Trading the News: An Event Driven Playbook for Prediction Markets

The Fed statement landed at 2:00 PM. By 2:03 PM the Polymarket rate-hold market had moved 11 cents. By 2:07 PM it had given back 4 of them. The traders who were positioned before 2:00 made money. The traders who read the headline and clicked buy at 2:04 paid for the correction.

Event-driven trading is not about reacting to news. It is about knowing what the news will change and being in the market before it does. The difference between those two things is the entire edge.

Quick Answer

Event-driven trading in prediction markets means taking positions around specific catalysts: scheduled announcements (Fed meetings, injury reports, election filings), breaking developments (transfers, court rulings, roster changes), and recurring patterns (post-news overreactions that fade within hours). The strategy works because prediction markets reprice faster than most traders can act, but interpretation of that repricing is slower than the initial price move. Pre-event positioning and post-event fade are the two primary strategies. The Edge Decay guide covers how fast different event types close.

Key Takeaways

- Event-driven trading works because prediction markets have a two-speed repricing mechanism: the initial price move is fast (seconds to minutes), but the interpretation of whether that move is correct takes longer. The gap between the two is where edge lives.

- Three event types create the best prediction market opportunities: scheduled catalysts with known timing (FOMC, injury reports), breaking developments with primary source verification gaps, and post-event fades where the initial market reaction overshot the genuine probability update.

- Pre-event positioning requires a probability model that diverges from the current market price before the catalyst arrives. If your estimate and the market’s estimate are the same, there is no edge to capture regardless of how the event resolves.

- Post-event fade is the most systematic strategy: when a Polymarket market moves sharply on news, the initial move frequently overshoots the true probability update. Buying the fade 15-30 minutes after the initial reaction has a positive historical expectation on liquid markets.

- Cognitive load is the primary execution risk. Fast-moving event markets require rapid decisions on incomplete information. A pre-built decision framework eliminates the mid-event thinking that causes hesitation. Read Cognitive Load in Fast Markets before running any event-driven strategy live.

- DG3’s Intelligence pane and Edge Finder reduce the gap between event arrival and execution decision. The Edge Finder shows the affected markets with live EV calculations. The Intelligence pane adds order book depth and whale activity context for the selected market.

Why Event-Driven Trading Works in Prediction Markets

Prediction markets have a structural feature that traditional financial markets do not: every market is about a specific, binary, verifiable event. That specificity means the probability implications of any new information are usually clearer than in equity or forex markets where the causal chain is long and diffuse.

When a starting goalkeeper is ruled out 90 minutes before kick-off, the probability impact on the match winner market is direct and calculable. The market has to move. The question is by how much and how fast. A trader who has a model of that specific goalkeeper’s contribution to their team’s defensive structure has a genuine edge over a trader who just sees the headline and reacts.

This is why event-driven strategies work better in prediction markets than almost anywhere else. The cause-effect relationship between information and probability is tighter. The window between information arrival and correct repricing exists on every market for every event type. The strategy is systematic exploitation of that window.

Three factors determine how exploitable any specific event window is: the predictability of the catalyst timing, the clarity of the probability implication, and the liquidity of the market in question. All three matter. A highly predictable catalyst (FOMC meeting) on an ambiguous market (will the statement be dovish?) in thin liquidity produces a different playbook than a predictable catalyst (injury report deadline) on a clear market (match winner) in deep liquidity.

The 3 Event Types That Create the Best Opportunities

Scheduled Catalysts

These are the highest-value event type for systematic traders because the timing is known in advance and the research can be done before the window opens.

FOMC meetings, NFL injury report deadlines, election filing dates, regulatory decision dates, and earnings announcements all have known timing. A trader who has built a probability model before the catalyst arrives can position days in advance, let the market come to them, and exit when the event reprices.

The edge in scheduled catalysts is not reaction speed. It is model quality. The trader who has a better model of how the Fed will respond to the current combination of inflation data and forward guidance language will be positioned correctly when the statement arrives, regardless of whether they are the first to read it.

The key discipline: do not build your model after looking at the current market price. The market price is the average of all current models. If you build your model by looking at the market first, your model will resemble the market’s, and the edge will be zero.

Breaking Developments

These are the highest-value edge per minute but the hardest to exploit systematically. A transfer confirmation from Fabrizio Romano, a court ruling that comes without advance scheduling, a sudden withdrawal from a political race: each creates an immediate repricing opportunity that exists for minutes on liquid markets and hours on thin ones.

The trader advantage in breaking developments is information infrastructure. A trader who monitors primary sources (official team channels, court dockets, election commission filings) rather than secondary aggregators (sports news sites, political news websites) will see the information minutes before the market fully prices it.

The discipline: have the Polymarket market already open in your workspace for every event you are tracking. The time cost of navigating to the market after information breaks on a liquid market is often the entire edge window.

Post-Event Fades

This is the most underused and most systematic of the three strategies. When a Polymarket market moves sharply on news, the initial move is frequently larger than the genuine probability update warrants.

Why this happens: the first wave of traders to react to news are often the fastest, not the most accurate. They push the price to a new level based on the headline. The slower, more analytical traders who read the full context then assess whether the initial move was correct. On liquid markets, the period 10-30 minutes after a sharp news move is when the correction occurs if the move overshot.

The post-event fade has a systematic positive expectation when three conditions are met: the initial move was driven by news (not whale order flow or a sharp line move from a reference book), the market is liquid enough that your fade position can be exited before resolution, and the news interpretation is genuinely ambiguous rather than directionally clear.

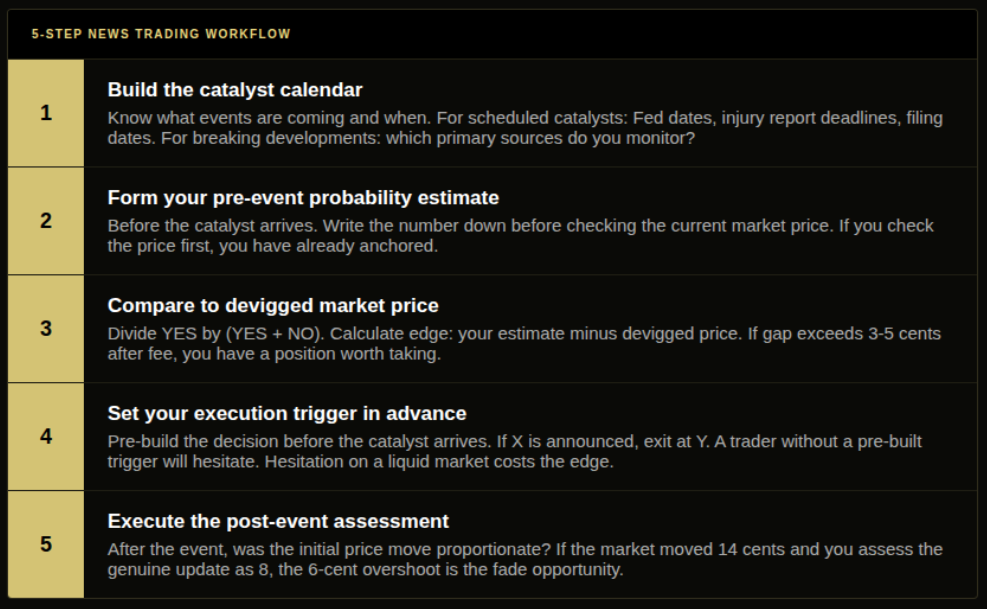

The 5-Step News Trading Workflow

Step 1: Build the catalyst calendar. Every event-driven strategy starts with knowing what events are coming and when. For scheduled catalysts, this is straightforward: Fed meeting dates, injury report deadlines, filing dates, and regulatory decision dates are all publicly available. For breaking developments, the calendar is about monitoring infrastructure: which primary sources cover your event categories, and how are you tracking them?

Step 2: Form your pre-event probability estimate. Before the catalyst arrives, estimate the probability of each possible outcome independently. For a Fed meeting: what is your estimate of the probability of a hold, given current inflation data, employment data, and forward guidance language? Write the number down before checking the current Polymarket price. If you check the price first, you have already anchored.

Step 3: Compare your estimate to the devigged market price. After forming your independent estimate, check the current Polymarket price and devig it (divide YES by YES plus NO). Calculate your edge: your estimate minus the devigged price. If the gap exceeds your minimum viable threshold (typically 3-5 cents on a 0.50 market after the 2% fee), you have a pre-event position worth taking.

Step 4: Set your execution trigger. For scheduled catalysts, set a clear decision rule before the catalyst arrives: if the announcement is X, my position has a genuine probability estimate of Y, and I will exit if the market moves to Z. Pre-building the decision eliminates the cognitive load of deciding under pressure. A trader without a pre-built trigger will hesitate. Hesitation on a liquid market costs the edge.

Step 5: Execute the post-event assessment. After the event, assess whether the initial price move was proportionate to the genuine probability update. If the market moved 14 cents on news that you assess warranted an 8-cent update, the 6-cent overshoot is the fade opportunity. Enter counter to the excess and exit when the market corrects to your estimated fair value.

Pre-Event Positioning: The FOMC Example

Federal Reserve meetings are the canonical scheduled catalyst for macro prediction markets on Polymarket. Every aspect of the playbook applies cleanly.

Six weeks before the September 2026 FOMC meeting, the Polymarket “Will the Fed hold rates?” market is trading at 0.58 YES. The trader’s process:

Read the most recent FOMC minutes, the July CPI data, and the most recent set of Fed official speeches. Assess the language pattern relative to previous periods when the Fed held versus cut. Form a probability estimate: 71% hold.

Devig the current market price: YES 0.58, NO 0.44 (total 1.02). Fair YES = 0.58 / 1.02 = 56.9%.

Edge: 71% minus 56.9% = 14.1 cents. At half Kelly on a $2,000 bankroll, the position is approximately $280 YES.

The catalyst arrives at 2:00 PM on September 17. The Fed holds. The market moves from 0.58 to 0.88. The position was entered at 0.58 and the market has now resolved. Profit: $0.42 per share times 280 shares = approximately $118 net before fees.

The model was correct. But the model would have been correct even if the Fed had cut (in which case the position would have lost), because the edge was in the probability estimation, not the outcome. Over 50 similar positions with similar edge, the arithmetic takes over.

Post-Event Fade: The Sports Injury Example

A starting centre-back for a Premier League team is confirmed out 2 hours before kick-off. The team’s match winner market on Polymarket moves from 0.52 to 0.39. Thirteen cents in 8 minutes.

The trader’s fade assessment: the centre-back’s replacement is a competent squad player who has started 6 matches this season. The team’s defensive structure does not depend heavily on this specific player’s individual qualities. A genuine probability update from this injury is probably 5-7 cents, not 13. The market has overshot.

Enter YES at 0.39, targeting an exit at 0.44-0.46 when the market digests the full context. Over the next 20 minutes, the market recovers to 0.43 as more-informed football traders assess the replacement quality. Exit at 0.43. Profit: 4 cents per share on the fade.

The fade works not because you predicted the outcome but because you correctly assessed that the initial market reaction overshot the genuine probability update.

Common Mistakes

Mistake 1: Reacting to news rather than positioning before it. Most retail traders on Polymarket trade news reactively: they see a headline, form a quick opinion, and click buy. On a liquid market, the first-wave reaction has usually finished by the time a retail trader processes the headline. They are buying the momentum of traders who were faster, not capturing the information signal. Pre-event positioning removes this problem entirely.

Mistake 2: Treating all sharp price moves as post-event fade opportunities. A sharp price move is a fade candidate only when it was driven by news-reaction momentum. A sharp price move driven by whale order flow from historically accurate wallets, or by a sharp reference book line move, is a different signal entirely and should not be faded. Check the source of the move before assuming overshoot.

Mistake 3: Not having the market open before the catalyst arrives. On a liquid Polymarket market with a scheduled catalyst, the price often starts moving in the 2-5 minutes before the official announcement as traders who have seen pre-release signals act. A trader who navigates to the market after the announcement has missed the best entry. Pre-event positioning requires having the market open and watched before the catalyst window.

Mistake 4: Building probability estimates after looking at the market price. This is the anchoring mistake. If you see the market at 0.58 and form a 0.63 estimate, you have not built an independent model. You have built a marginal displacement from market consensus. Your edge is the gap between an honest independent estimate and the market price, not the gap between a market-anchored estimate and the market price.

Mistake 5: Fading without a planned exit price. Post-event fades require a target exit price determined before entry, not after. A fade entered at 0.39 targeting 0.44 should be exited at 0.44 regardless of whether you think it will keep going. Fades that are held beyond the target become directional bets on the outcome, which is a different strategy with different risk.

How DG3 Helps

Event-driven trading has one dominant constraint: time between information arrival and execution decision. On liquid Polymarket markets, that window is measured in minutes for news events. The trader who has to navigate to the news, assess the market, and then find the right Polymarket market is systematically behind.

DG3’s Edge Finder shows which markets are moving, ranked by the size of the gap between current price and fair value. When a central bank statement drops and a rate-decision market reprices, the Edge Finder updates the EV ranking in real time so the affected market rises to the top. The Intelligence pane, open on the selected market, shows the order book depth and whale activity that confirm whether the move is informed capital or reactive noise.

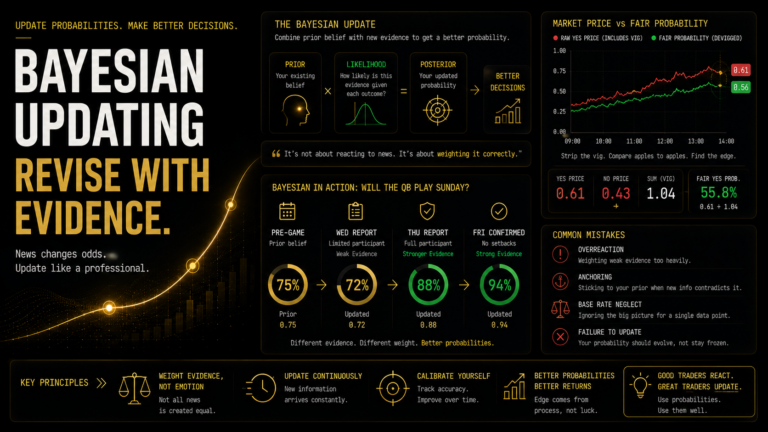

The Bayesian Updating guide covers the correct probability revision process when news arrives. The Information Asymmetry guide covers why some traders consistently get to events before the market.

Frequently Asked Questions

Q: Why does event-driven trading work on prediction markets? A: Because prediction markets reprice specific binary events, and the cause-effect relationship between new information and probability is tighter than in most financial markets. When a clear catalyst arrives, the market must reprice. The edge is in knowing the correct new probability before the market fully reflects it, either by positioning before the catalyst or by correctly assessing whether the initial reaction was proportionate.

Q: What types of events create the best prediction market trading opportunities? A: Three types: scheduled catalysts with known timing (FOMC, injury reports, election filing deadlines) where model quality determines edge. Breaking developments with primary source verification gaps, where faster information access creates edge. And post-event fades where the initial market reaction overshoots the genuine probability update and corrects within 15-30 minutes.

Q: How do you position before news breaks on Polymarket? A: Build your probability estimate independently before checking the current market price. Devig the market price to find fair implied probability. Calculate the gap between your estimate and the devigged price. If the gap exceeds the minimum viable edge threshold (typically 3-5 cents on a 0.50 market), enter the position. Have the market open and monitored before the catalyst window arrives.

Q: What is the post-event fade strategy? A: A post-event fade enters counter to a sharp news-driven price move on the assumption that the initial reaction overshot the genuine probability update. The strategy works when: the move was driven by news reaction (not informed whale order flow), the market is liquid enough to exit before resolution, and the news interpretation is genuinely ambiguous. Enter counter to the excess, target the correction to fair value, and exit at the pre-determined target price.

Q: How does DG3 give traders a timing edge on news events? A: DG3’s Edge Finder ranks all active markets by EV gap in real time, so when a news event reprices a market, that market rises to the top of the ranked list. The Intelligence pane on the selected market shows order book depth and whale activity simultaneously. The trader does not need to navigate across separate tools — market, EV calculation, and order flow context are in the same three-column view.

Q: How do you trade FOMC meetings on Polymarket? A: Six steps: read FOMC minutes and recent Fed official speeches before the meeting. Form an independent probability estimate. Devig the current price. Calculate edge. If edge exceeds threshold, enter the pre-event position. After the announcement, assess whether the market’s repricing was proportionate to the genuine probability update and take a fade position if it overshot.

Q: How do you trade before news breaks on Polymarket? A: Monitor primary information sources (official team channels, court dockets, regulatory filings) rather than secondary aggregators. Have the relevant Polymarket market open and watched before the expected announcement window. Use scheduled catalyst calendars to anticipate when information will arrive. Enter positions based on your pre-event probability model, not on the announcement itself.

Q: What is the news catalyst playbook for prediction markets? A: Build a catalyst calendar of scheduled events. Form independent probability estimates before checking market prices. Compare estimates to devigged market prices and enter positions with genuine edge. Set pre-built execution triggers before catalysts arrive to eliminate mid-event hesitation. Assess post-event price moves for overshoot and take fade positions when the initial reaction exceeded the genuine probability update.

Final Thoughts

Event-driven trading on prediction markets is not about being faster than the market. Most retail traders cannot be faster than the traders who have dedicated infrastructure for speed. The edge is in being more accurate about what the event means.

Pre-event positioning based on model quality. Post-event fades based on overshoot assessment. Both strategies require the same thing: an independent probability estimate built before the market price shapes your thinking.

The traders who do this consistently do not react to news. They wait for the market to react to news, assess whether the reaction was right, and take the position that the market’s first move got wrong.

That is the entire playbook. The Trading Signals guide covers which signal types feed best into each stage of this framework.