases range from event probability inputs to options pricing models to leading indicator signals for correlated equity positions. The adoption is still early relative to other alternative data categories, partly because institutional-grade cleaned prediction market data products are a relatively recent development, and partly because the thin-market problem limits which specific markets carry enough signal to be useful.

Q: What are the institutional use cases for prediction market data? A: Five primary cases: leading indicator for correlated equity positions, event probability input to options pricing models, political risk signal for macro positions, backtesting data source for event-driven equity strategies, and real-time thesis validation for equity positions dependent on binary event outcomes.

Q: How does prediction market data compare to traditional alternative data? A: It is probabilistic rather than transactional or sentiment-based. It provides a directly usable event probability estimate that updates continuously, produced by financially incentivised participants, and is on-chain verifiable. Most other alternative data requires transformation into a probability before it can be used in expected value calculations. Prediction market data arrives in that format.

Q: What data quality standards do institutions require? A: Verified timestamp accuracy, clean bid-ask data with spread metadata, normalised cross-venue pricing between Polymarket and Kalshi, historical data with settlement verification, and delivery latency SLAs. The free API tier provides raw data without this processing.

Q: How does DG3 provide institutional-grade data access? A: DG3 provides a processed Polymarket data layer with devigged fair value calculations, spread metadata, and edge rankings. The core data engineering is inside DG3’s infrastructure. For institutional requirements including latency SLAs and full cross-venue normalisation, DG3 is the starting point for a data pipeline rather than the complete institutional product.

Q: What is an event probability signal in quant fund context? A: A prediction market price, devigged to a clean probability, used as an input variable in a quantitative model. For example: a fund’s options position on a pharmaceutical stock incorporates the Polymarket FDA approval probability as a variable in the binary options pricing formula. As the prediction market probability changes, the model recalculates the fair value of the options position. The prediction market price is the live input. The options repricing is the trade.

Q: What is prediction market alpha and how do funds capture it? A: Prediction market alpha is the return generated by trading correlated assets based on prediction market price movements that lead conventional price discovery. A fund that adds to pharmaceutical equity based on rising FDA approval market probability, before the equity market has fully priced the probability change, is capturing prediction market alpha. The alpha exists because the prediction market aggregates and prices information faster than conventional research consensus.

Q: Do prediction market prices lead equity market prices? A: In documented event categories, yes. The evidence is strongest on pharmaceutical FDA decisions, where Polymarket approval markets have shown leading price discovery ahead of equity markets on specific approval events. The evidence on election markets is more mixed, partly because of partisan bias and partly because equity markets themselves price political risk in advance through other channels. The leading relationship needs to be validated empirically for each specific event category before being used as a systematic signal.

Final Thoughts

Prediction market data is not yet mainstream alternative data at the institutional level. The liquidity constraints, thin-market reliability issues, and infrastructure immaturity mean it is a specialist tool rather than a standard quant factor.

The trajectory is clear. Polymarket volume has grown substantially each year since 2020. The event categories covered are expanding. The data infrastructure is maturing. Funds that build their prediction market data pipelines now will have backtested track records and calibrated use cases before the data becomes crowded.

The fundamental value proposition does not change regardless of scale. Prediction markets price binary events faster than conventional research. That speed advantage translates to leading indicators that are usable in both direct prediction market trading and cross-asset institutional strategies.

The question is not whether this data is valuable. The question is whether you have the infrastructure to use it before the edge prices in.

Also read – The Polymarket API: What Data You Can Pull and What to Build With It

Correlated Markets in Prediction Markets: Managing Portfolio Risk, Market Efficiency in Prediction Markets: Are They Really Smarter Than the Crowd?