Order Execution Speed Trading: 3 Layers That Cost Prediction Market Traders Cents

The news broke at 14:23:04. A trader with a WebSocket connection and a pre-built trigger had a limit order in the CLOB by 14:23:05.2. She entered at 0.42. A second trader on a REST polling setup saw the price at 14:23:34 and clicked buy at 14:23:41. He paid 0.49.

Same trade thesis. Same prediction. Seven cents of difference in entry price. Both traders read the situation correctly. Only one profited from it.

Execution speed in prediction markets is not about being clever faster. It is about having the infrastructure to express the edge you already have before the edge closes. On event-driven trades, that window is measured in minutes. On information timing trades, it is measured in seconds.

Quick Answer

Execution speed in prediction markets is the total time from decision to confirmed fill, measured across three layers: data latency (how fast you receive price updates), order routing latency (how fast your order reaches Polymarket’s CLOB), and on-chain confirmation latency (Polygon block time, approximately 2 seconds, equal for all participants). A well-configured WebSocket setup achieves total execution in 200-800ms. A REST-polling manual-click setup takes 30-60 seconds. On markets moving at 0.5 cents per second, the difference between those two setups is 15-30 cents of entry price – often the entire edge window for an information timing trade.

Key Takeaways

- Execution speed only matters when the edge has a short shelf life. On a stable political market resolving in 8 weeks, a 30-second data lag costs nothing. On a breaking news event where the edge window is 90 seconds, that same lag can eliminate the position entirely before your order is submitted.

- The three latency layers compound. A 30-second data lag plus a 10-second manual click sequence plus a 4-second on-chain confirmation produces 44 seconds of total latency. On a market repricing at 0.5 cents per second, that is 22 cents of entry cost before slippage and fees. A 6-cent gross edge trade is deeply negative EV before a single share changes hands.

- The human click sequence is where most retail traders lose the most time. Read the signal, assess, navigate to the market, enter size, confirm: 8-15 seconds. DG3’s 1-Click Trade mode pre-configures the order type, Kelly fraction, and routing so the trader can execute with a single tap rather than working through the full form. That reduction in friction on a fast-moving event market is worth more than reducing network latency from 200ms to 80ms.

- Smart order routing is the practice of checking multiple venues before executing. On equivalent events where Polymarket and Kalshi both have active markets, prices can differ by 2-4 cents at any given moment. A 3-cent better entry on Kalshi versus Polymarket, captured by checking both venues before executing, compounds across every cross-listed event you trade.

- Sub-100ms execution matters for a specific subset of strategies: true arbitrage between correlated markets where the gap exists for under a second, and front-running of thin markets that update slowly. For most retail event-driven strategies, eliminating the human click latency (8-15 seconds) produces more edge recovery than cutting network latency from 300ms to 80ms.

- Speed without a model is worthless. A trader who enters 10 seconds faster than average with a bad probability estimate is losing money faster, not making money smarter. Infrastructure amplifies edge. It does not create it.

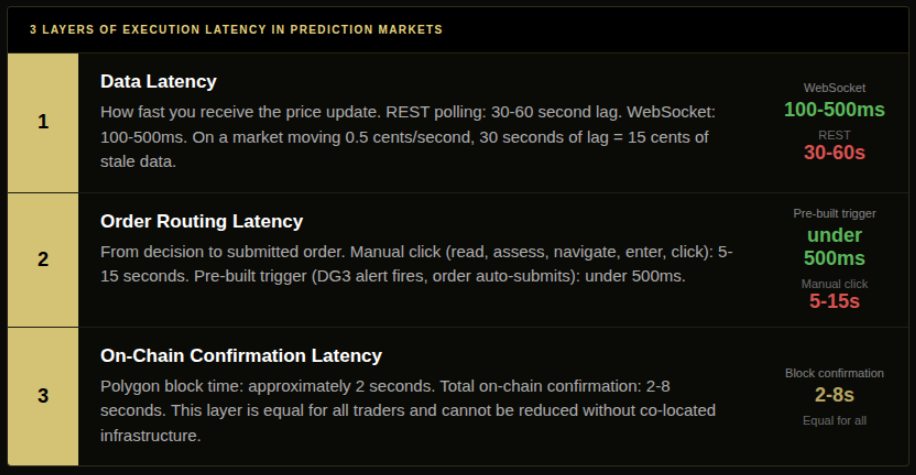

The 3 Layers of Execution Latency

Layer 1: Data Latency

How fast the price signal reaches you. This is where most retail traders leak the most.

REST polling at 30-second intervals means your price data is potentially 30 seconds old at any moment. During a news event where the market moves 9 cents in 75 seconds, 30-second polling means you see a pre-event price, decide at that price, and submit an order into a market that has already moved 3-6 cents past your decision point. You are not trading the current market. You are trading a market that existed half a minute ago.

WebSocket subscriptions deliver price updates within 100-500ms of each on-chain transaction. During the same 75-second repricing event, you are seeing the price continuously and making decisions on current data.

The performance difference between REST and WebSocket on stable slow-moving markets is negligible. On event-driven markets, it is the difference between the trade existing and the trade not existing.

Layer 2: Order Routing Latency

How fast your order travels from decision to the CLOB. This is where the human click sequence becomes visible as a cost.

Manual execution: read the signal, assess the market, navigate to the correct Polymarket market, enter position size, confirm the order. Total time: 8-15 seconds depending on how quickly the process runs. At 0.5 cents per second of market movement, that is 4-7.5 cents of timing slippage on the entry price before the order is even submitted.

DG3’s 1-Click Trade mode pre-configures the order setup so that when you decide to act, a single tap places the order rather than working through outcome selection, size entry, and method confirmation sequentially. Total time from decision to submitted order: under 2 seconds for most traders. The form friction disappears from the chain.

For most retail event-driven strategies, reducing order routing latency from 10 seconds to under 1 second produces more edge improvement than any other infrastructure investment. It is also cheaper and faster to implement than network-level optimisation.

Layer 3: On-Chain Confirmation Latency

Every Polymarket order is an on-chain transaction on Polygon. Block time on Polygon is approximately 2 seconds. Order submission to confirmation: typically 2-8 seconds.

This layer is equal for all participants on standard infrastructure. No retail trader has a meaningful advantage here without co-located nodes and real engineering investment. For event-driven strategies where the edge window is 90+ seconds, this layer is not the constraint. For true arbitrage strategies where the gap closes in under 5 seconds, it becomes the binding limit.

Speed Impact: The Dollar Math

The question that matters is not “how fast am I” but “how much does my current speed cost me on the specific trades I take?”

On a stable Polymarket Senate race market with 6 weeks to resolution, a 30-second data lag costs approximately 0.001 cents per share. Irrelevant.

On a market repricing at 0.5 cents per second after a FOMC statement:

- REST polling lag (30 seconds): 15 cents of entry price slippage

- Manual click sequence (10 seconds): 5 cents of additional slippage

- Total latency cost before on-chain confirmation: 20 cents

A trader with a 6-cent gross edge on this trade, operating on REST polling with manual execution, is executing at negative 14 cents net. The trade is not bad. The infrastructure made it unprofitable before it started.

Now the same trader with WebSocket data and a pre-built trigger:

- WebSocket data lag (300ms): 0.15 cents

- Pre-built trigger (400ms): 0.2 cents

- Total latency cost: 0.35 cents

Net edge after latency: 5.65 cents. After slippage and fees: probably 3-4 cents. That is a viable trade.

The infrastructure difference between these two scenarios: switch from REST polling to WebSocket, configure a pre-built alert trigger. Not expensive. Not technically complex. Just not the thing most traders think about.

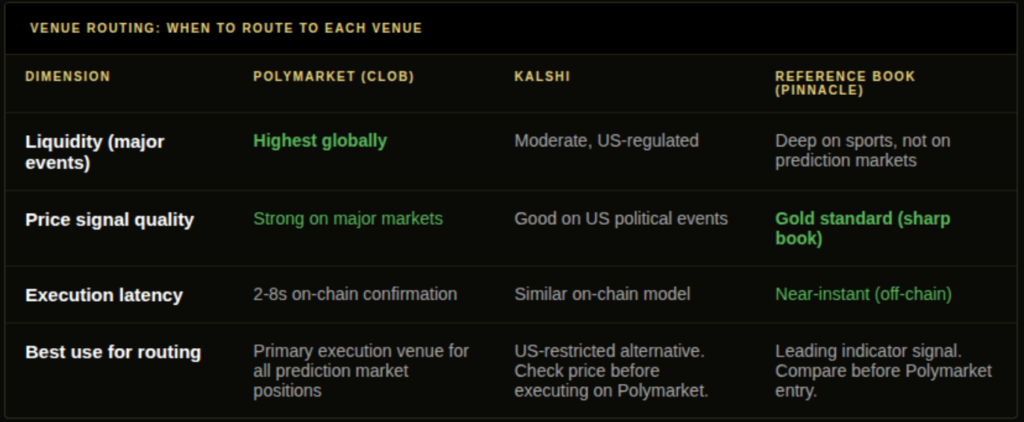

Checking Reference Books Before Executing

Before executing on Polymarket, the highest-value manual check for event-driven trades is comparing the Polymarket price against a sharp reference sportsbook’s implied probability on the same event.

On a sports event, Pinnacle’s devigged line is the gold standard for sharp-money pricing. When Pinnacle has moved before Polymarket, the Polymarket price is stale relative to where informed capital is pricing the event. That divergence is both a directional signal and potentially a 2-4 cent better entry on Polymarket before it catches up to the reference book.

This check takes 10-30 seconds manually: look up the Pinnacle line, devig it, compare against the current Polymarket price. It is worth doing on any event-driven trade where you are not in a sub-60-second execution window. The information is public and the process is the same every time.

DG3 Phase 0 operates on Polymarket. Cross-venue execution routing across Polymarket and Kalshi simultaneously is a planned future feature. In Phase 0, the reference book comparison is a manual research step before execution rather than an automated routing decision.

When Execution Speed Does Not Matter

This section matters as much as the one before it.

On a Polymarket legislative market resolving in 3 months, a 30-second data lag produces approximately zero additional edge decay. The price is not moving that fast. A limit order placed today fills at roughly the same price whether your infrastructure has 50ms or 30-second latency.

On a stable macro market with no pending catalysts, model accuracy is the constraint. A trader with better probability estimation on a slow-moving market will outperform a trader with faster execution and a worse model, every time, over any meaningful sample size. Speed amplifies the edge you have. It does not substitute for an edge you lack.

The frame: which of your specific positions have edge windows measured in seconds or minutes? For those trades, speed infrastructure matters. For everything else, the engineering budget is better spent on probability model quality than on millisecond improvements.

Most retail Polymarket traders would get more return from improving their signal research process than from cutting their execution latency from 10 seconds to 1 second. The order matters. Model first. Infrastructure second.

Common Mistakes

Optimising for execution speed on positions that are not time-sensitive is the most common infrastructure mistake. A trader who spends two weeks configuring a WebSocket setup primarily for long-horizon political markets will find that it saves approximately 0.05 cents per entry on positions that were never speed-constrained. The same infrastructure on event-driven sports and news markets saves 3-8 cents per entry. Know which category your trades fall into before deciding which bottleneck to address.

The second mistake is conflating data latency and total execution latency. WebSocket data with a manual click sequence still has 8-15 seconds of human routing latency. WebSocket data with pre-built triggers is fast. The two are not the same, and most discussions of “real-time data” skip over the click sequence as if it does not exist.

The third mistake is treating on-chain confirmation latency as reducible without major infrastructure investment. Polygon block time is approximately 2 seconds and is equal for all standard participants. Spending time optimising for sub-second confirmation without co-located infrastructure produces no improvement. The reducible latency layers are data receipt and order routing – the ones that are within reach of normal retail infrastructure.

How DG3 Helps

DG3’s Trade Desk operates on a WebSocket connection to Polymarket’s CLOB API. When a trader spots a signal, 1-Click Trade mode lets them execute with a single tap rather than completing the full order form, reducing the time from decision to submitted order from 10-15 seconds of form interaction to under 2 seconds.

The Intelligence pane tracks whale activity and order flow in real time for the selected market, making signal identification faster without requiring separate monitoring tools.

For most retail traders, the practical benefit is not sub-100ms execution. It is the reduction in form friction between spotting a signal and submitting the order – the layer where most event-driven edge leaks.

Frequently Asked Questions

Q: Why does execution speed matter in prediction markets? A: On time-sensitive positions, edge has a measured shelf life. A market repricing at 0.5 cents per second loses 15 cents of available entry price over a 30-second REST polling lag. A pre-built trigger operating on WebSocket data enters at 0.35 cents of timing cost on the same trade. The difference is whether the edge window was captured or missed.

Q: How much does a 50ms delay cost on a 6-cent edge trade? A: On a stable market: effectively nothing. On a fast-moving event market repricing at 0.5 cents per second: 0.025 cents per share – negligible. The scenario where sub-100ms matters is institutional arbitrage between correlated markets where gaps close in under a second. For retail event-driven strategies, the 8-15 second human click latency is the binding constraint, not the 50ms network latency.

Q: What is the multi-venue price check strategy in prediction markets? A: Before executing on Polymarket, checking a sharp reference sportsbook’s devigged price on the same event. When the reference book has moved before Polymarket, the Polymarket price is stale and the reference book’s direction is a signal. Checking takes 10-30 seconds. Automated cross-venue routing across Polymarket and Kalshi simultaneously is a planned future feature.

Q: How does DG3 help reduce execution latency? A: DG3’s Trade Desk supports 1-Click Trade mode, which pre-configures Kelly fraction, order type, and routing so the trader executes with a single tap. The Intelligence pane tracks whale activity and order flow in real time, supporting faster signal identification. Phase 0 operates on Polymarket. Cross-venue execution routing is a planned future feature.

Q: What does sub-100ms execution mean for edge capture? A: Sub-100ms execution means the round-trip from order submission to CLOB receipt takes under 100ms. At this speed, entry price closely matches the price at the moment of decision for most market conditions. The practical value is in institutional arbitrage strategies where pricing gaps between correlated markets exist for under a second. For retail event-driven strategies, the more valuable target is eliminating 10-second human click sequences, not reducing 200ms network latency to 80ms.

Q: Does execution speed matter for long-horizon prediction market positions? A: Rarely. On a political market with 8 weeks to resolution, price movement during a 30-second lag is negligible. The binding constraint on long-horizon positions is model accuracy, the probability estimation, not execution speed. Speed investment is most valuable on the subset of positions with short edge windows, typically event-driven and information timing trades.

Final Thoughts

Execution speed is infrastructure. Infrastructure amplifies the edge you already have. A trader with a well-calibrated probability model and WebSocket infrastructure beats a trader with fast infrastructure and a bad model, on every question type, over any meaningful sample.

Get the model right first. Then, for the specific trades where the edge window is measured in seconds, invest in the infrastructure to capture it. In that order.

The Edge Decay guide explains how fast different edge types compress and why speed matters specifically in the context of alpha half-lives. The Slippage guide covers the execution cost dimension of the same problem.